Homework 1 Review

- Closing entries

- Accounts are: Revenues, Expenses, Gains, Losses, Dividends

- Depreciation

- (Price paid - salvage value) / [life length from purchase]

- In homework: (100,000 - 20,000) / 5 = 16,000

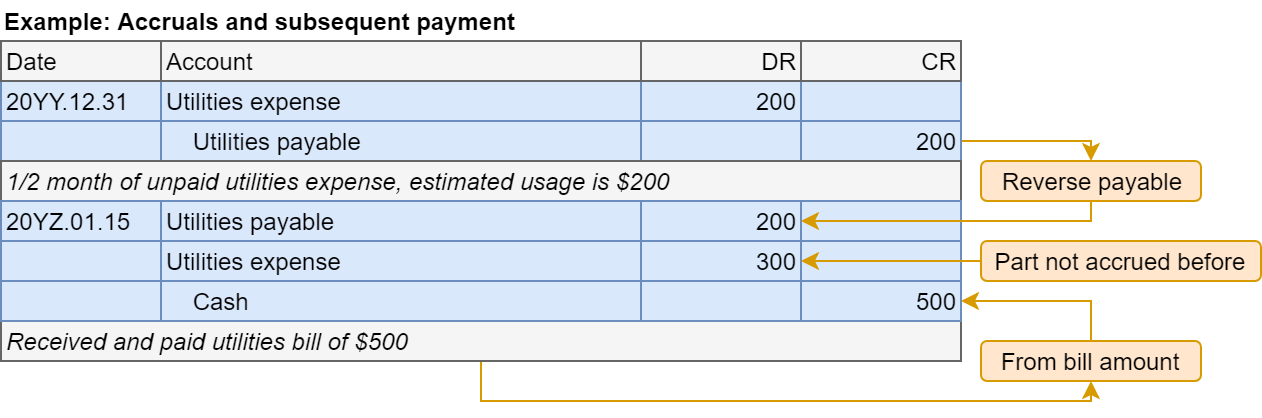

- Accrual entries:

