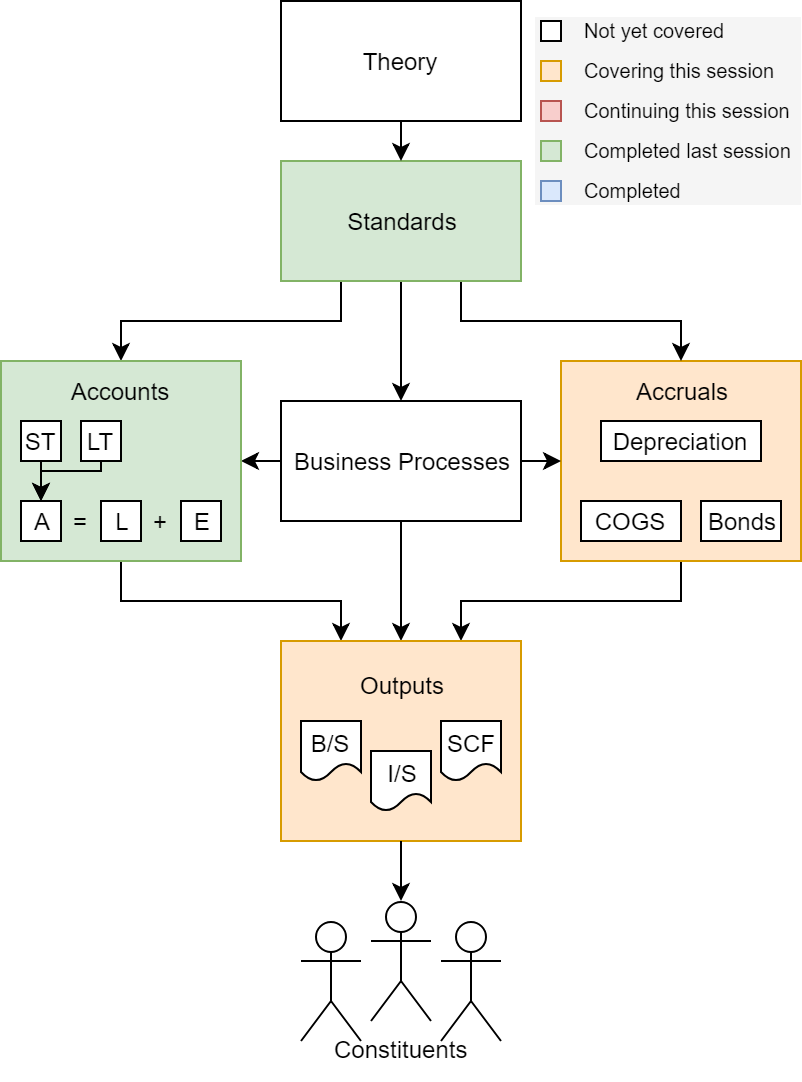

Learning objectives

- Bookkeeping (Chapter 2)

- Understand how accounting works

- Record transactions in the journal

- Construct a trial balance

- Accruals and Adjustments (Chapter 3)

- Relate accrual accounting and cash flows

- Apply the revenue and matching principals

- Adjust accounts

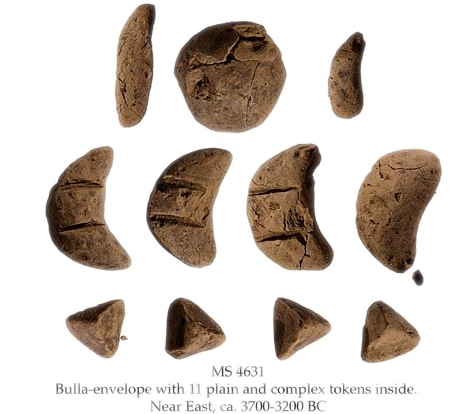

History: Before double entry

- 8500 BCE: Shaped clay tokens represent commodities

- 200 BCE: Arabic numerals (except 0)

- 600 CE: 0 developed

- 800 CE: 10-digit numerals spread throughout Europe

*Note: This slide is based on a history lecture by Dr. Pierre Liang at Carnegie Mellon from October 2017

