| Number | Topic | Top_words |

|---|---|---|

| 23 | Financial | market, growth, markets, trading, earnings, global, report, quarter, results, energy |

| 2 | Nonfinancial: Marketing | #shareacoke, make, #tastethefeeling, gifs, reply, mistletoe, happy, tweets, #makeithappy, hashtag |

| 12 | Other | el, paso, police, trump, obama, man, city, donald, news, york |

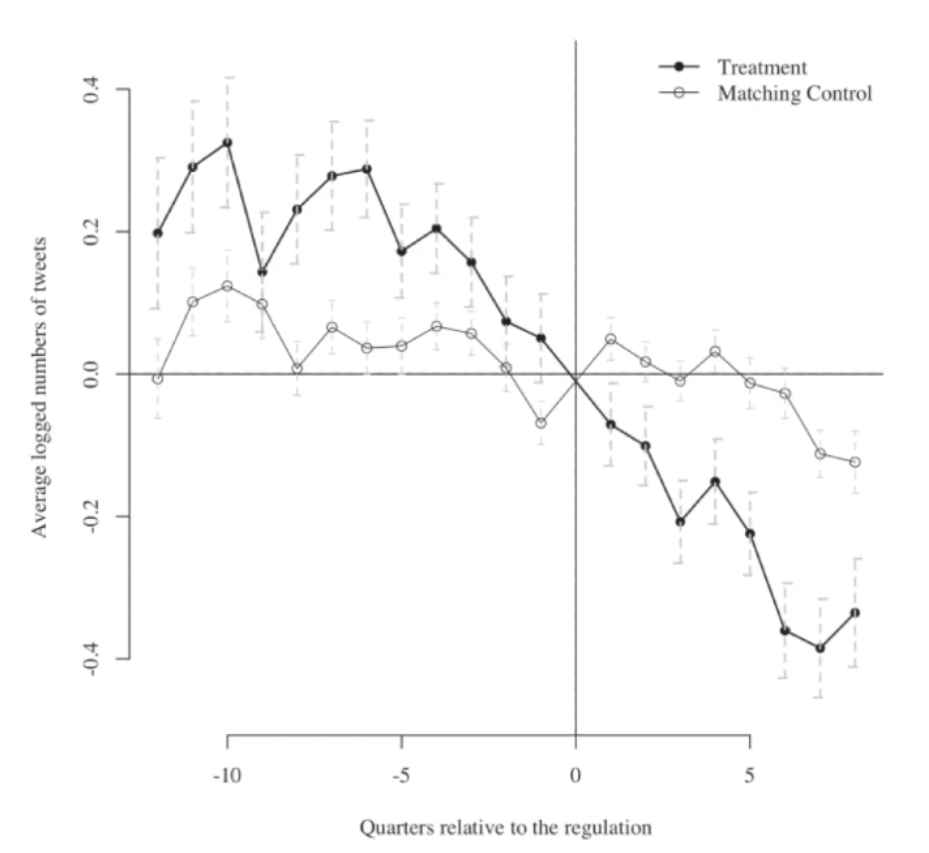

