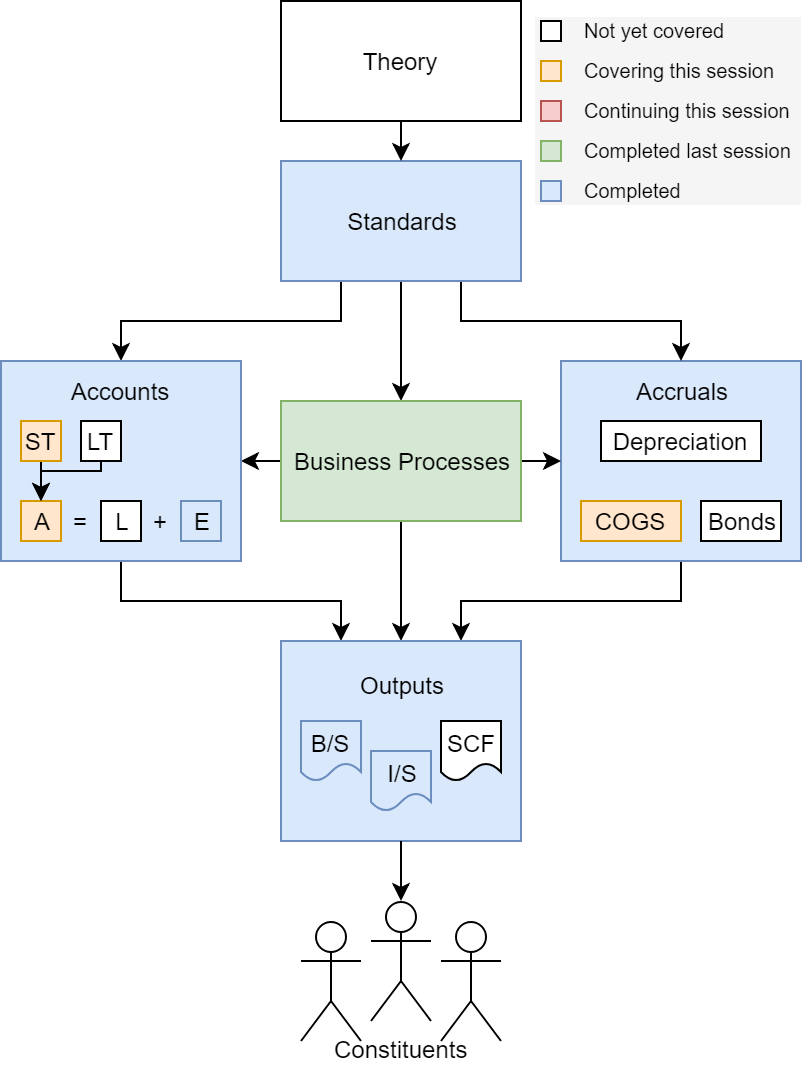

Learning objectives

Starting part 2 of the course

- Deep dive into transactions

Inventory (Chapter 6)

- Understand the nature of inventory operations

- Record inventory transactions

- Determine inventory and COGS value

Firm types

- Service firms

- Have little to no inventory

- Merchandisers

- Get inventory items

- Sell them at a higher price

- Than inventory cost + overhead

- Manufacturers

- Get raw materials

- Transform raw materials into finished goods

- Sell them at a higher price

- Than raw materials + transformation + overhead

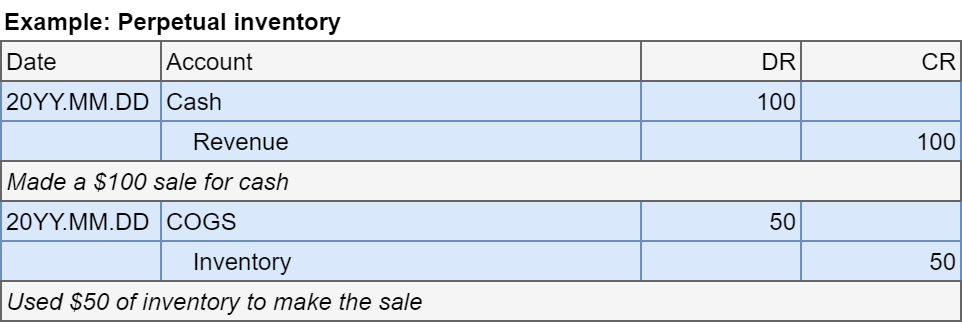

Perpetual inventories

- Usually barcode based.

- Allows efficient tracking

- Record two entries per transaction

- DR Cash or A/R (↑), CR Revenue (↑)

- DR COGS (↑), CR Inventory (↓)

