Learning objectives

Liabilities (Chapter 9)

- Account for bonds at par

- Account for bonds not at par

- Account for bond buybacks

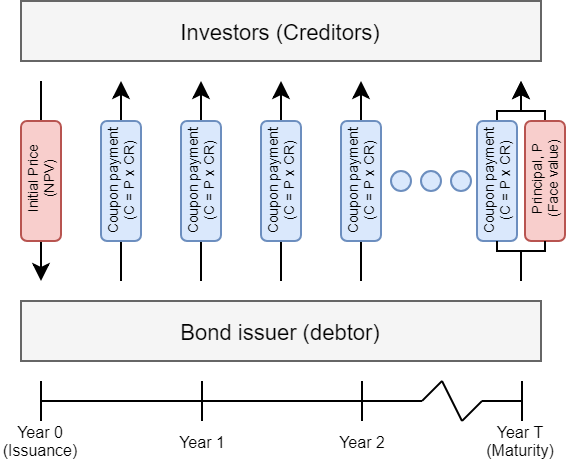

What is a bond?

- An interest bearing note payable

- Issued by a company in a manner similar to stock

- Often to investors (like stock)

- Trades on an exchange daily (like stock)

- Does not offer ownership

- For the simpler bonds we’ll cover in this course

- Usually due in 5 or 10 years, frequently longer

- Interest is usually paid every 6 months

Life of a bond

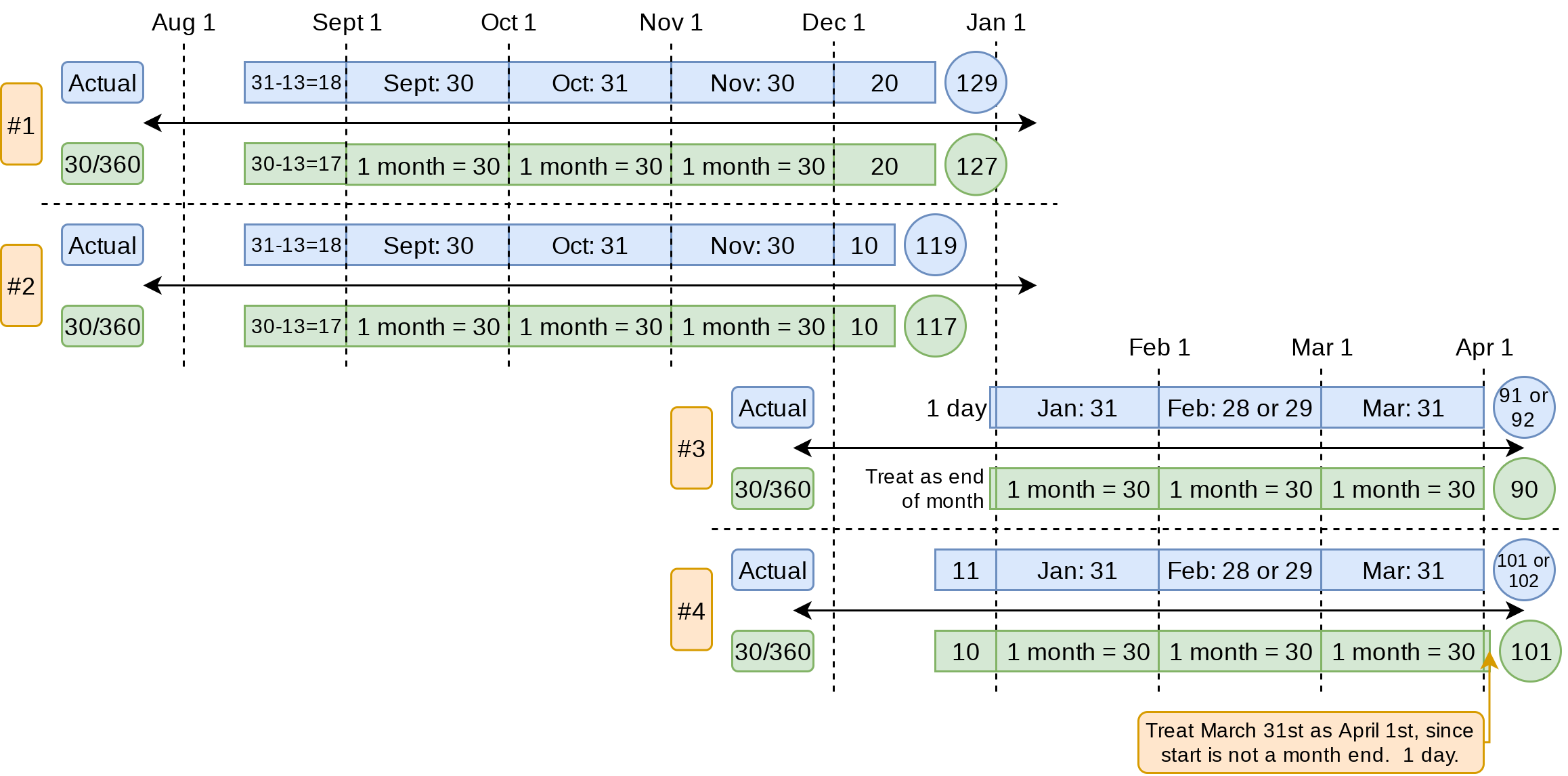

How to do day counts

Day counts, 30/360