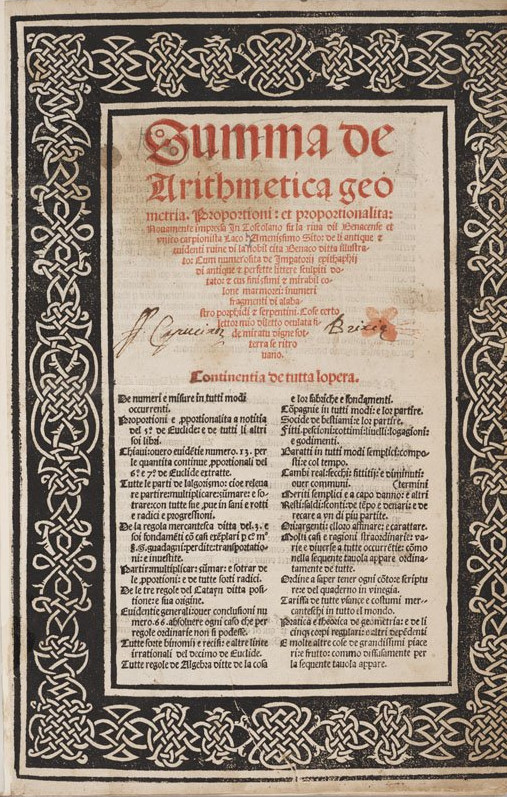

History: Double entry

- 1400s CE: First evidence of double entry accounting in Italy

- 1494 CE Italian monk and scholar Luca Pacioli publishes first text on double entry bookkeeping

*Note: This slide is based on a history lecture by Dr. Pierre Liang at Carnegie Mellon from October 2017

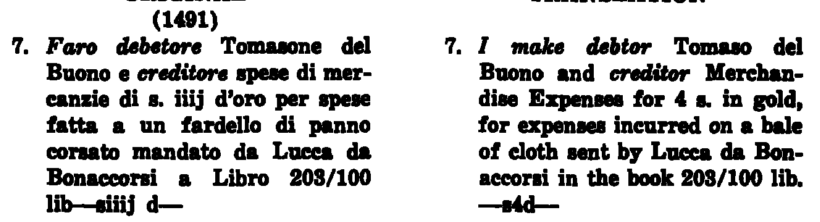

History: Journal entries

Images from Littleton 1928 TAR.

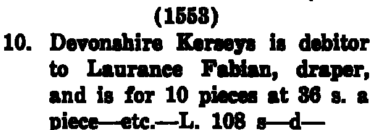

History: Journal entry evolution

Shakespeare likely did this sort of work for the British Navy! (Source: Reynolds 1974 JAR)