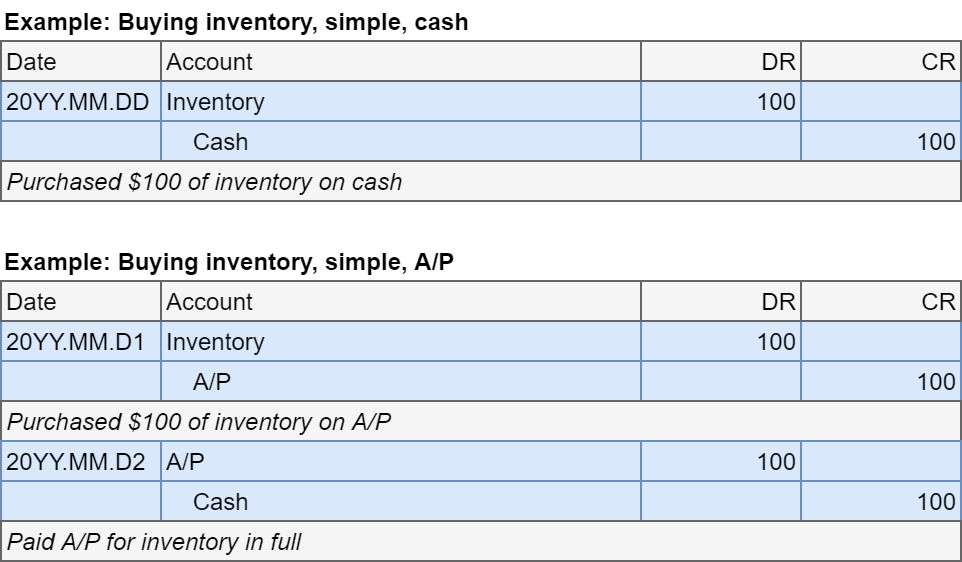

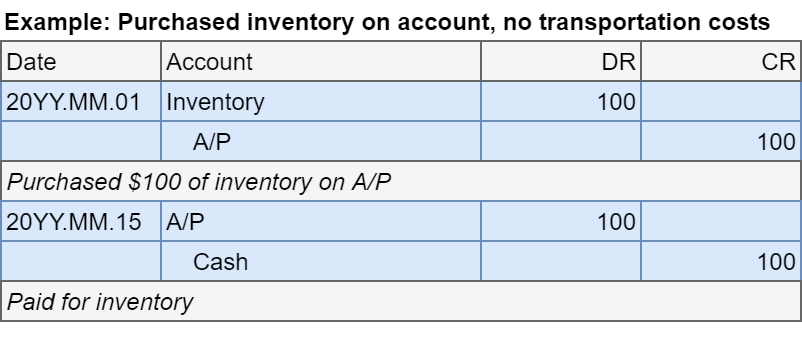

Simple case

- Buying on cash or A/P

- Paying full amount

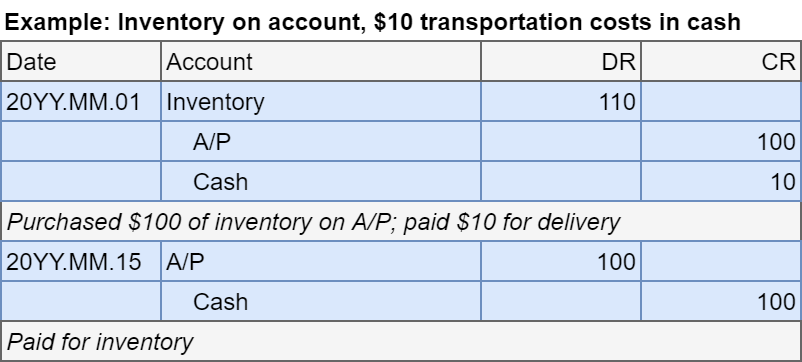

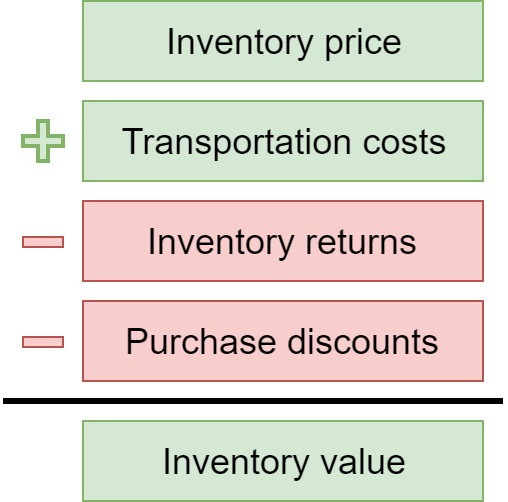

Shipping

- If there are shipping costs to receive the inventory, we add those to the inventory value itself

- Debit inventory

- Credit cash

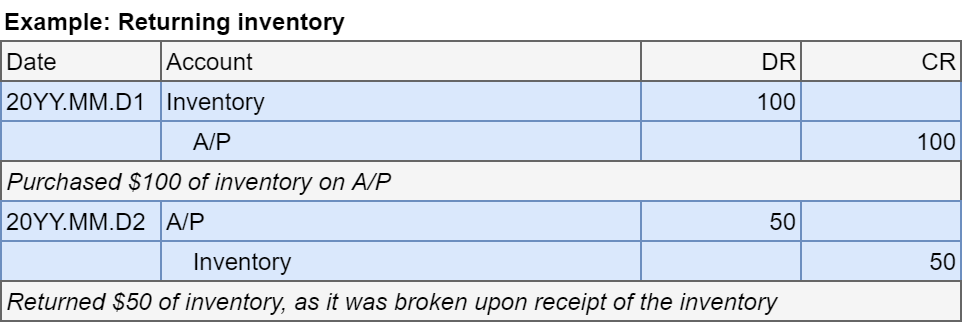

Returns

- Sometimes inventory needs to be returned

- Wrong or faulty/broken items

- To record:

- Directly credit the inventory account for the amount returned

- OR: Credit “Purchase returns,” a contra-asset to inventory

- Debit…

- A/P if not yet paid

- Cash if paid and receiving cash now

- A/R if paid and receiving credit now or cash later

- Directly credit the inventory account for the amount returned

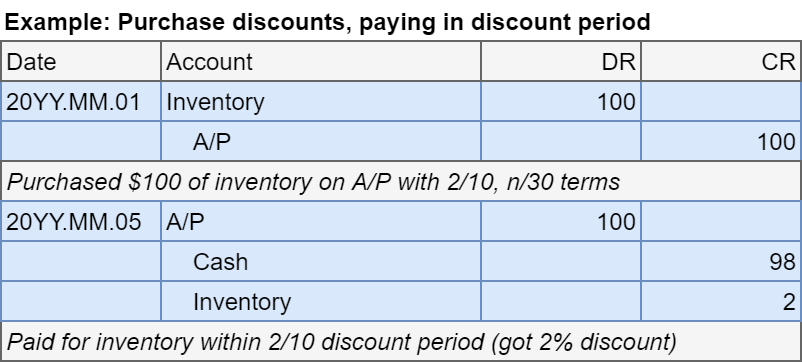

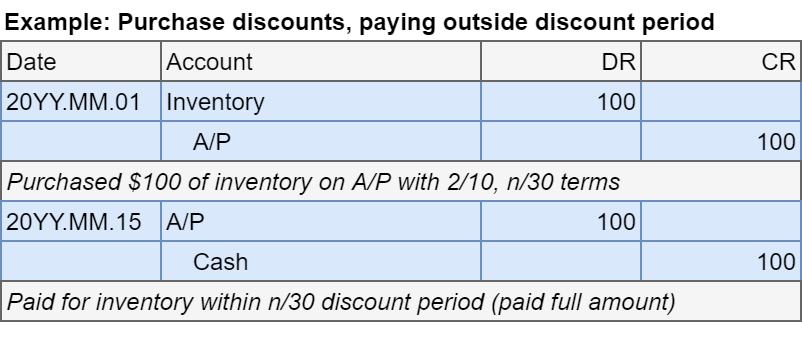

Payment and discounts

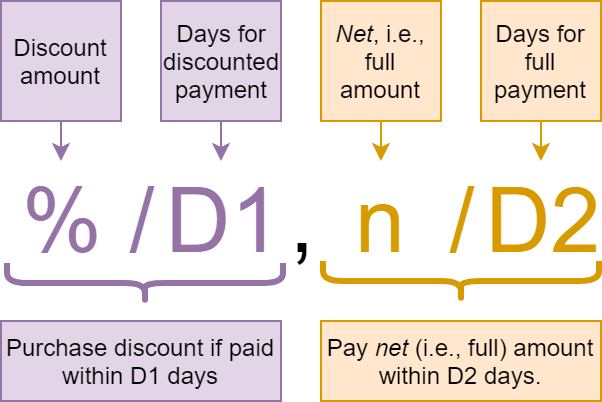

- Sometimes companies offer discounts for paying early

- There is a standard format for B2B discounts:

- Ex.: 2/10, n/30 =

- Get a 2% discount if paid in 10 days

- Pay the full amount by 30 days.