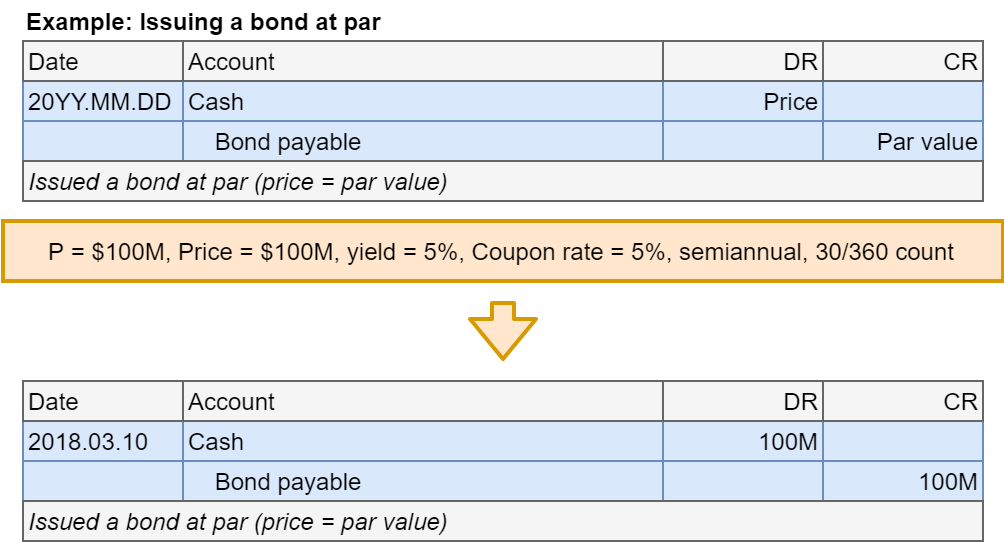

Bonds at par: Issuance

- If a bond is at par value, the accounting is the same structure as a note payable

- Step 1: Account for bond issuance

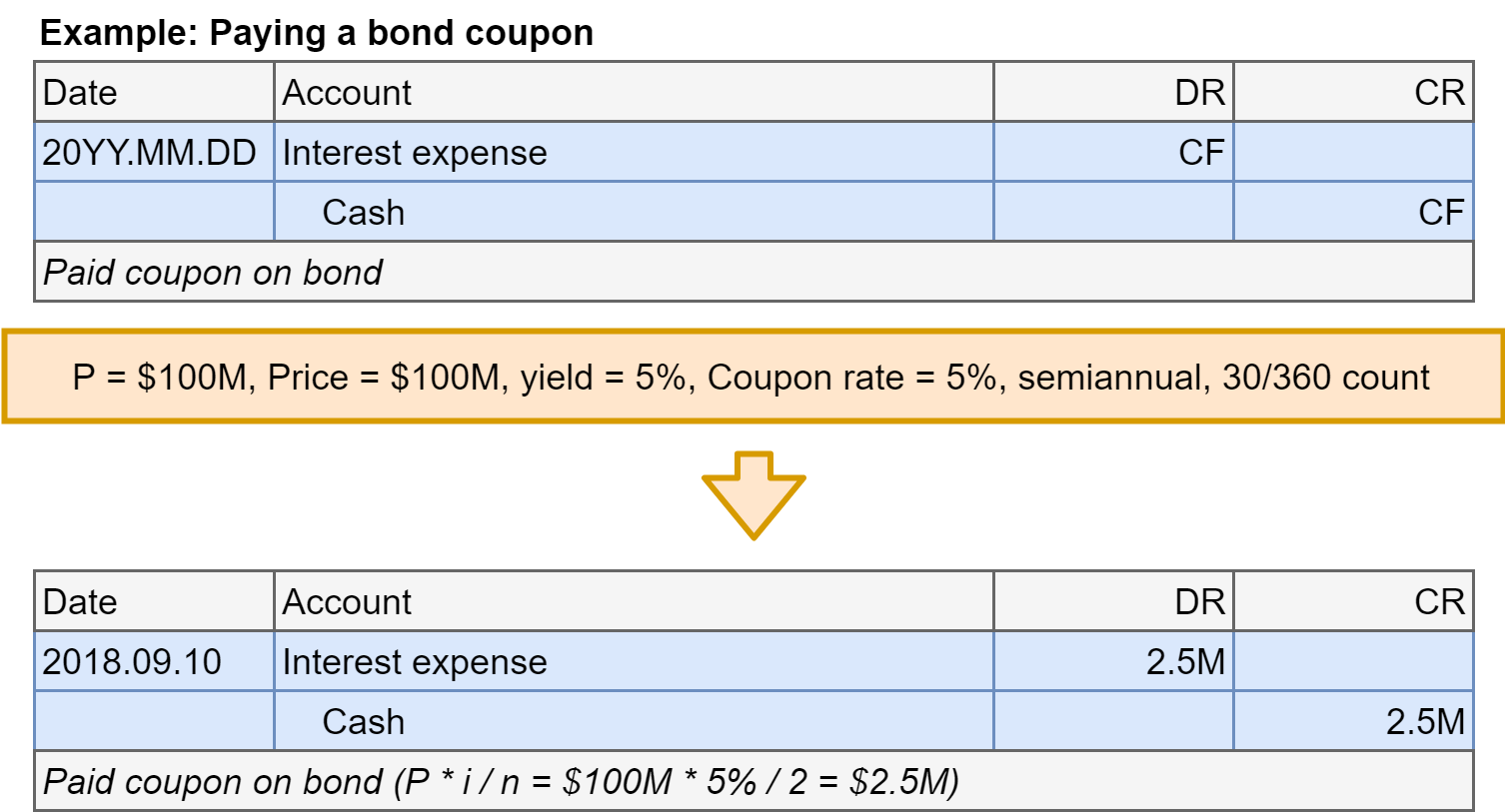

Bonds at par: Coupon payment

- Step 2: Account for coupon payments

- Interest expense

- Cash payment is the coupon

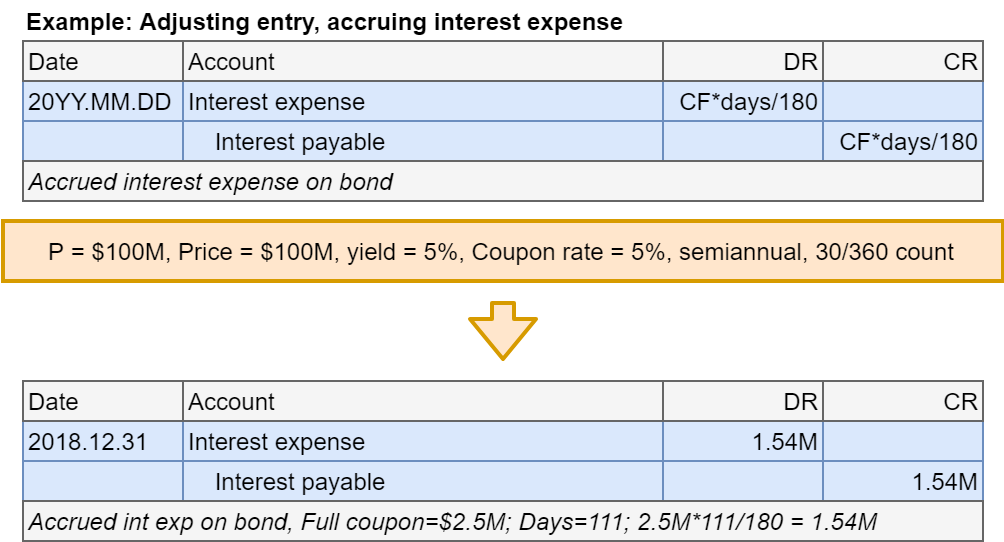

Bonds at par: Adjusting entry

- Step 3: Account for accrued interest expense at year end

- The accrued interest is based on the number of days

- We’ll use 30/360 day counts unless otherwise stated

- Interest owed will be \(CF \times \frac{days}{180}\)