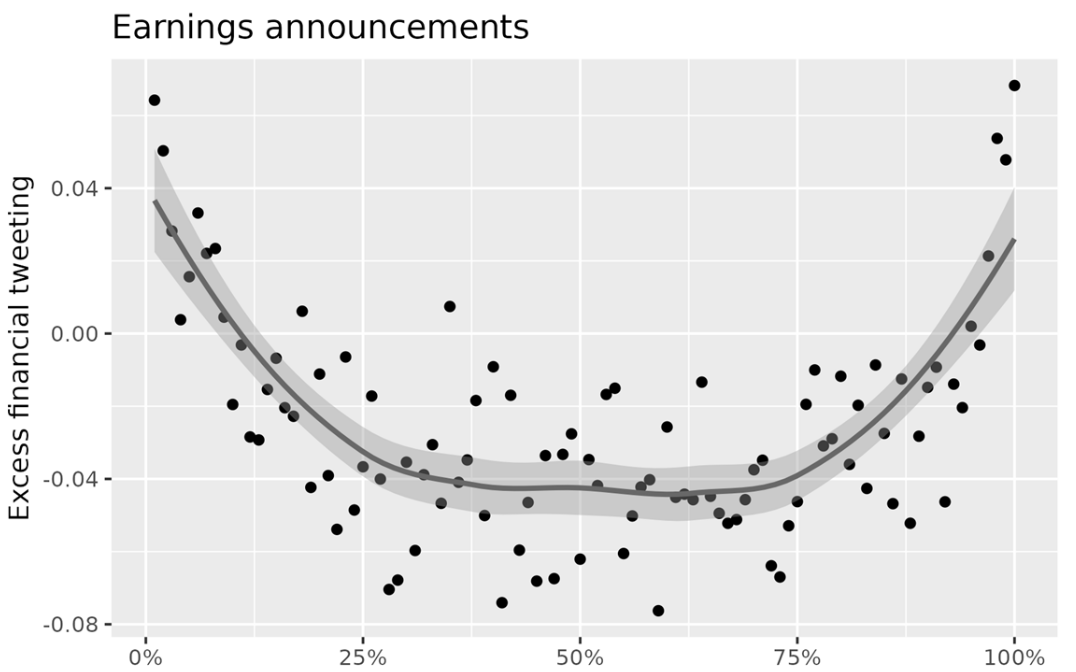

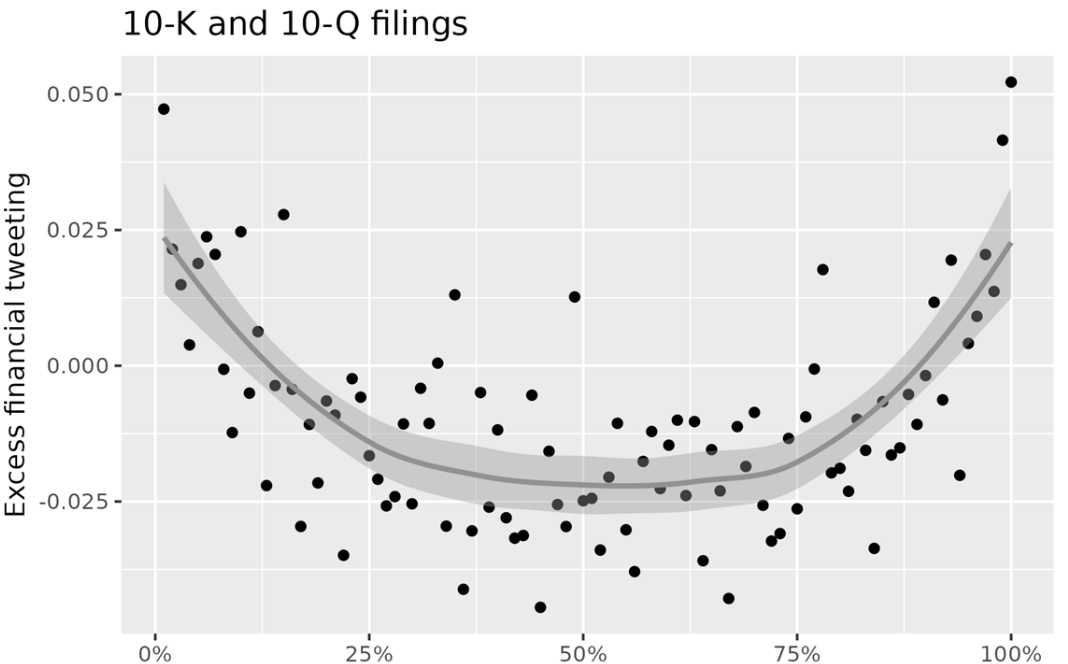

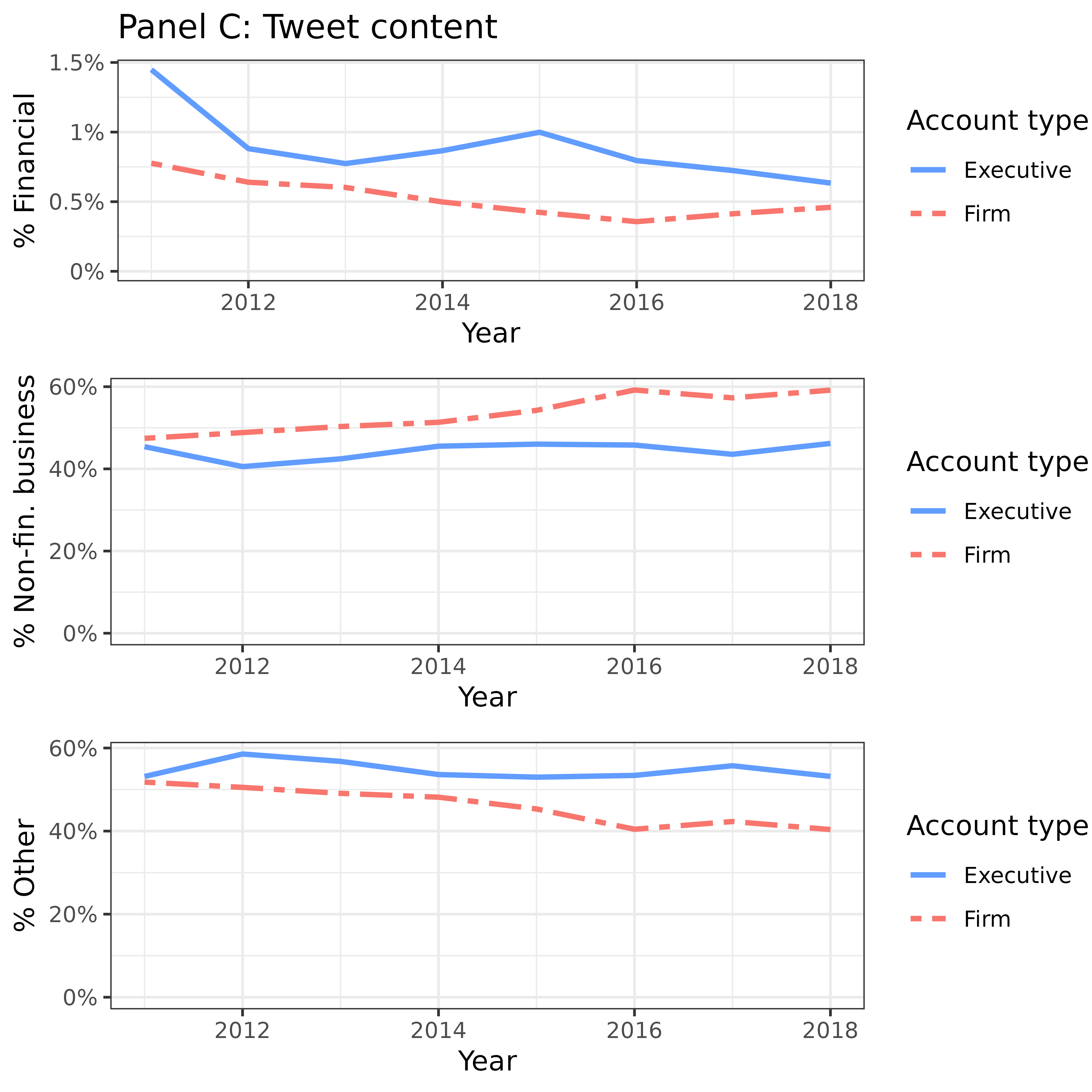

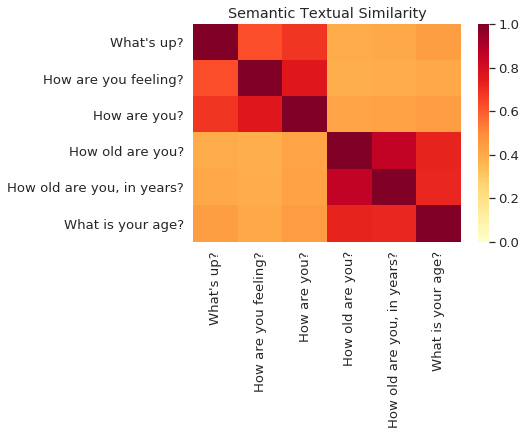

Main result