- Bring an expense or revenue forward

- Create a payable or receivable as well

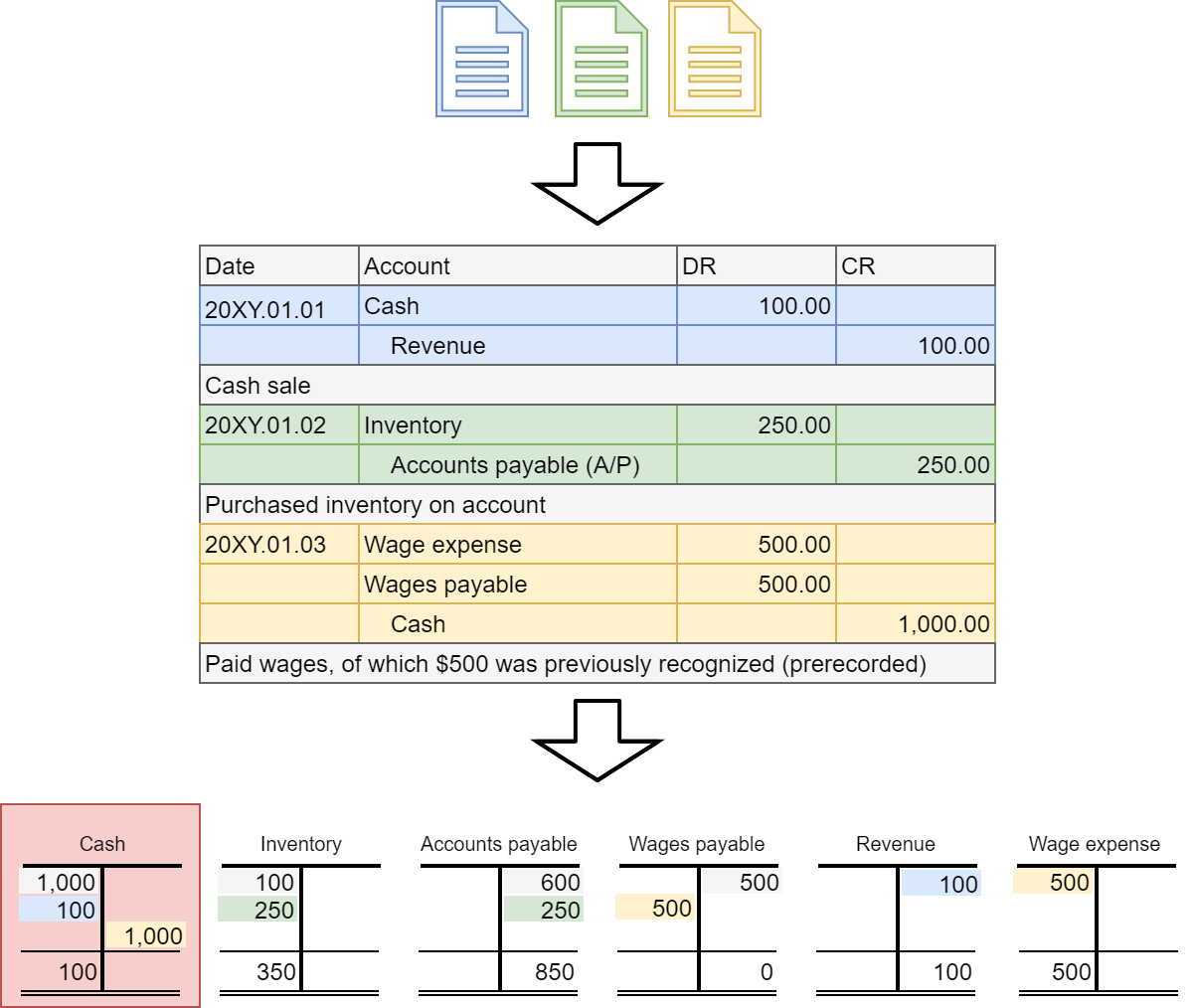

- Payable or receivable reversed upon payment

Learning objectives

Control Systems (Chapter 4)

- Understand the drivers of fraud

- Be able to identify weaknesses in firms’ systems and suggest improvements

- Be able to reconcile book and bank cash

A/R (Chapter 5)

- Understand how to write off uncollectible A/R

Misreporting: A simple definition

Errors that affect firms’ accounting statements or disclosures which were done seemingly intentionally by management or other employees at the firm.