- The accrued interest is based on the number of days

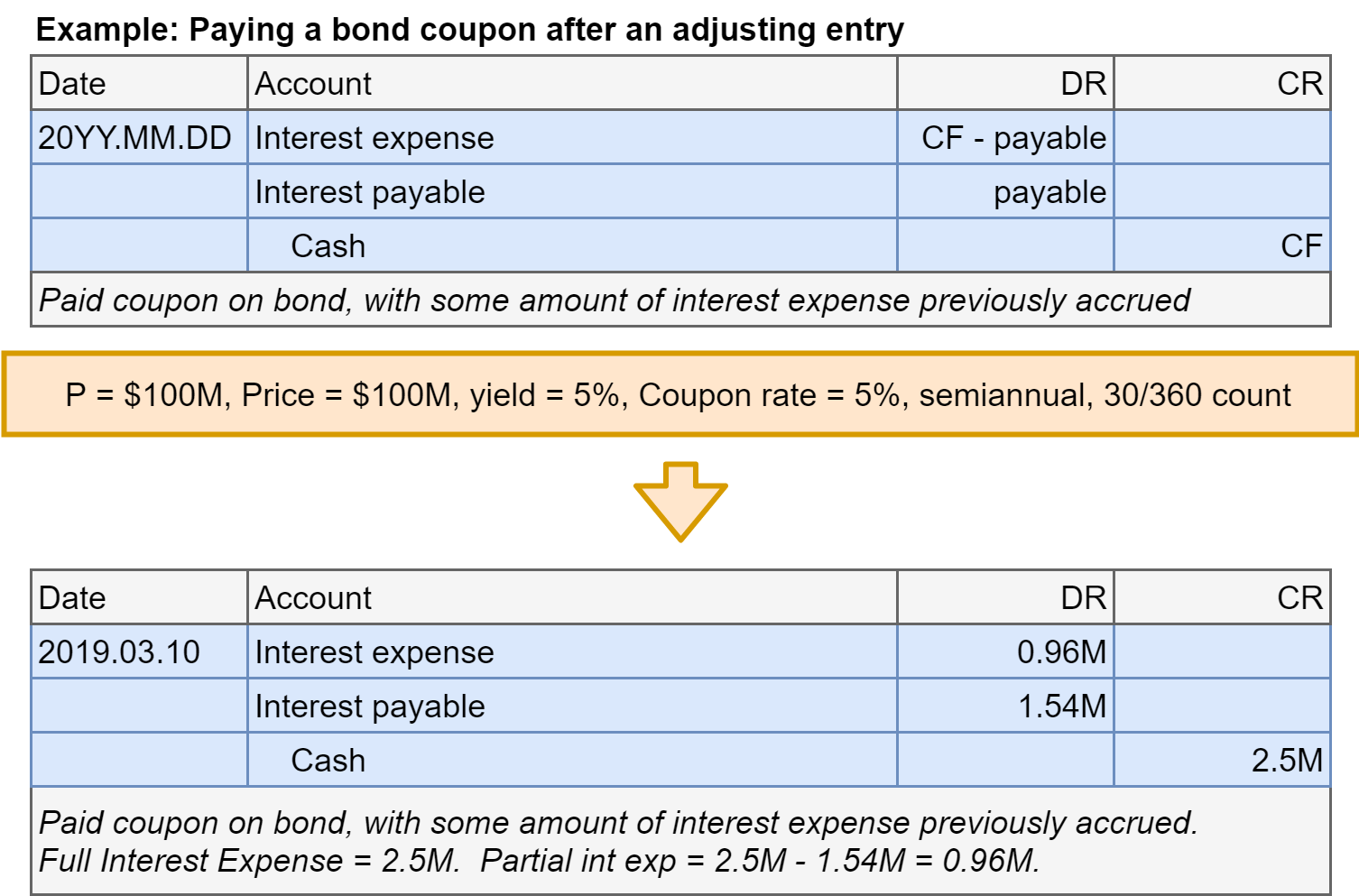

Bonds at par: Coupon after adjusting

- Step 2 revisited: Account for coupon payments

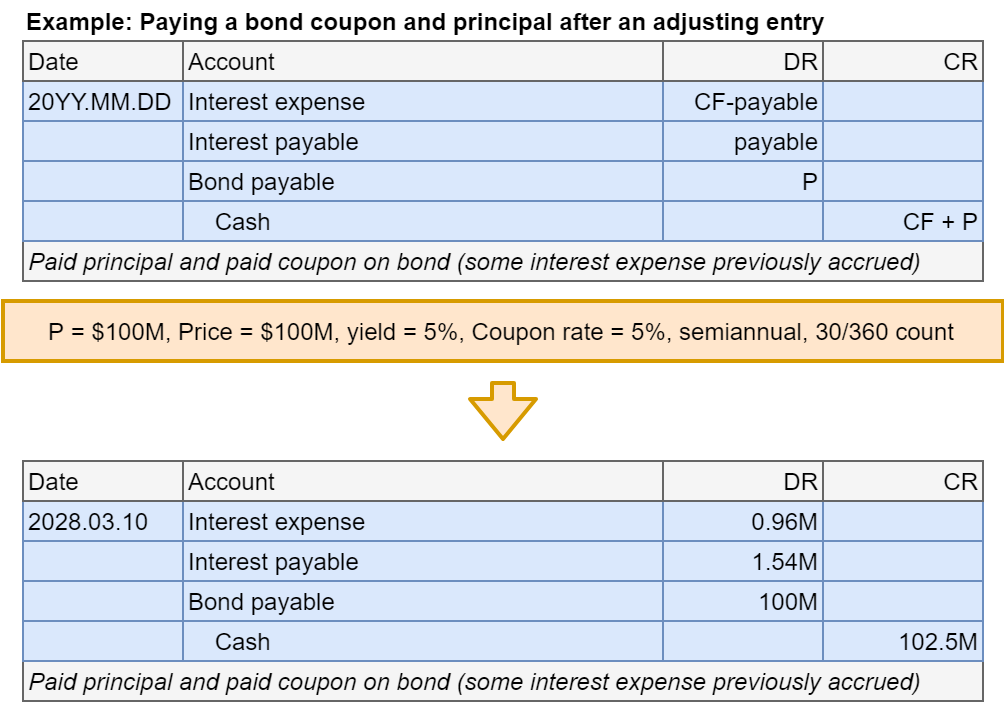

Bonds at par: Final payment

- Step 4: In the final period, pay back the principal (and a coupon)

- Since interest expense is the same every period for bonds at par, we can figure this out

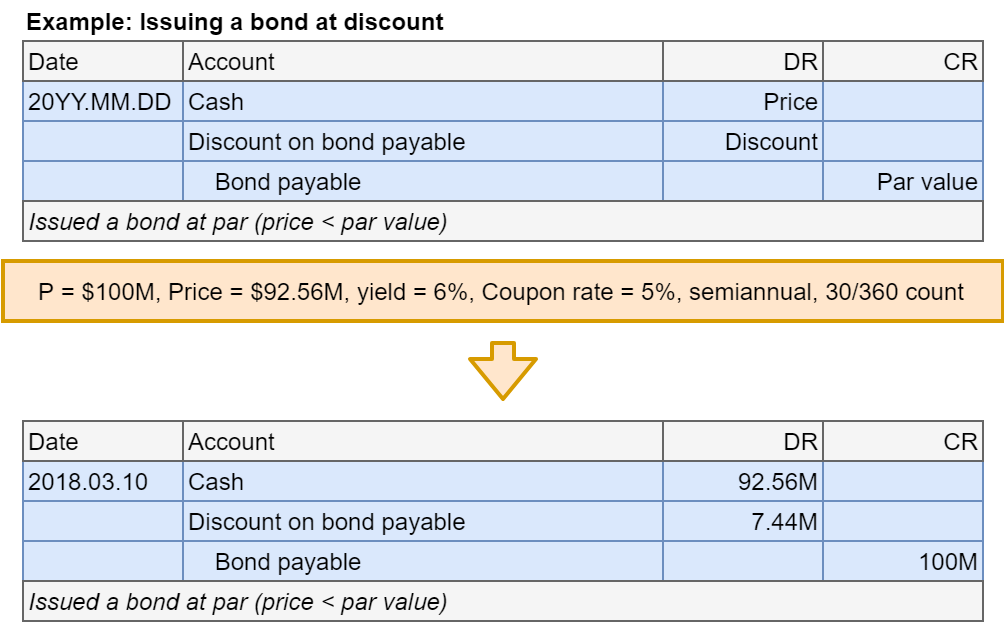

Bonds at discount: Issuance

- Step 1: Account for bond issuance

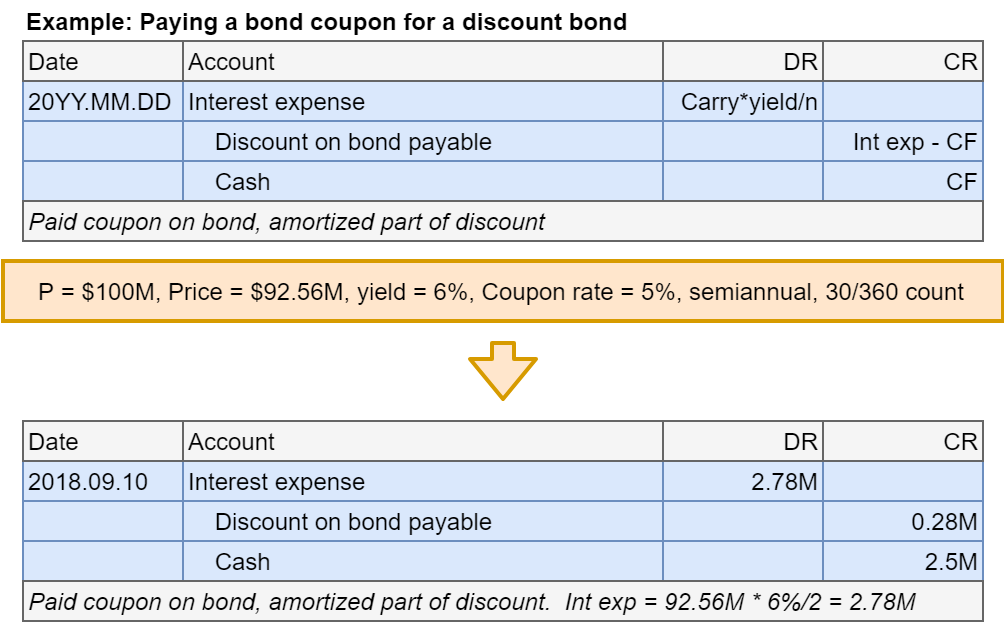

Bonds at discount: Coupon payment

- Step 2: Account for coupon payments

- Need to use the effective interest method!