Discounts in journal entries

- Record discount as a decrease in inventory

- Remember: we record assets at cost paid for them

- Can also record to a “purchase discounts” contra-asset

Situation: Purchase inventory on account for $100 with 2/10 n/30 terms

Bringing it all together

Practice question (3 entries):

- Purchased $200 of inventory on account with 10/5, n/45 terms

- Also paid $20 in shipping to DHL on delivery

- $50 of inventory was damaged, which we returned

- Paid payable 3 days after receiving inventory

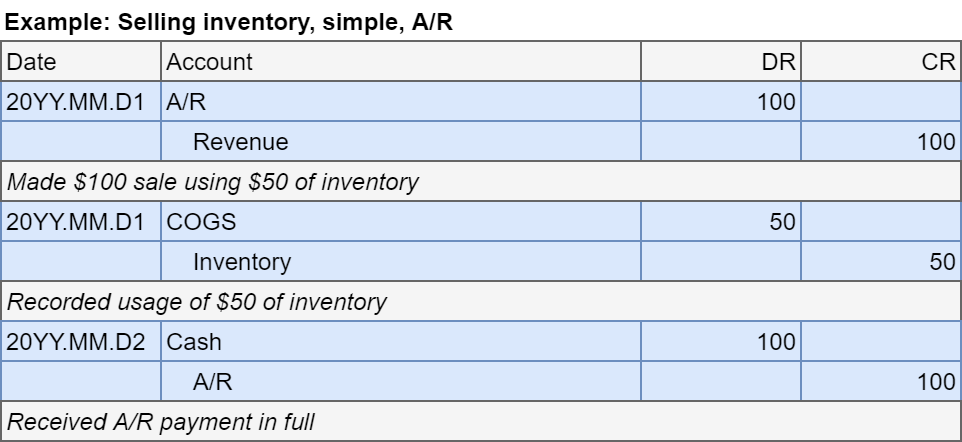

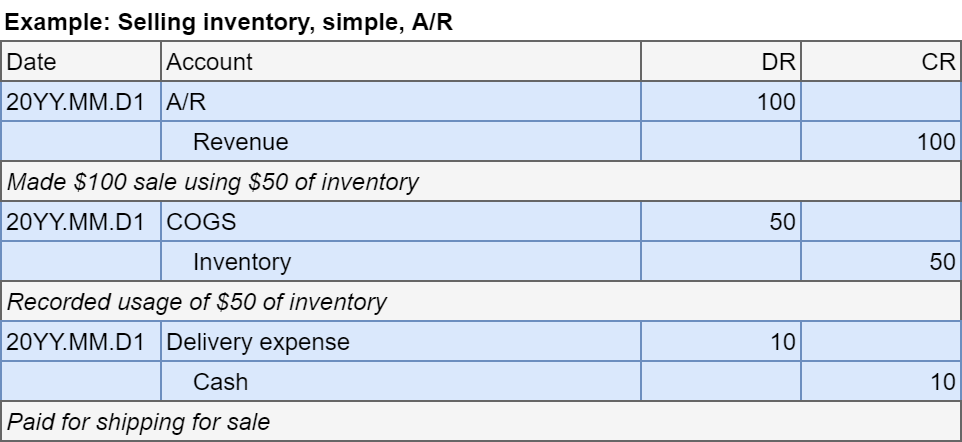

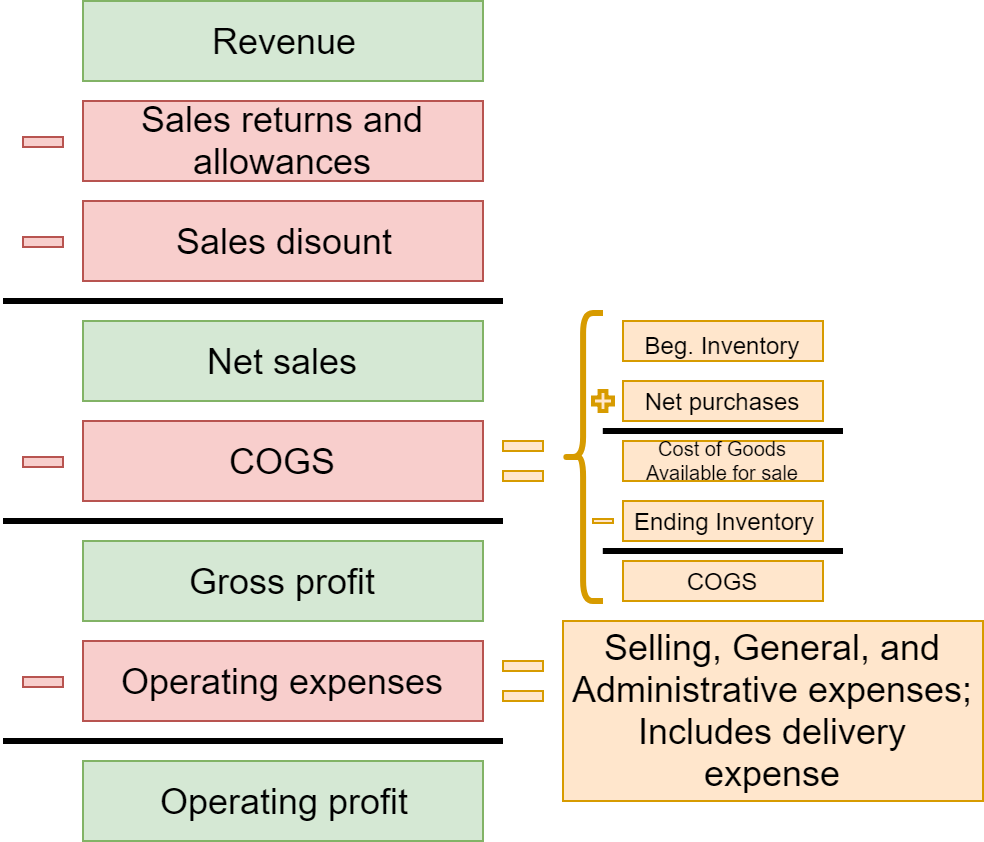

General case

- Selling for cash or A/R

- Receiving full amount

Revenue for goods

- Recognize revenue when earned

- Recall from lesson 2: Revenue recognition principle

- FOB shipping point: record when given to shipping company

- FOB destination: Record when customer receives goods

- Since we will need to pay shipping, we will have a Delivery expense account, an operating expense