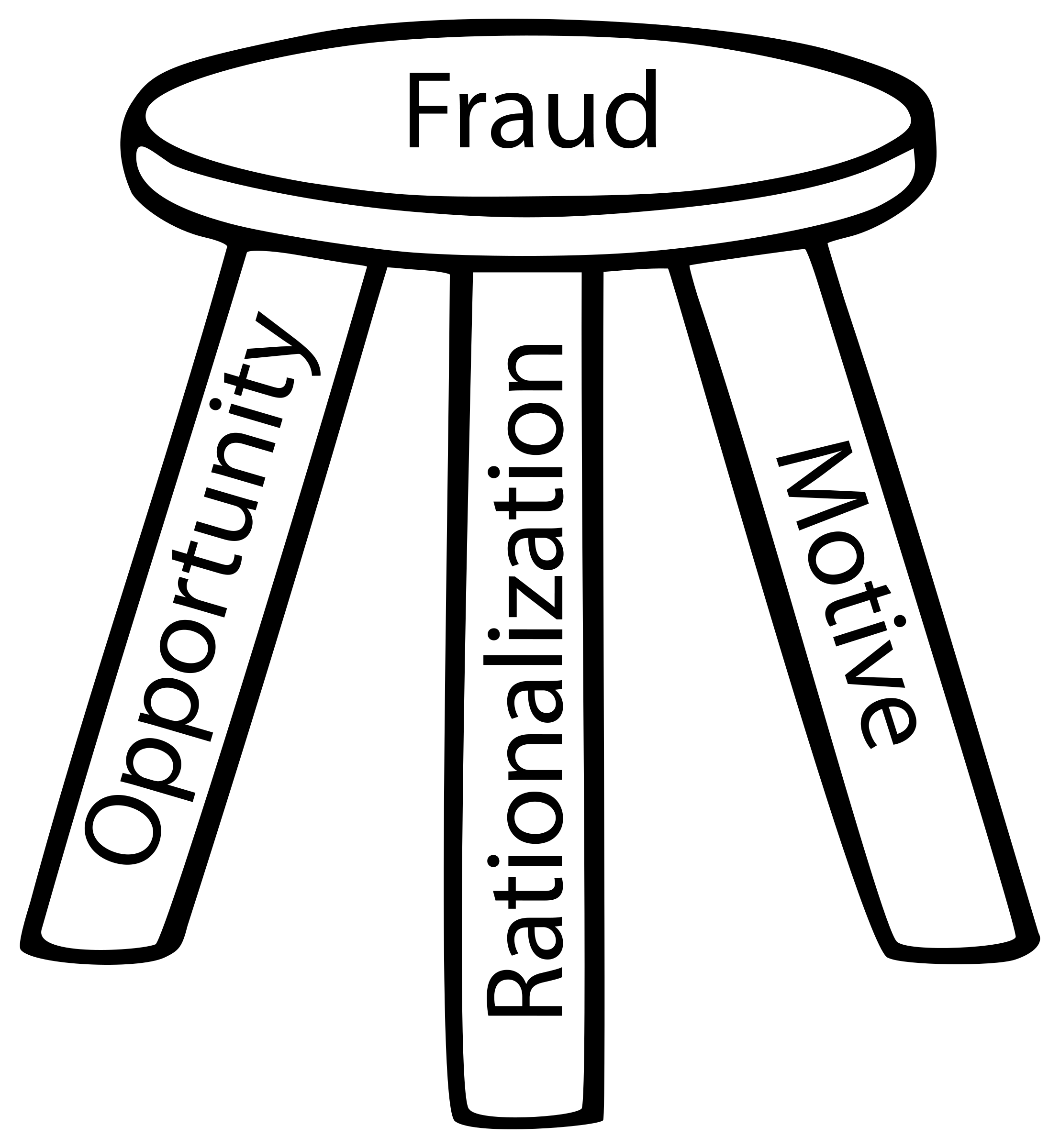

Fraud triangle

- Opportunity

- Hole in the control system

- Profitably exploitable

- Rationalization

- Resentment of corporation

- Poor culture

- “Borrowing”

- Motivation

- Family needs

- Maintaining lifestyle

- Maintaining performance

Need all 3 for fraud to happen

Champaign Parking Enforcement

Their Objectives

- Validity: All recorded transactions ocurred

- Completeness: All valid transactions have been recorded

- Valuation: Amounts measured properly

- Security: Information system protected from unauthorized access or destruction

Discussion questions

- What are some risks that threaten these objectives?

- How frequent is the risk?

- How serious is the risk?

- How could they be addressed?

Cash on companies’ books

Documents:

- Purchase orders

- Invoices for purchases/sales

- Checks

- Payment records

- Petty cash

- Small amount set aside for small purchases

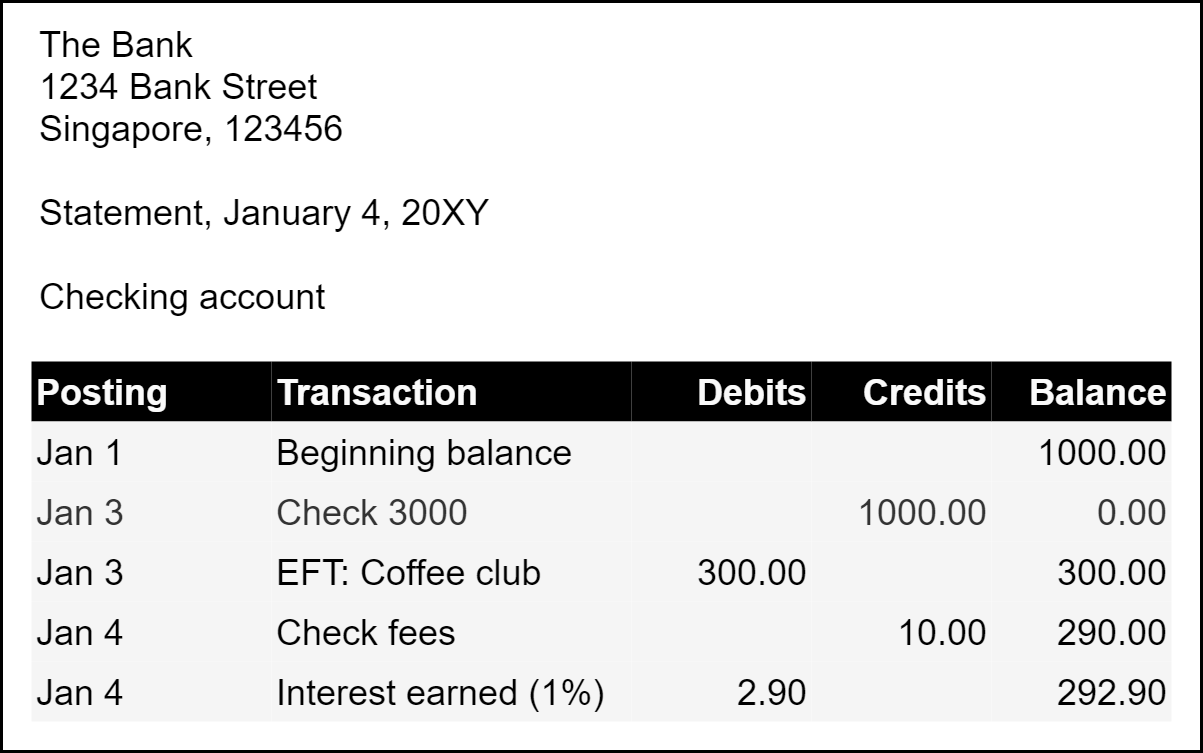

Cash in the bank

Documents:

- Cash deposits, withdrawals

- Checks

- Electronic checks

- EFT, ACH, GIRO, etc.