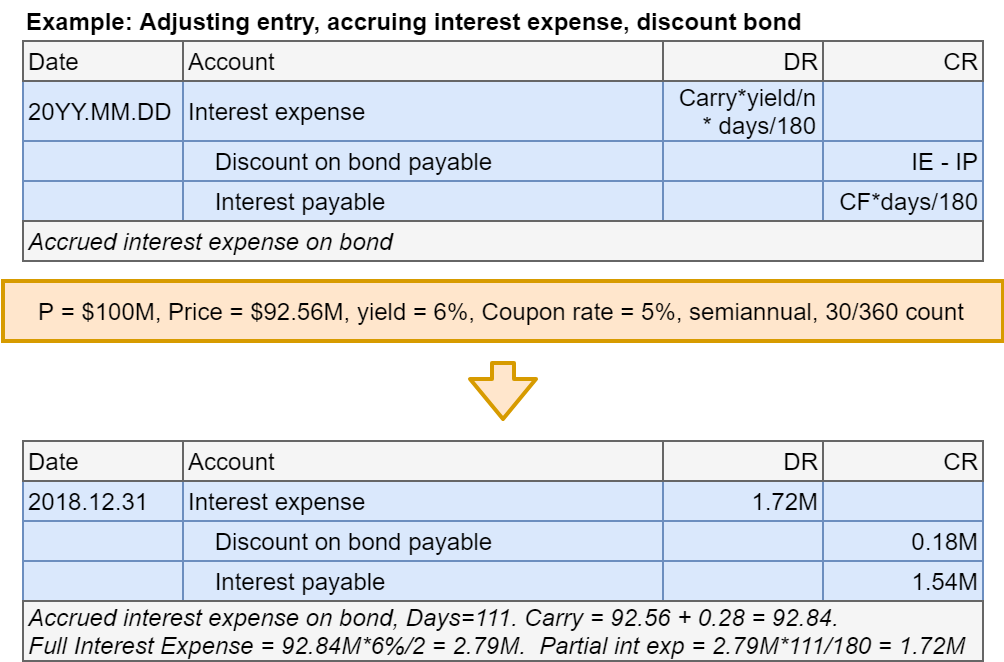

Bonds at discount: Adjusting entry

- Step 3: Account for accrued interest expense at year end

- Interest owed and interest expense will be multiplied by \(\frac{days}{180}\)