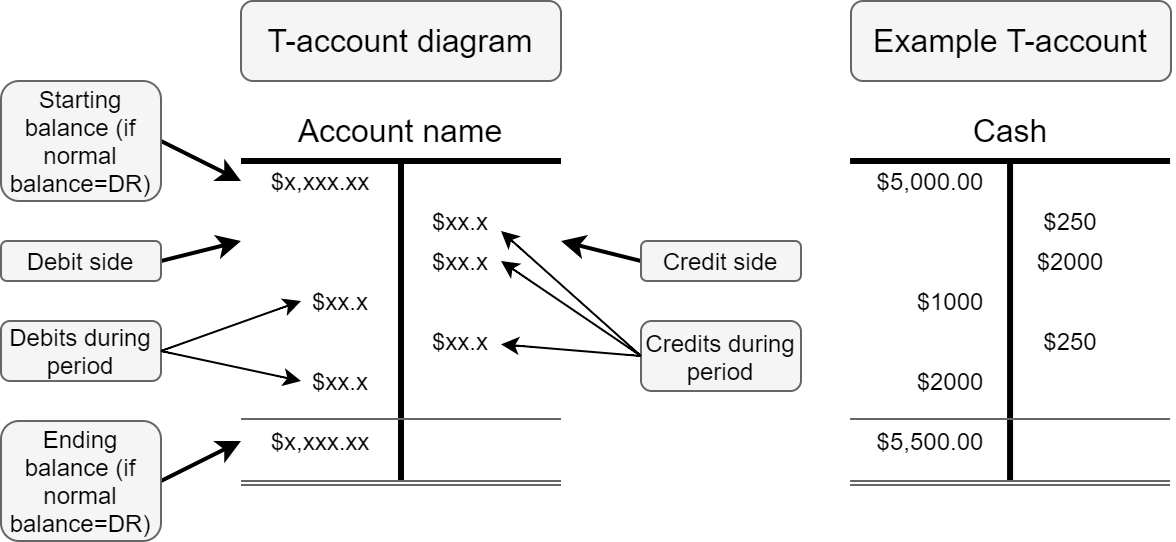

Representing accounts: T-accounts

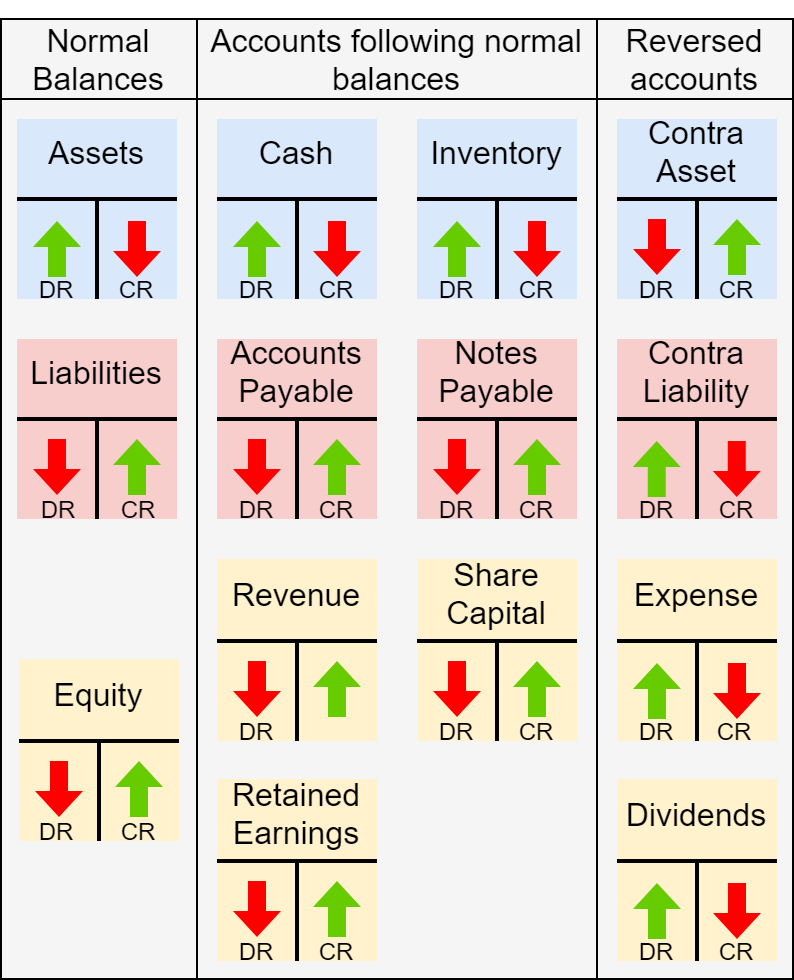

Normal balances

Accounts

- Assets: Cash, A/R, inventory, equipment, …

- Liabilities: A/P, debt, expenses payable, …

- Equities: Expenses, revenue, capital, ret. earnings, …

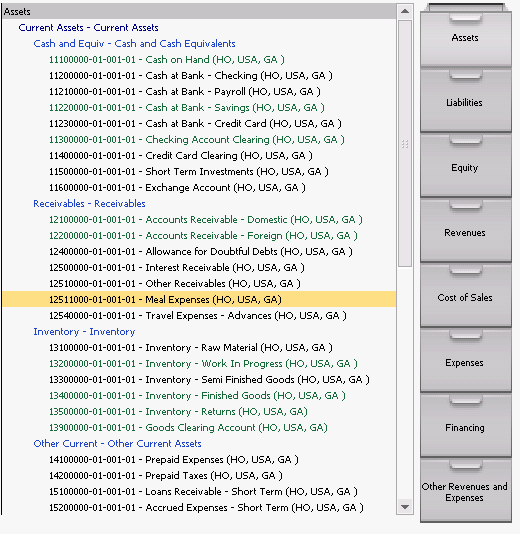

- Documented granularly in the Chart of Accounts

Source documents

- The paper trail

- Establishes amounts

- Confirms a traction occurred or was contracted

- Allows for analyzing and verifying at the transaction level

- Needed for auditing!