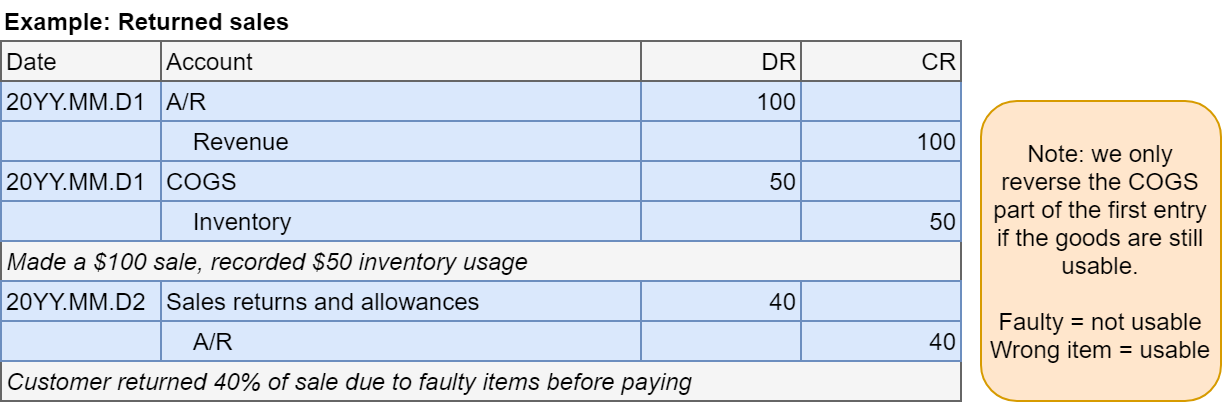

Returns, revisited

- Sometimes our sales are returned: Wrong or faulty/broken items

- To record, debit…

- If faulty: sales returns and allowances

- Contra-equity to revenue

- If usable: COGS

- If faulty: sales returns and allowances

- And credit…

- A/R if not yet paid

- Cash if paid and returning cash now

- A/P if paid and giving credit now or returning cash later

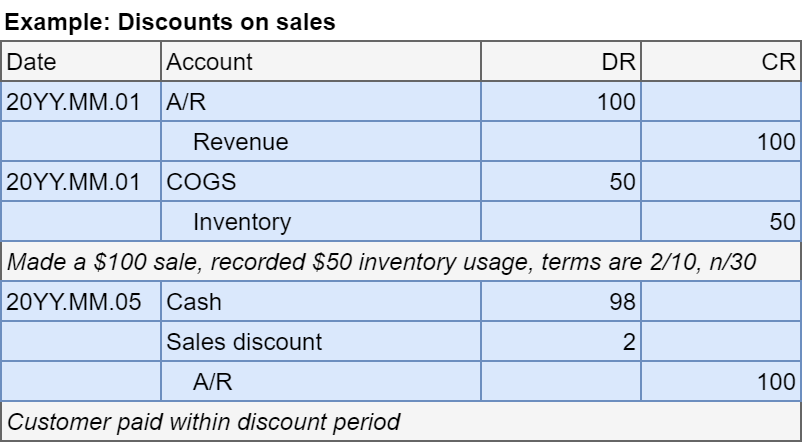

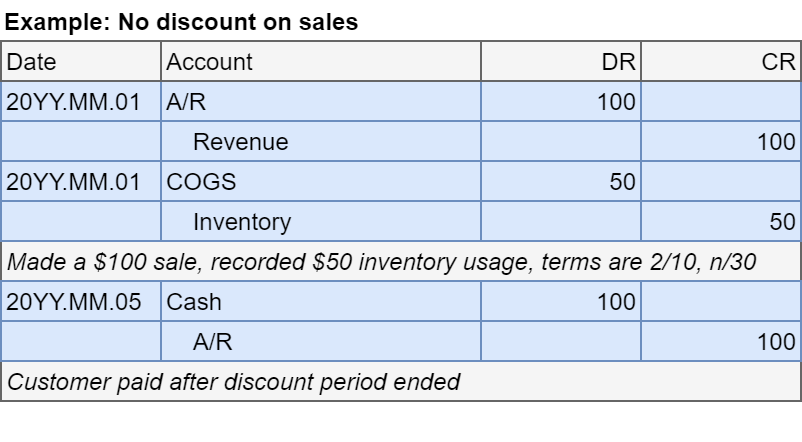

Discounts, revisited

- We use the same discount terminology here

- Record any discount as a debit to Sales discount

- Another contra-equity to revenue

Situation: Sold inventory of $50 for $100 on account with 2/10 n/30 terms

Bringing it all together

Practice question:

Determine the journal entries, and then calculate Net sales, Gross profit, and operating profit

- Sold $155 of inventory for $300 on account with 10/5, n/45 terms

- Also paid $20 in shipping to DHL for delivery

- $50 of goods were damaged, which were returned to us

- Customer Paid receivable 3 days after receiving goods

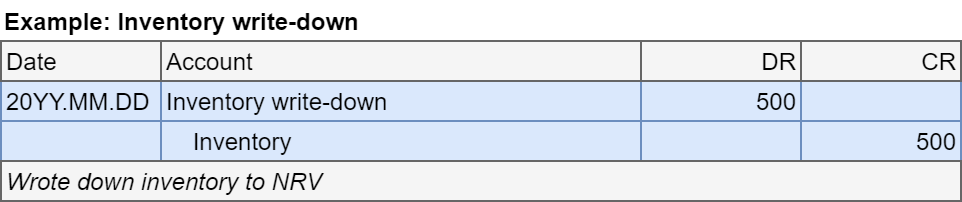

Buy low, selling lower…

- Need to write down your inventory value

- If book value of inventory > lower of cost or NRV

Situation: Inventory is valued at $1,500, but NRV is $1,000

- Can be reversed if the value goes back up

- Only up to the amount originally written down

- Credit gain when reversing

Practice: Gross profit method

Situation: Coffee Corp sells all of their products using fixed margins. Determine the COGS for each product below, using the given revenues.

- $50,000 worth of lattes were sold with a fixed gross margin of 70%

- $9,000 worth of travel mugs were sold at a 50% mark-up

- $1,000 worth of espresso cups were sold, comprising 50 cups each sold with $8 profit (all cups cost the same)