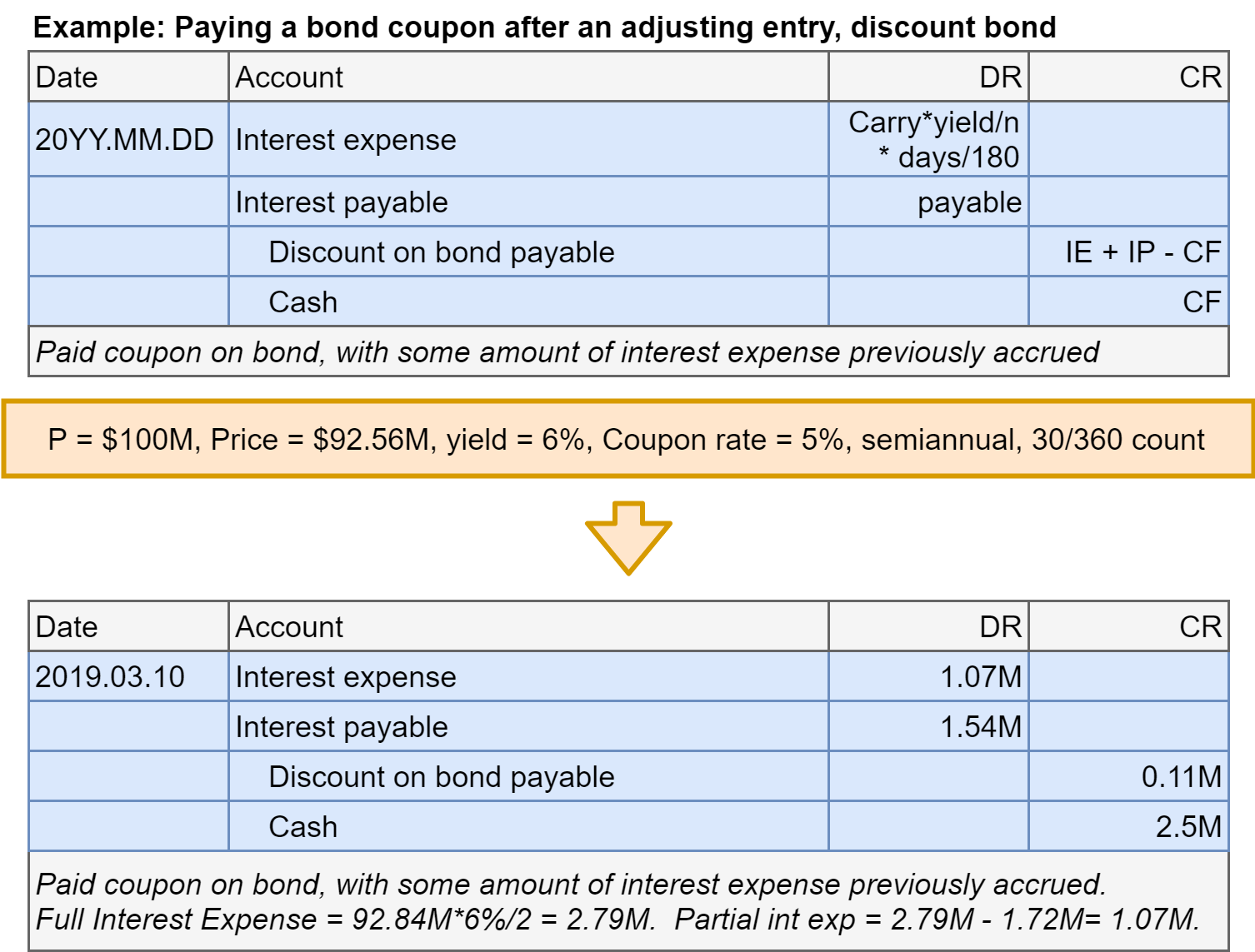

Bonds at discount: Coupon after adjusting

- Step 2 revisited: Account for coupon payments

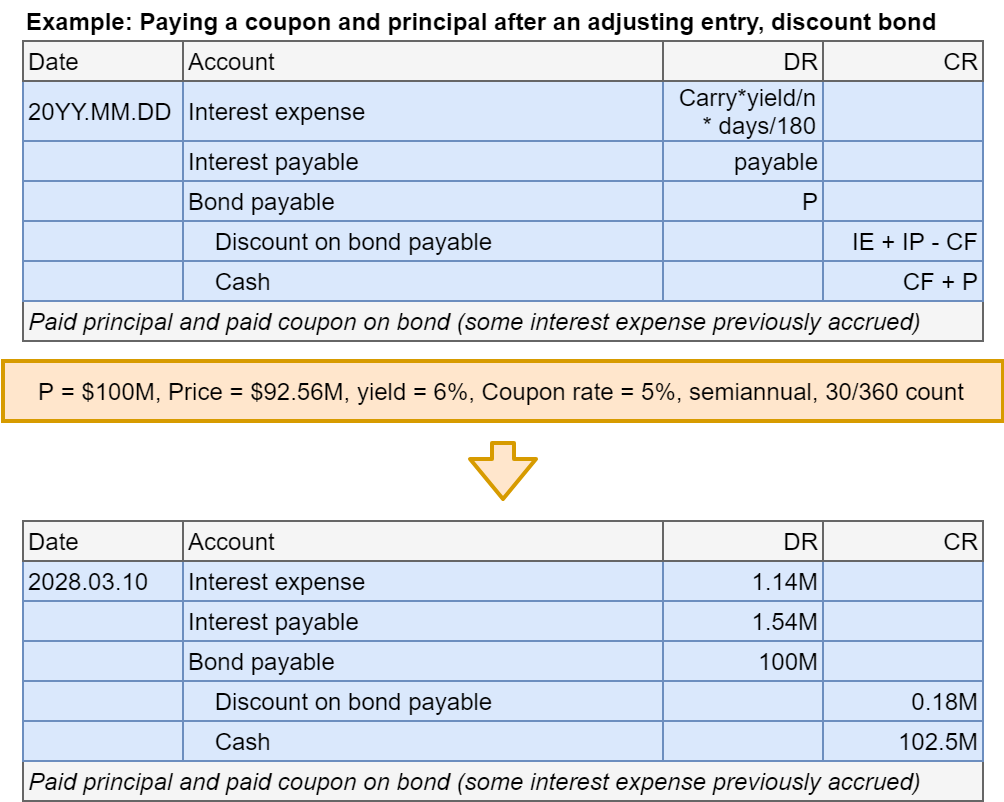

Bonds at discount: Final payment

- Step 4: In the final period, pay back the principal (and a coupon)