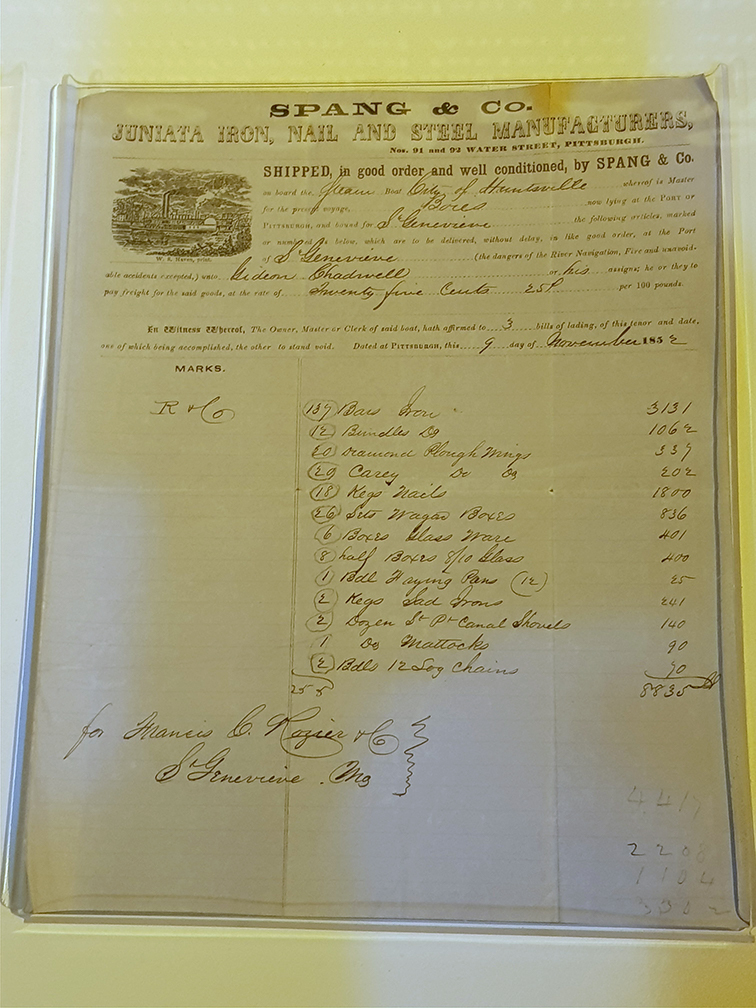

Bill of laiding, 1852

[Heinz Museum]