Specific identification

- Only used with expensive items

- Too costly to track individual items otherwise

- Examples

- Cars

- Luxury goods

- Real estate

Record COGS with revenue

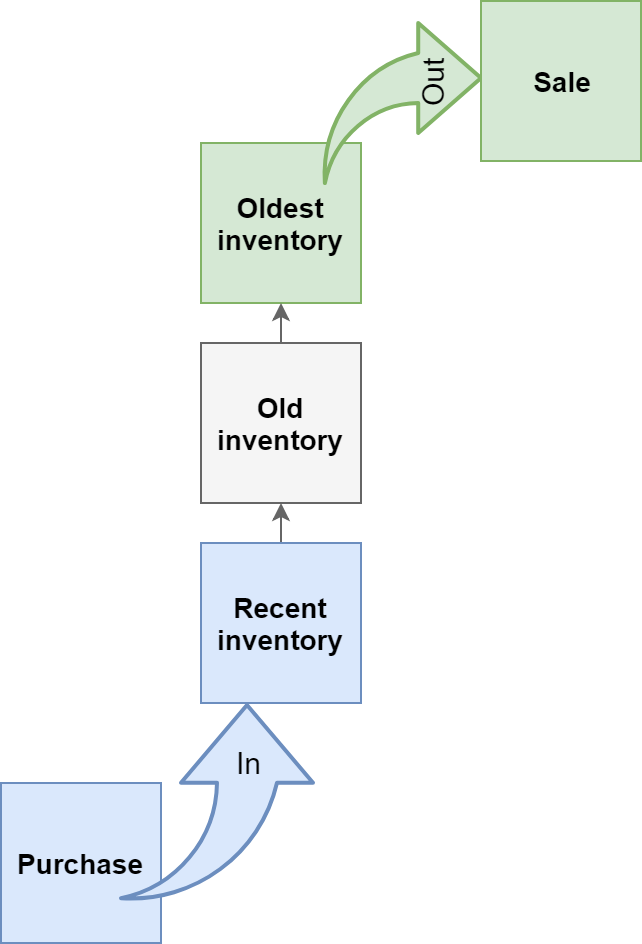

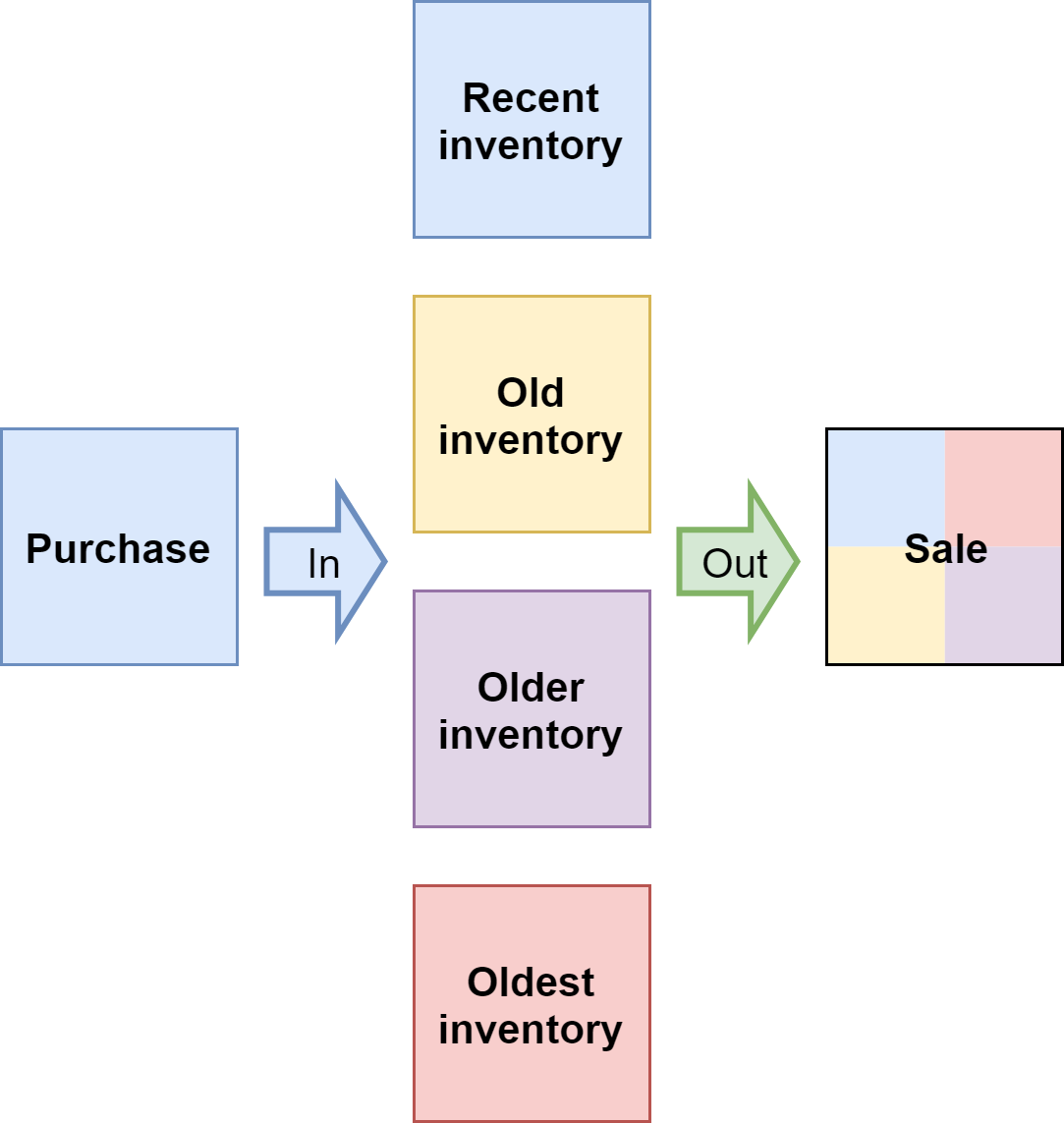

FIFO

- First In, First Out

- Assumes you sell items in the order you received them

- Ex.: You buy 5 bags of coffee beans for $10 each, and then another 5 at $12 each. You sell 3 bags and then 4 bags.

- The first 3:

- \(3 \times 10 = \$30\)

- The next 4:

- \(2 \times 10 + 2\times 12 = \$44\)

- COGS: $74 for 7 bags

- The first 3:

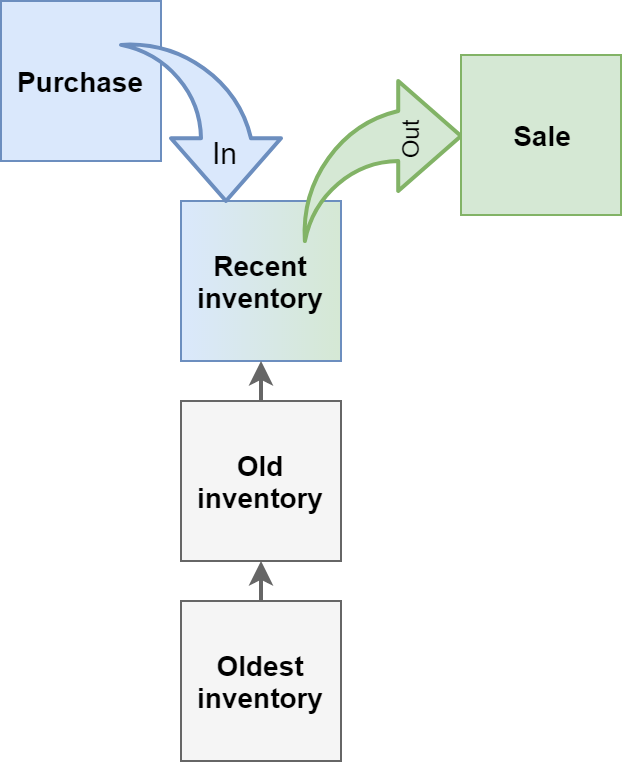

LIFO

- Last In, First Out

- Assumes you sell the most recent items first

- Ex.: You buy 5 bags of coffee beans for $10 each, and then another 5 at $12 each. You sell 3 bags and then 4 bags.

- The first 3:

- \(3 \times 12 = \$36\)

- The next 4:

- \(2 \times 12 + 2 \times 10 = \$44\)

- COGS: $80 for 7 bags

- The first 3:

Average cost

\[ \begin{equation*} Price = \frac{P_1 \times N_1 + P_2\times N_2 + \cdots}{N_1 + N_2 + \cdots} \end{equation*} \]

- Assumes you sell a mix

- Weighted average

- \(P_i\): price per item for order \(i\)

- \(N_i\): number of items in order \(i\)

- Ex.: You buy 5 bags of coffee beans for $10 each, and then another 5 at $12 each. You sell 3 bags and then 4 bags.