- You won’t be asked to figure this out without extra information

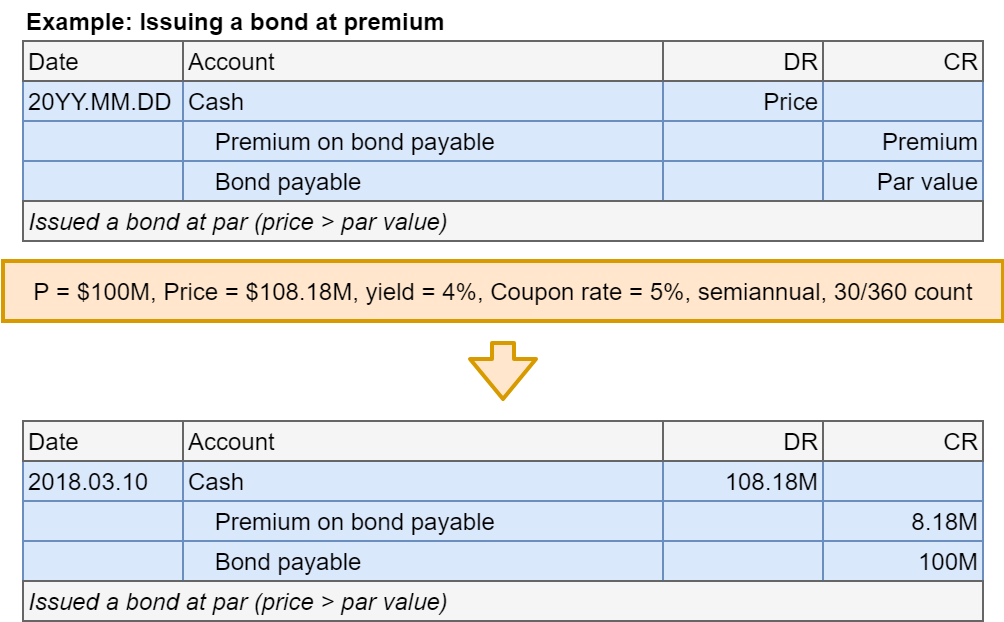

Bonds at premium: Issuance

- Step 1: Account for bond issuance

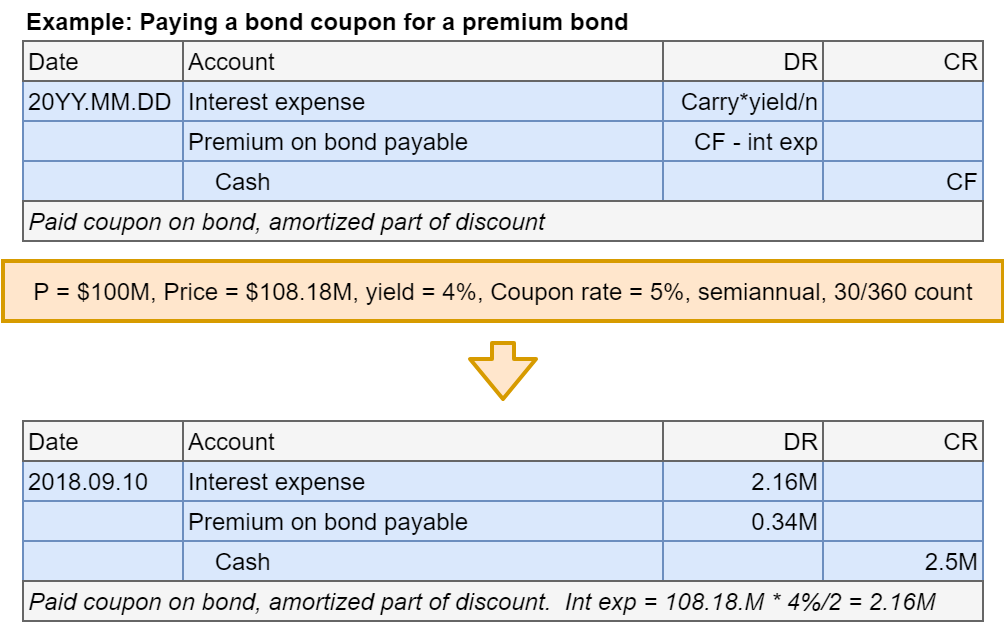

Bonds at premium: Coupon payment

- Step 2: Account for coupon payments

- Need to use the effective interest method!