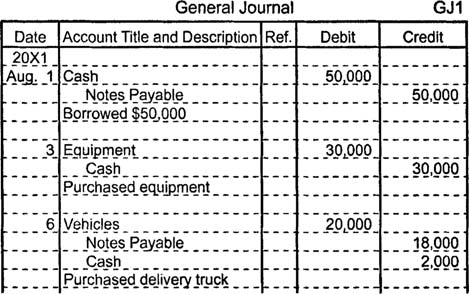

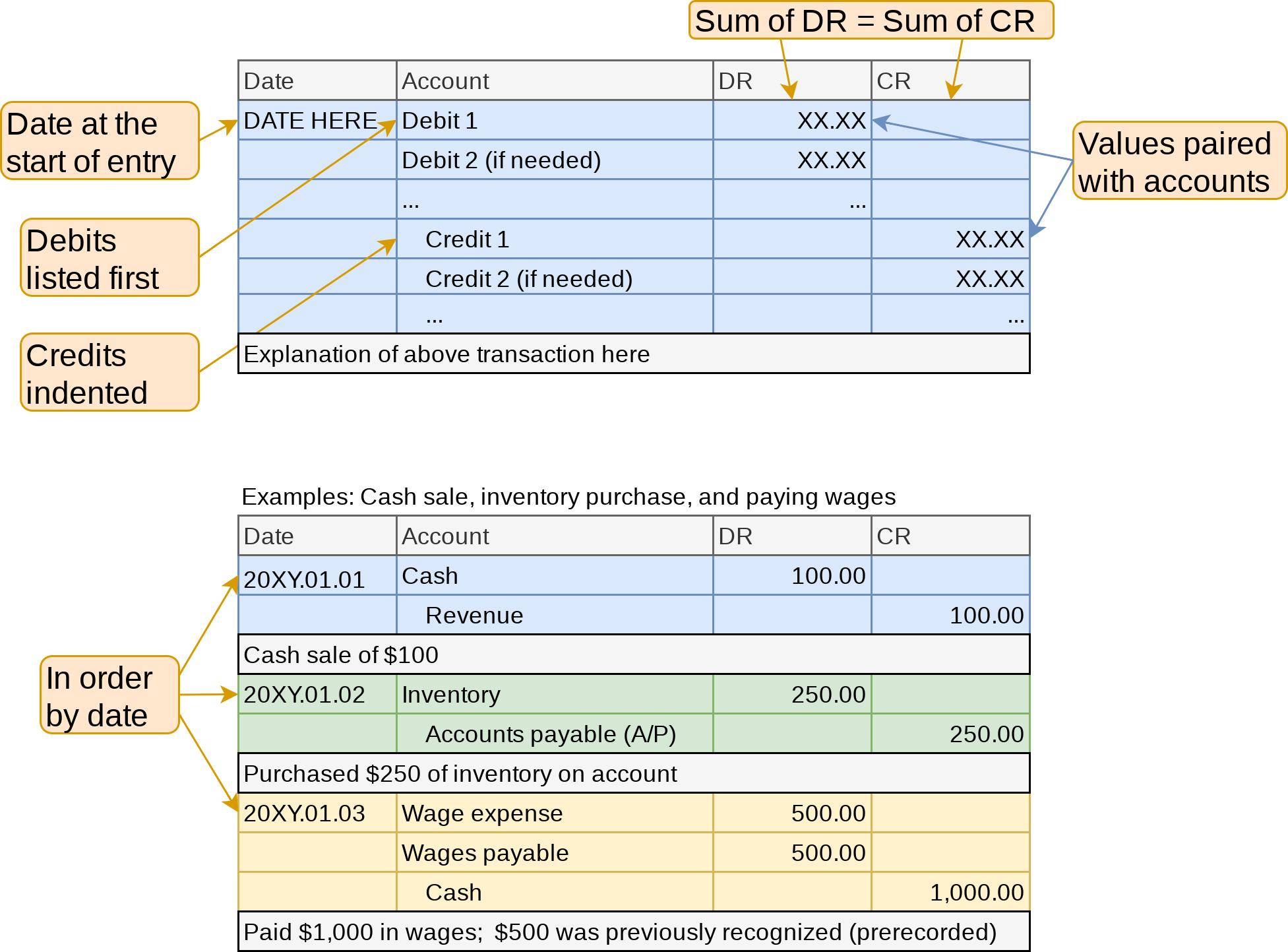

General journal

- Where everything is recorded first

- Everything

- Every little transaction

- Specifies the accounts, values, and document for each transaction

- We will skip references

- We will be doing journal entries through session 9

- Always list debits first

DR = CR for each entry

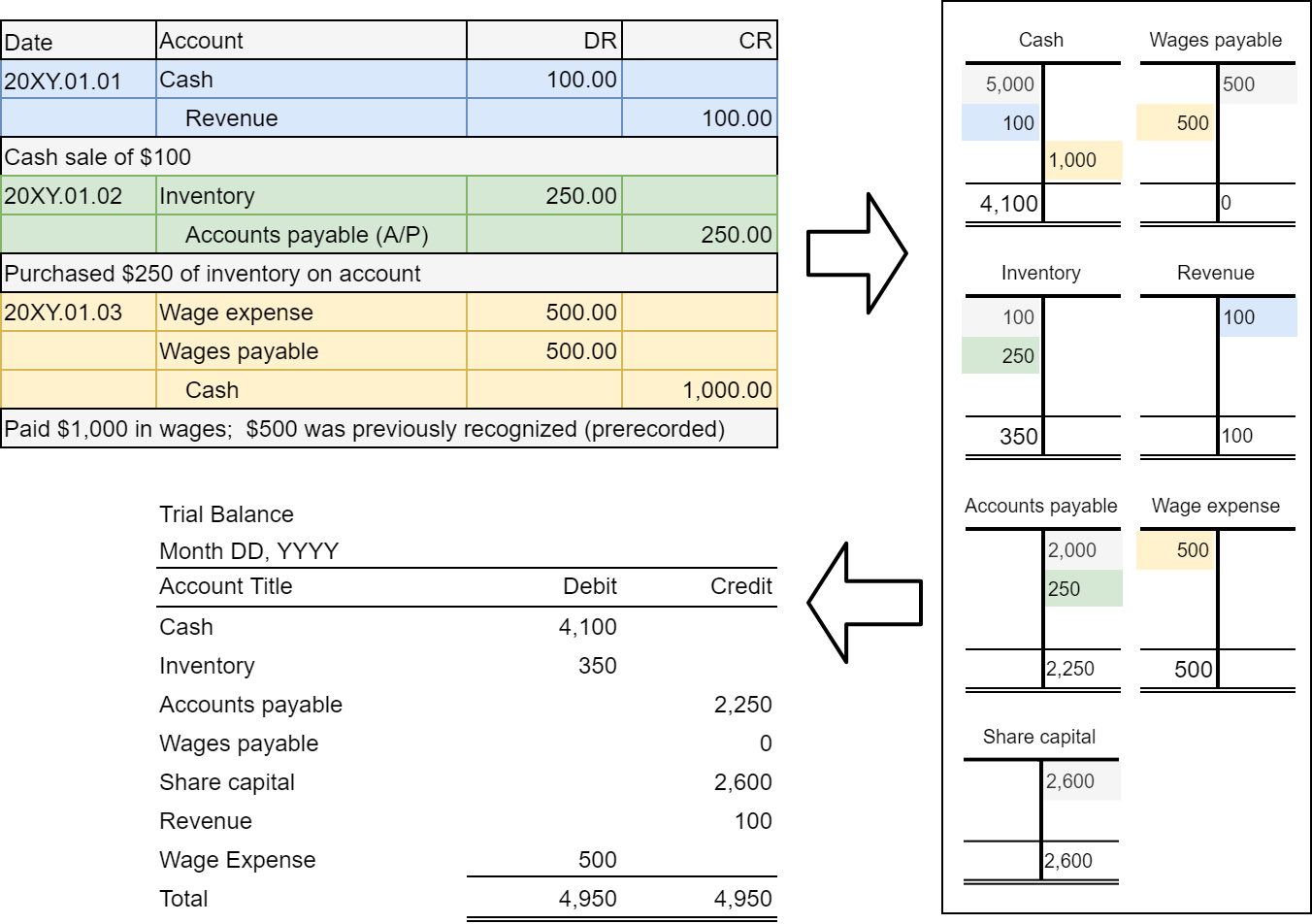

Constructing journal entries

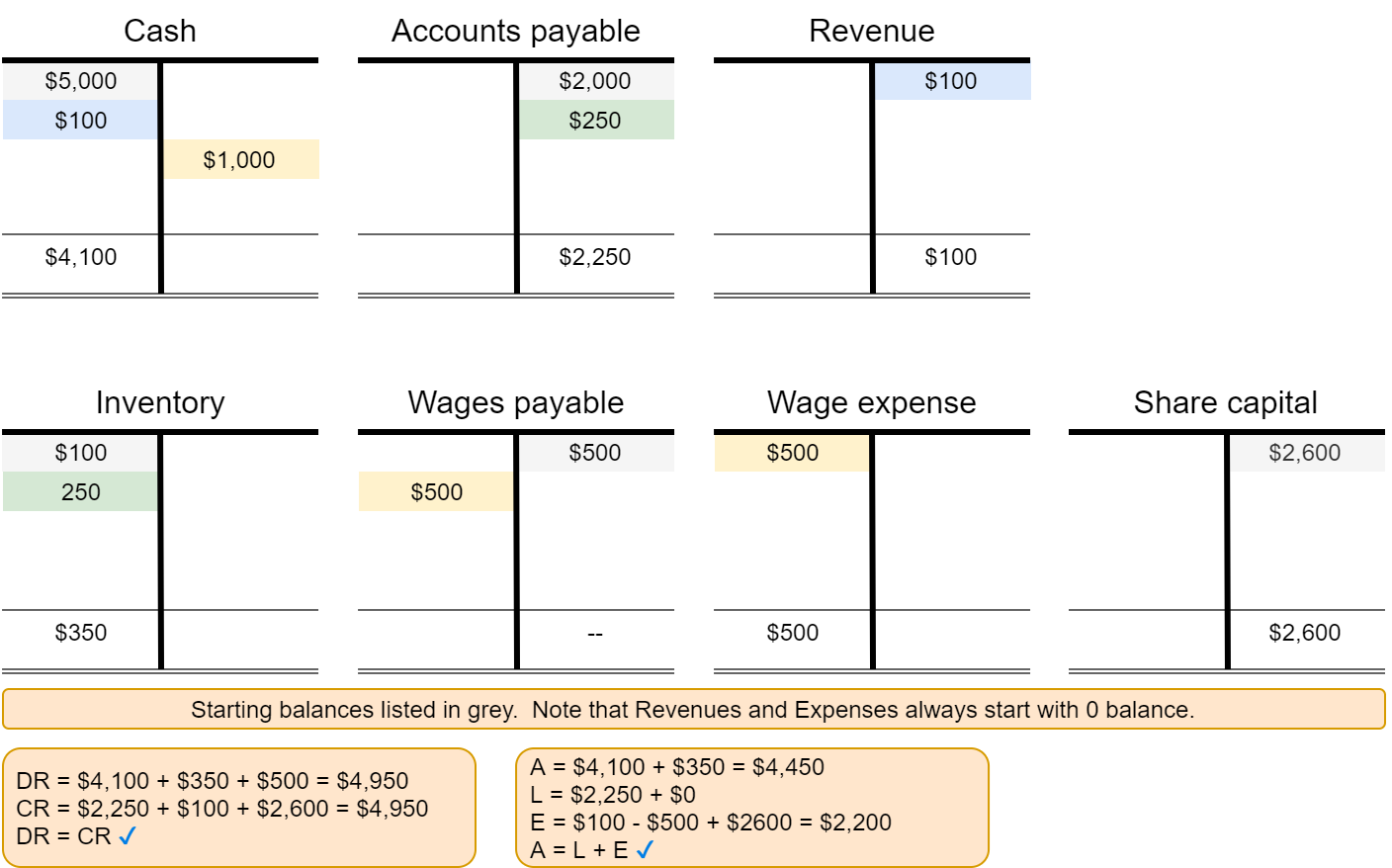

General ledger

- An aggregation of all the accounts

- Shows all account balances

- Includes details of each account

- T-accounts sufficient for this course

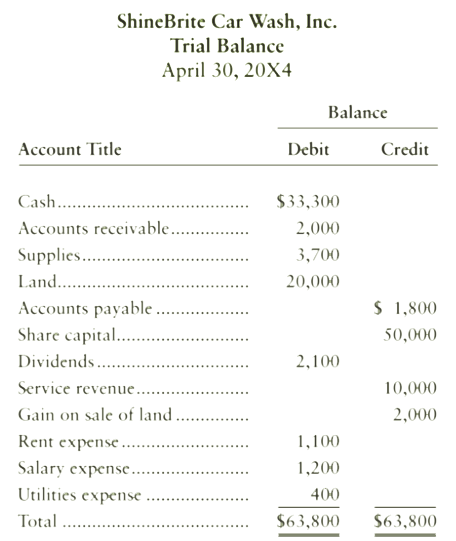

Trial Balance