- Avg cost: \(\frac{5\times 10+5\times 12}{5+5}=\$11\)

- COGS: \(7\times \$11 = \$77\)

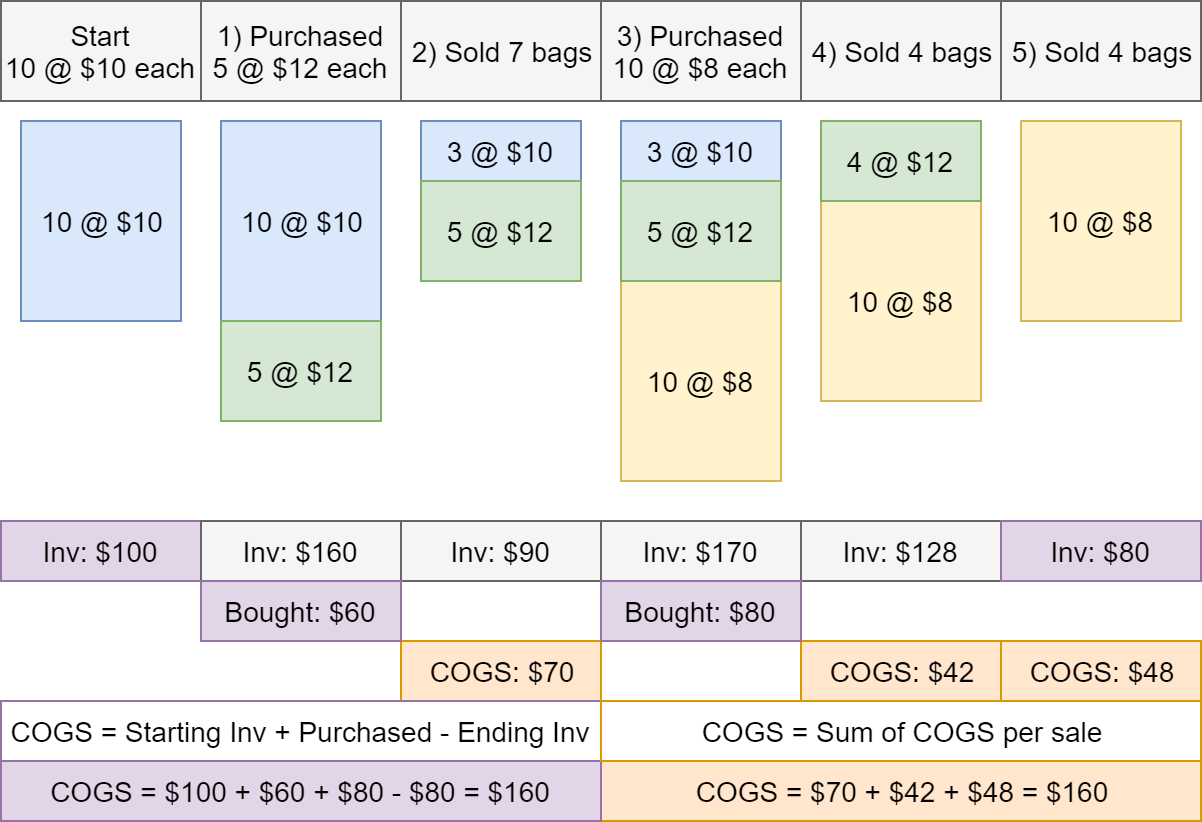

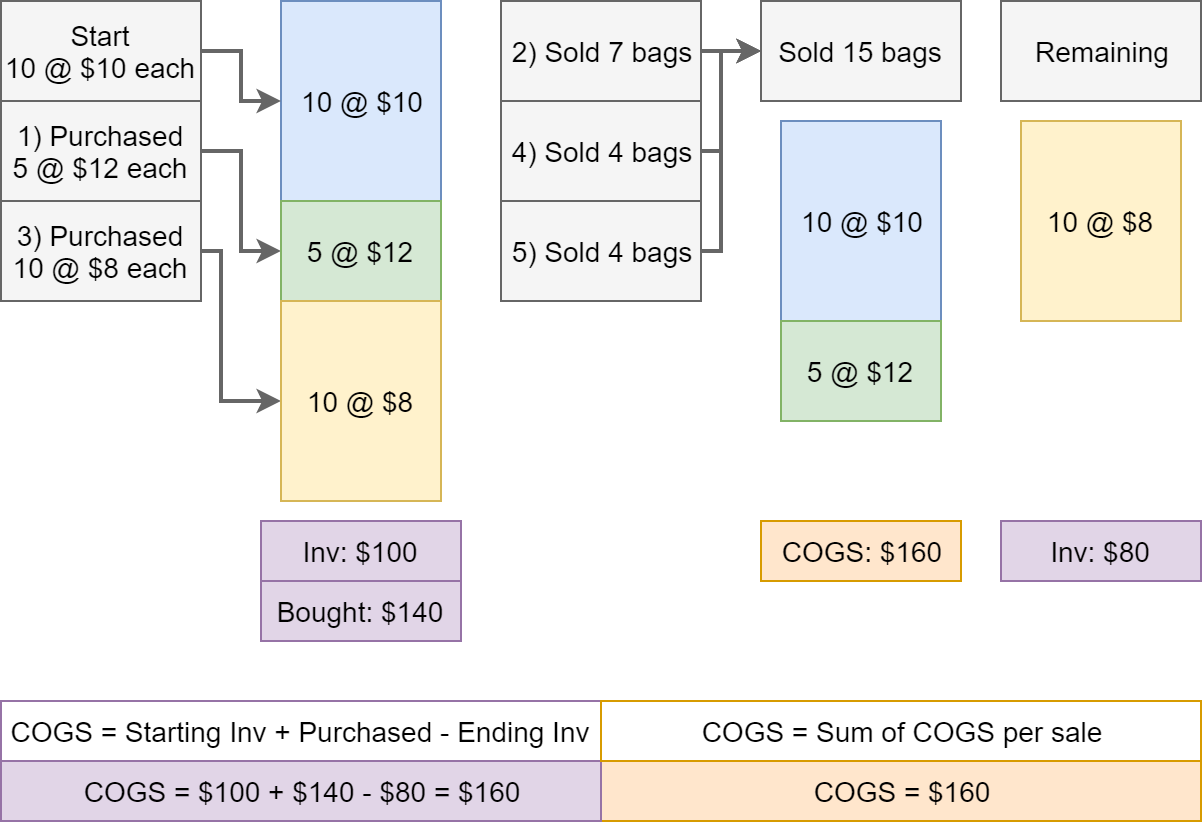

Example: FIFO, Perpetual

Started with 10 bags of coffee beans at $10 each. Then: 1) purchased 5 bags at $12 each; 2) Sold 7 bags; 3) Bought 10 bags at $8 each; 4) Sold 4 bags; 5) Sold 4 bags. Determine COGS.

