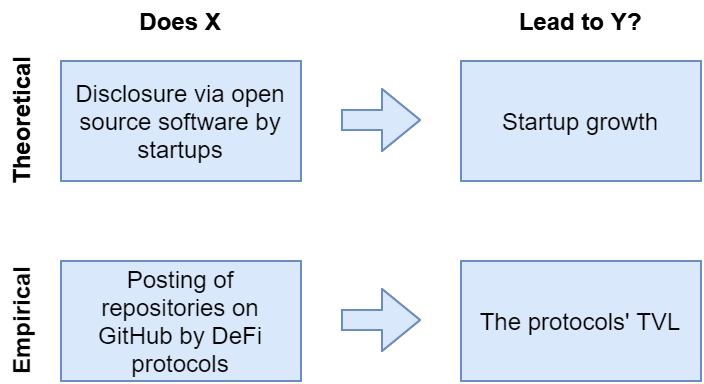

Main result

“We start our empirical examination with an event-study framework that treats the launch of a new open-source repository as a quasi-exogenous information shock to the market and developer community”

- However, the choice to open source is highly endogenous in DeFi

- Which is a concern for the main result, that GitHub repositories lead to increased TVL

- It may also explain the large economic effects

- Per the intro, $+4.3M TVL per repository on an average TVL of $6.1M

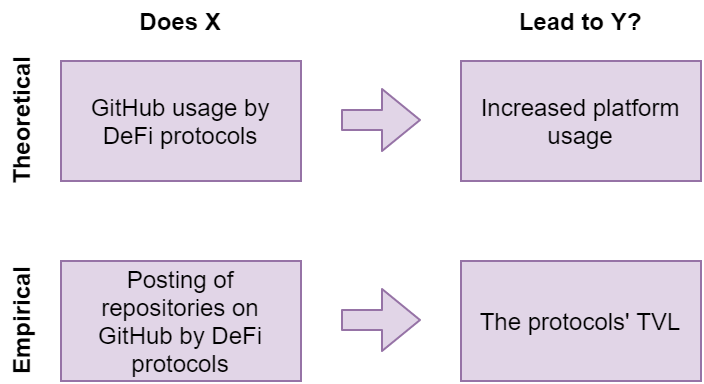

Protocols’ incentives

Platforms can open source code as part of a plan to increase TVL