- Shows all account balances just like the general ledger

- Make sure they add up!

- Use it to verify DR = CR

- Use it to verify the accounting equation

- Usually prepared at the end of a period

- Can prepare income statement and balance sheet from it

DR = CR for totals

Constructing the trial balance

Periodicity

- Divides time into artificial segments to understand a firm’s changes over time

- Fiscal year, fiscal quarter

- Breadtalk: Jan 1 - Dec 31

- Citigroup: Jan 1 - Dec 31

- Microsoft: Jul 1 - Jun 30

- Walt Disney

- 2020: Sept 29 - Oct 2

- 2019: Sept 30 - Sept 28

- 2018: Oct 1 - Sept 29

Don’t focus on this too much for this class

Expense matching

- 3 ways to match

- Directly

- The expense is easy to track to an account

- Ex.: Inventory

- The expense is easy to track to an account

- Indirectly (over a period)

- The asset has a long life or is difficult to track

- Ex.: Buildings

- The asset has a long life or is difficult to track

- With acquisition

- Simultaneous usage and acquisition

- Ex.: Utilities, rent, labor

- Often prepaid expenses

- Simultaneous usage and acquisition

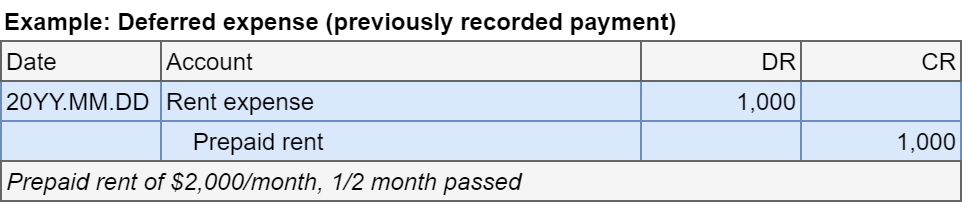

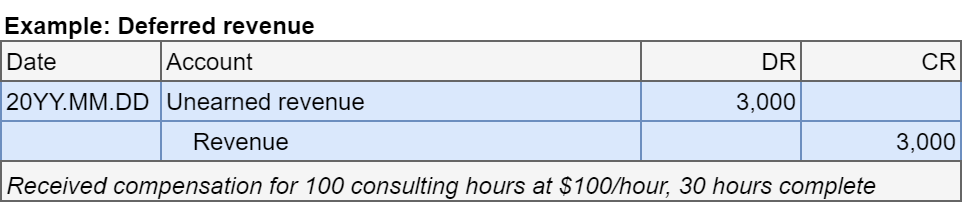

Deferral

- Adjustment for cash paid or received in advance

- Expense or revenue has yet to occur

- We defer some of it to the next period

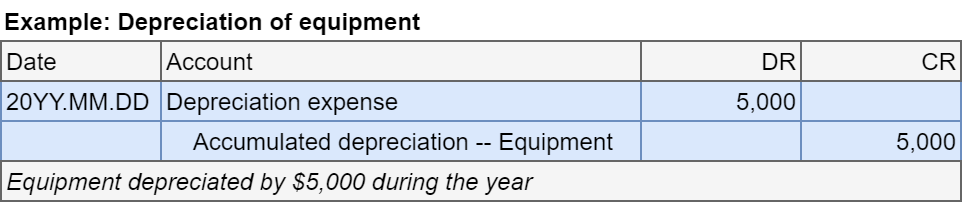

Depreciation

- Adjustment for allocating the cost of Property, Plant and Equipment (PP&E) over its useful life