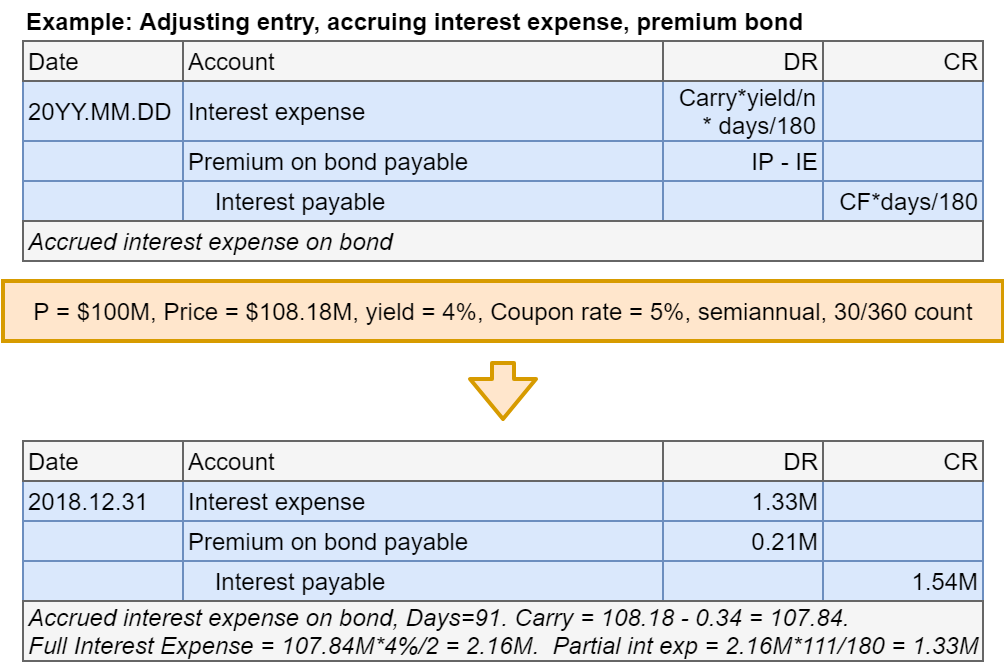

Bonds at premium: Adjusting entry

- Step 3: Account for accrued interest expense at year end

- Interest owed and interest expense will be multiplied by \(\frac{days}{180}\)