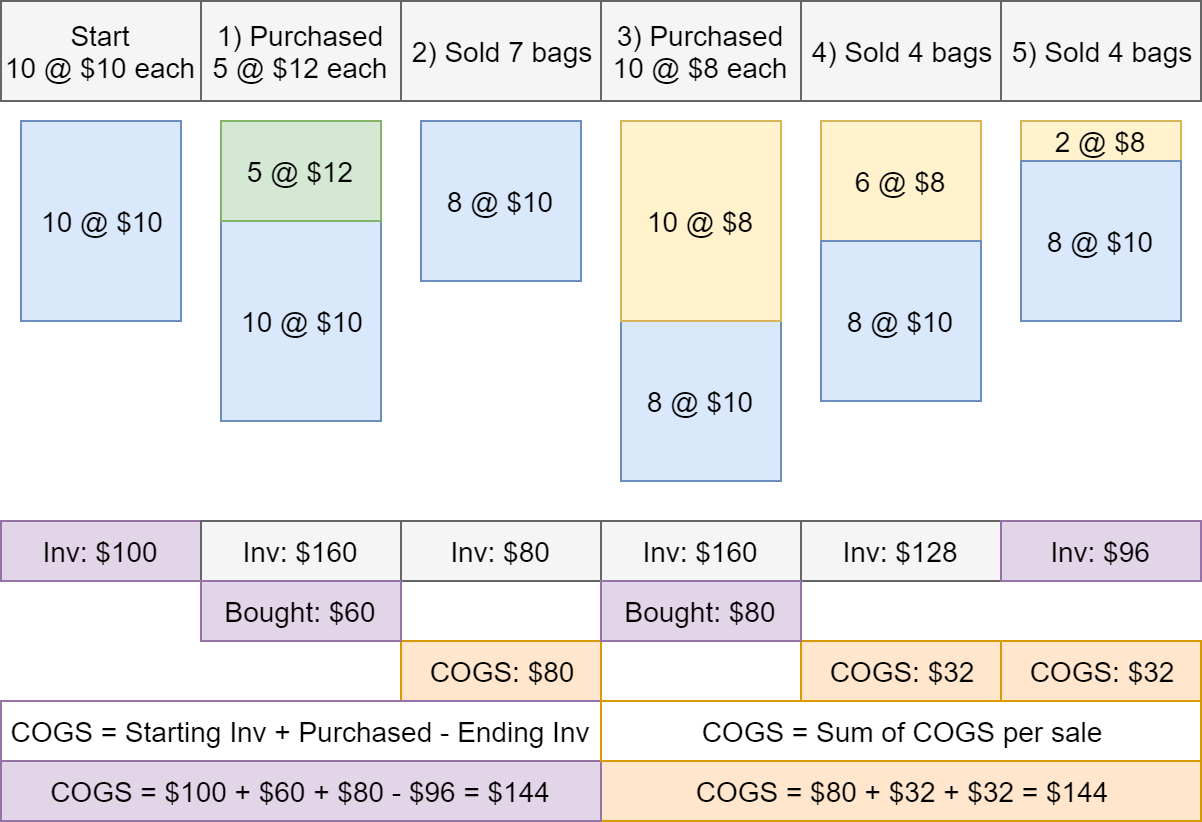

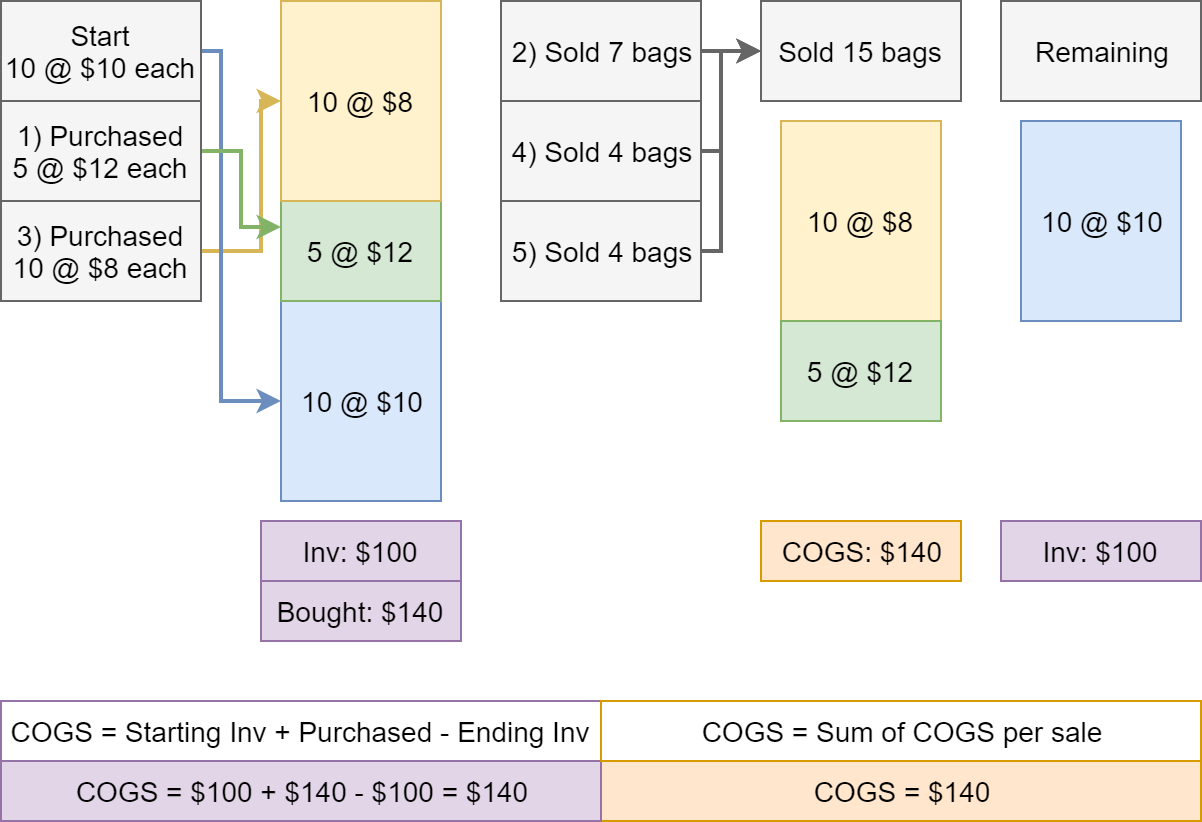

Example: LIFO, Perpetual

Started with 10 bags of coffee beans at $10 each. Then: 1) purchased 5 bags at $12 each; 2) Sold 7 bags; 3) Bought 10 bags at $8 each; 4) Sold 4 bags; 5) Sold 4 bags. Determine COGS.