- Record to accumulated depreciation

- Asset’s book value is asset account minus accumulated depreciation

- Depreciate to salvage value

- What you expect to get when it is used up

Depreciation methods

- Straight line

- Same amount each period

- If \(N\) periods, \(S\) salvage value, \(H\) historical cost:

- \((H-S)/N\) per period

- Units of activity

- Expense based on units produced

- Good if capacity is known and tracked

- Declining balance

- More depreciation early on, less later

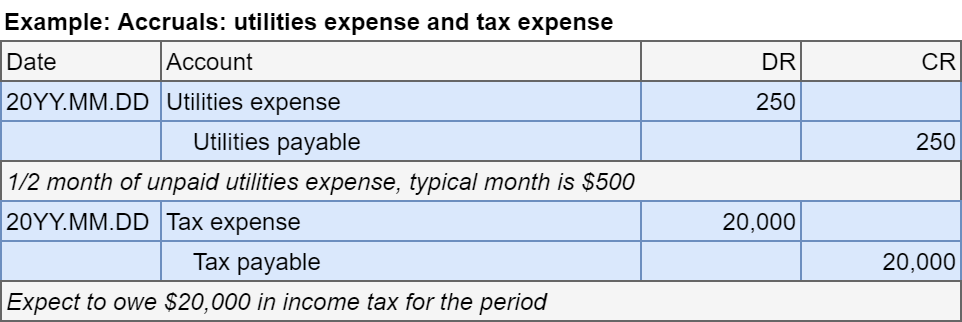

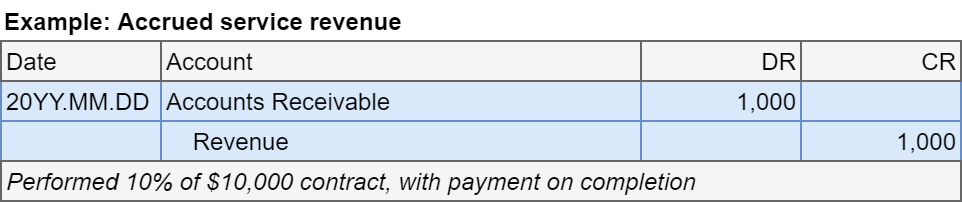

Accrual

- Accrued expense: debit expense, credit liability

- Accrued revenue: debit asset, credit revenue

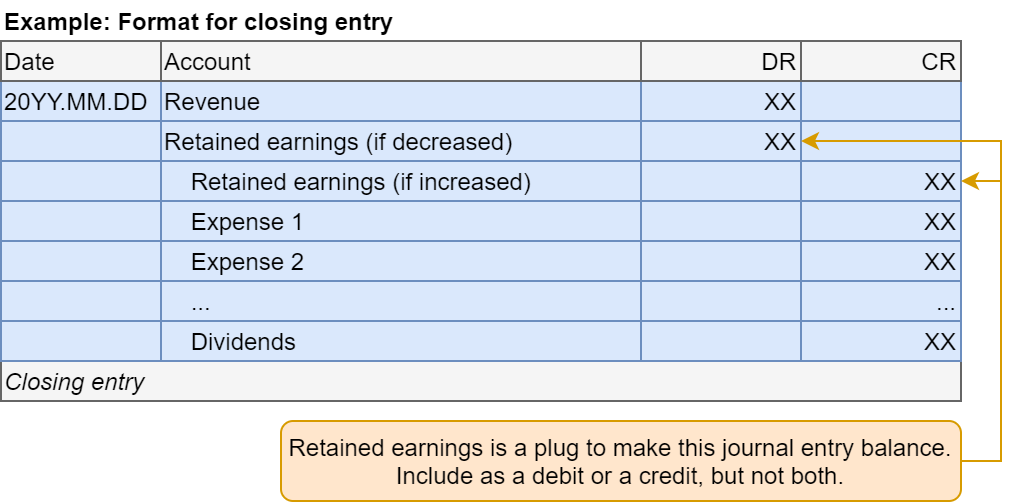

Reset temporary accounts at period end

- We close the accounts into retained earnings directly

- Or close into income summary, and then close that into retained earnings

- Debit Revenue, Credit Retained earnings

- Debit Retained earnings, Credit Expense

- Debit Retained earnings, Credit Dividends