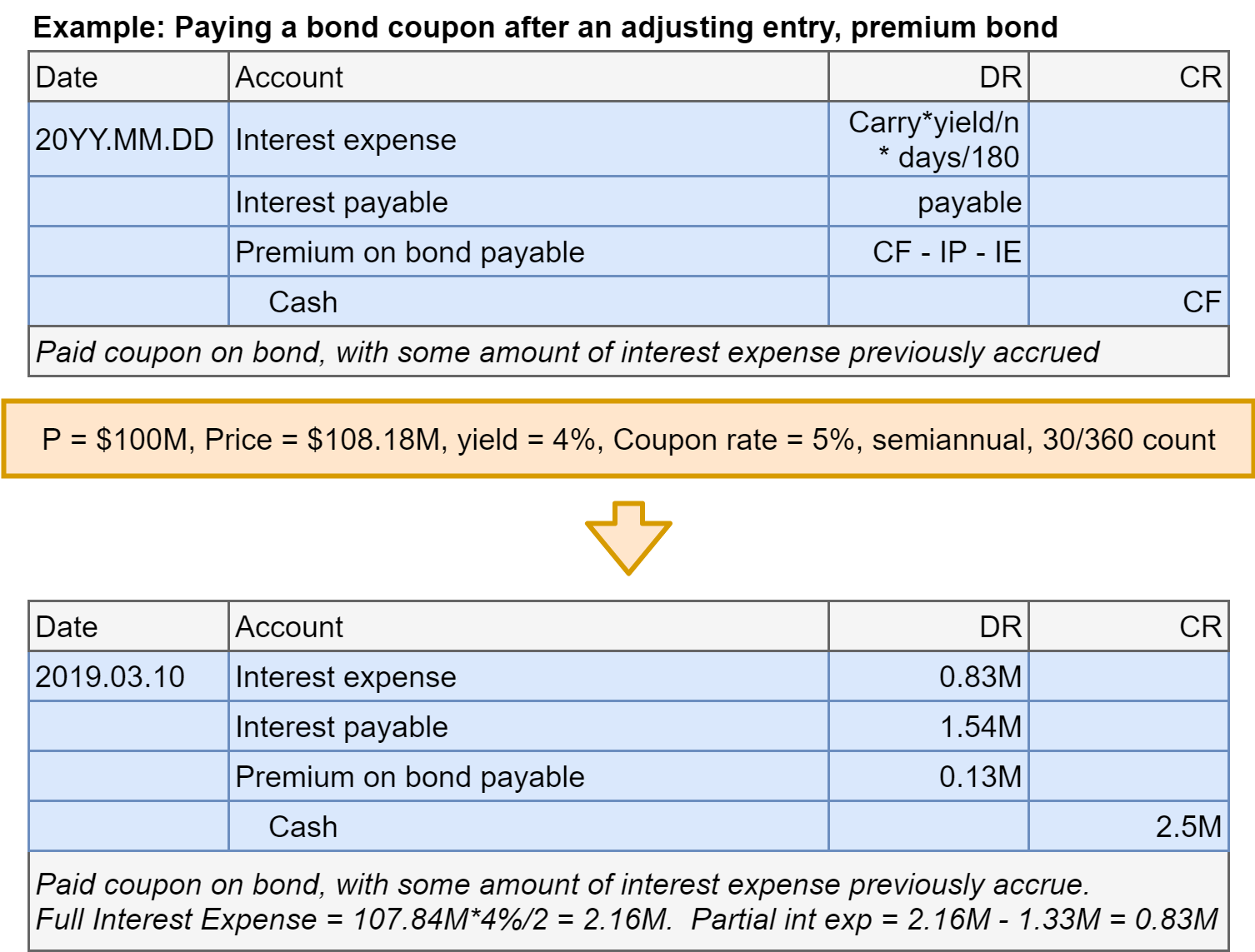

Bonds at premium: Coupon after adjusting

- Step 2 revisited: Account for coupon payments

Bonds at premium: Final payment

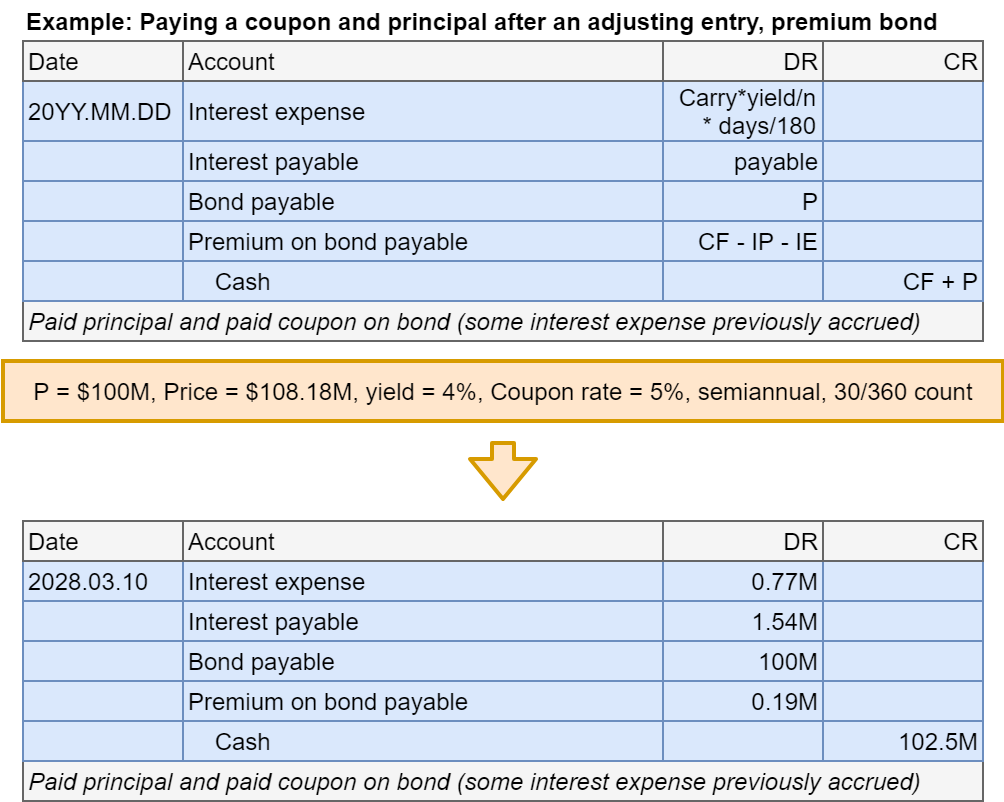

- Step 4: In the final period, pay back the principal (and a coupon)

- You won’t be asked to figure this out without extra information

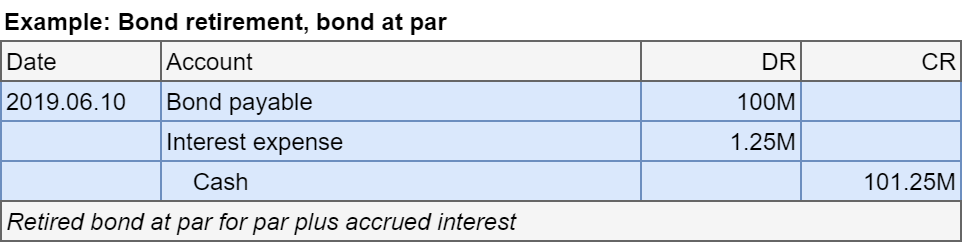

Bond retirement example: Bond at par

Suppose our example bond at par was retired after 1.25 years, on 2019.06.10, for par plus accrued interest.

- Par: $100M, Coupon rate: 5%, Yield: 5%

- Carrying value on 2019.03.10: $100M

- Accrued interest (to pay): \(\$100M \times \frac{5\%}{2} \times \frac{90}{180}=\$1.25M\)

- Accrued interest expense: \(\$100M \times \frac{5\%}{2} \times \frac{90}{180} = \$1.25M\)

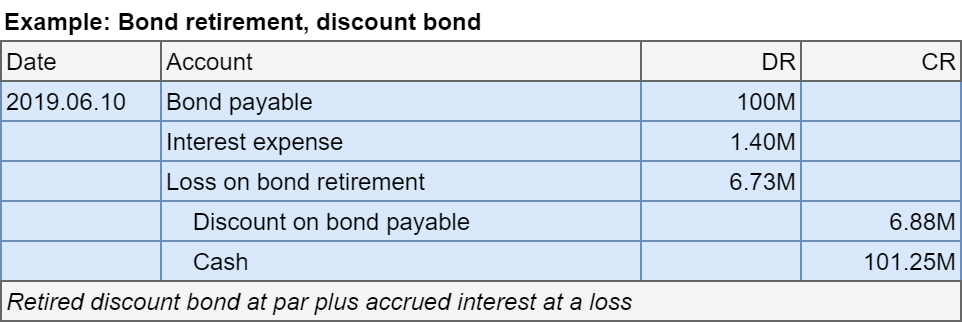

Bond retirement example: Discount bond

Suppose our example discount bond was retired after 1.25 years, on 2019.06.10, for par plus accrued interest.

- Par: $100M, Coupon rate: 5%, Yield: 6%

- Carrying value on 2019.03.10: $93.12M (discount: $6.88M)

- Accrued interest (to pay): \(\$100M \times \frac{5\%}{2} \times \frac{90}{180}=\$1.25M\)

- Accrued interest expense: \(\$93.12M \times \frac{6\%}{2} \times \frac{90}{180} = \$1.40M\)

Bond retirement example: Premium bond

Suppose our example premium bond was retired after 1.25 years, on 2019.06.10, for par plus accrued interest.

- Par: $100M, Coupon rate: 5%, Yield: 4%

- Carrying value on 2019.03.10: $107.50M (premium: $7.50M)

- Accrued interest (to pay): \(\$100M \times \frac{5\%}{2} \times \frac{90}{180}=\$1.25M\)

- Accrued interest expense: \(\$107.50M \times \frac{4\%}{2} \times \frac{90}{180} = \$1.07M\)