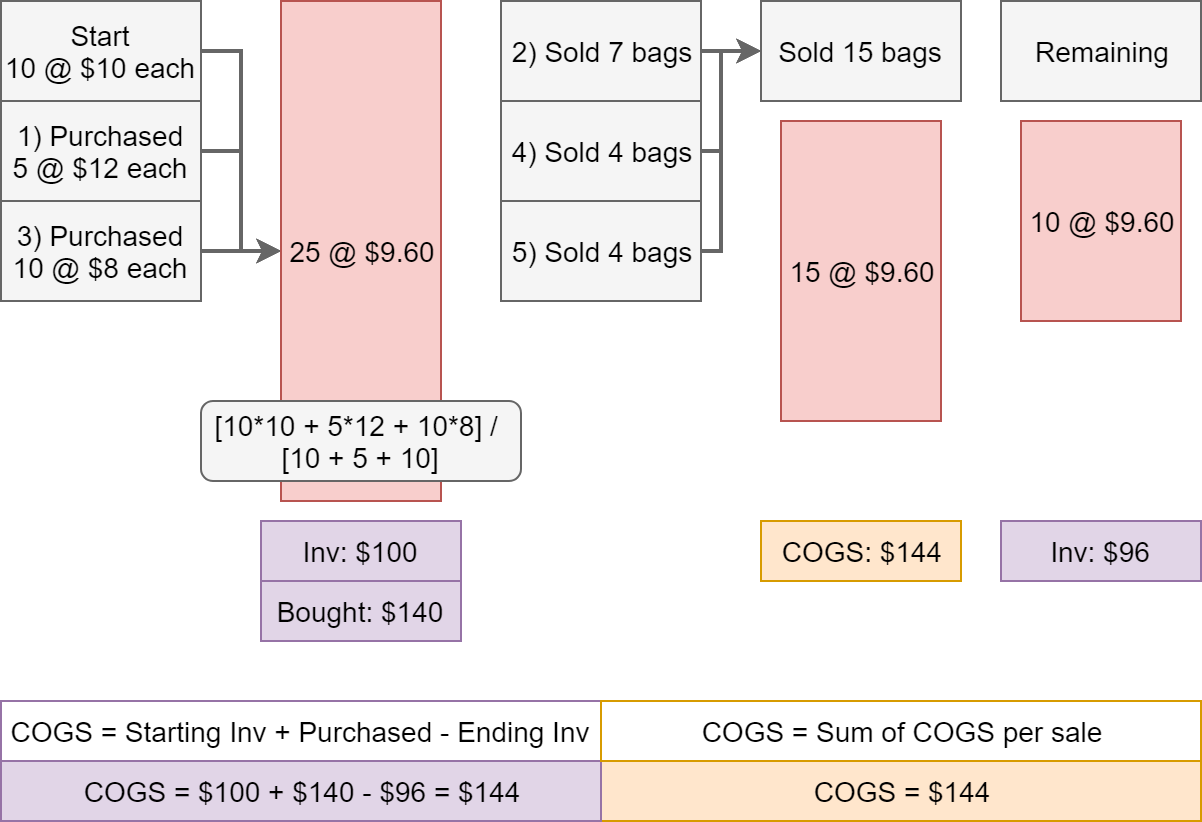

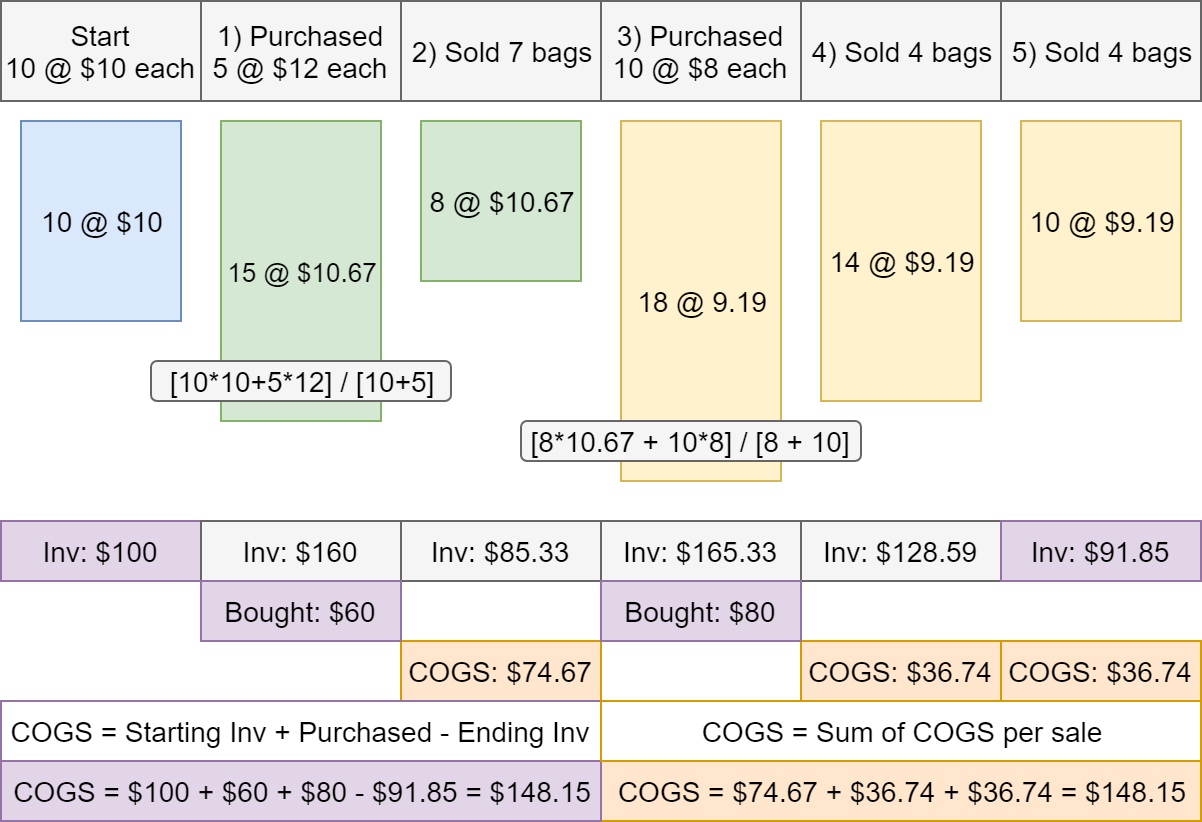

Example: Average cost, Perpetual

Started with 10 bags of coffee beans at $10 each. Then: 1) purchased 5 bags at $12 each; 2) Sold 7 bags; 3) Bought 10 bags at $8 each; 4) Sold 4 bags; 5) Sold 4 bags. Determine COGS.

Example: FIFO, Periodic

Started with 10 bags of coffee beans at $10 each. Then: 1) purchased 5 bags at $12 each; 2) Sold 7 bags; 3) Bought 10 bags at $8 each; 4) Sold 4 bags; 5) Sold 4 bags. Determine COGS.

Example: LIFO, Periodic

Started with 10 bags of coffee beans at $10 each. Then: 1) purchased 5 bags at $12 each; 2) Sold 7 bags; 3) Bought 10 bags at $8 each; 4) Sold 4 bags; 5) Sold 4 bags. Determine COGS.

Example: Average cost, Periodic

Started with 10 bags of coffee beans at $10 each. Then: 1) purchased 5 bags at $12 each; 2) Sold 7 bags; 3) Bought 10 bags at $8 each; 4) Sold 4 bags; 5) Sold 4 bags. Determine COGS.