- Bank interest and fees

- Nonsufficient funds

- Customer’s check is rejected

- Check writer didn’t have enough cash in the bank

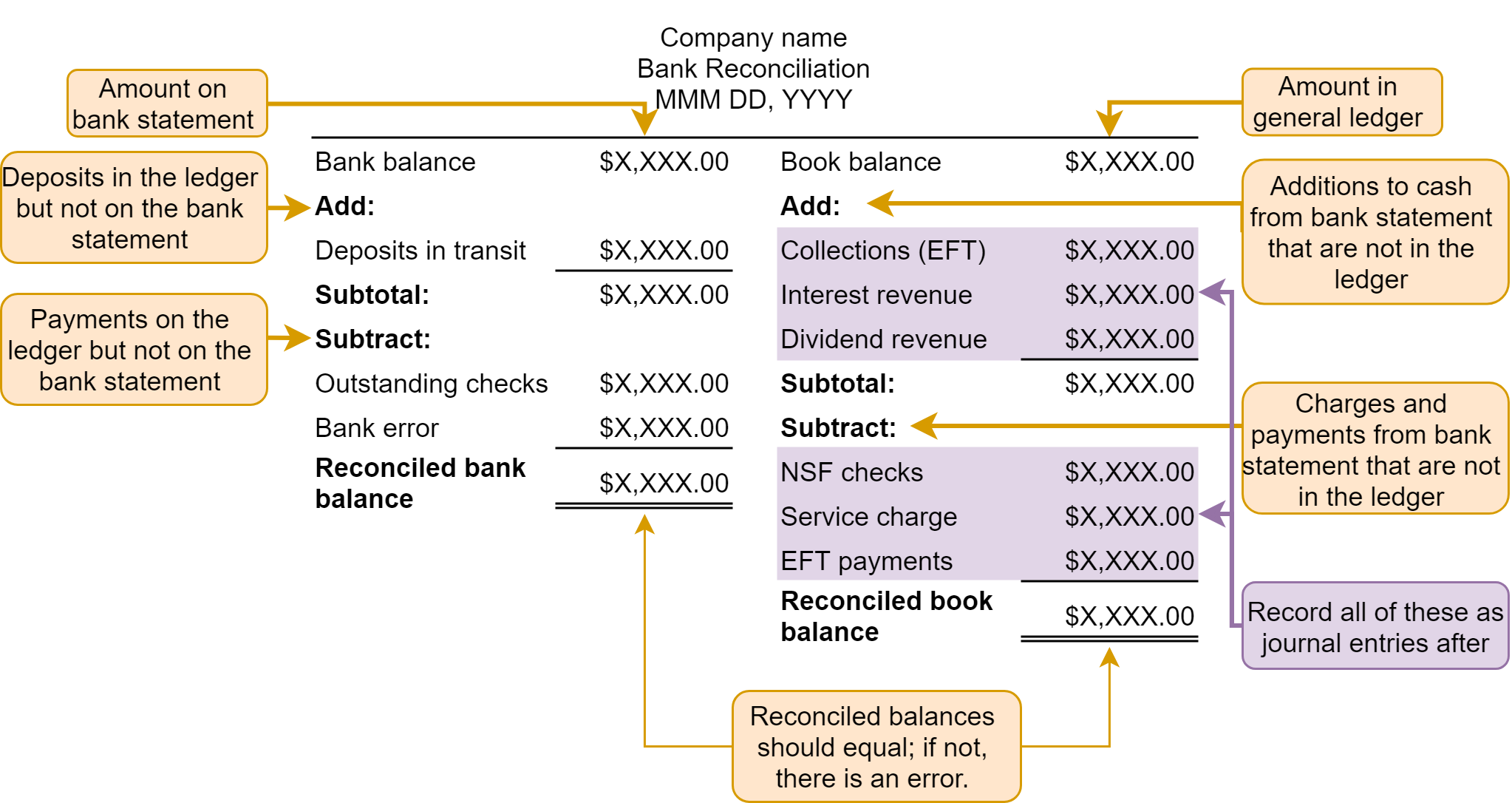

Reconciliation process

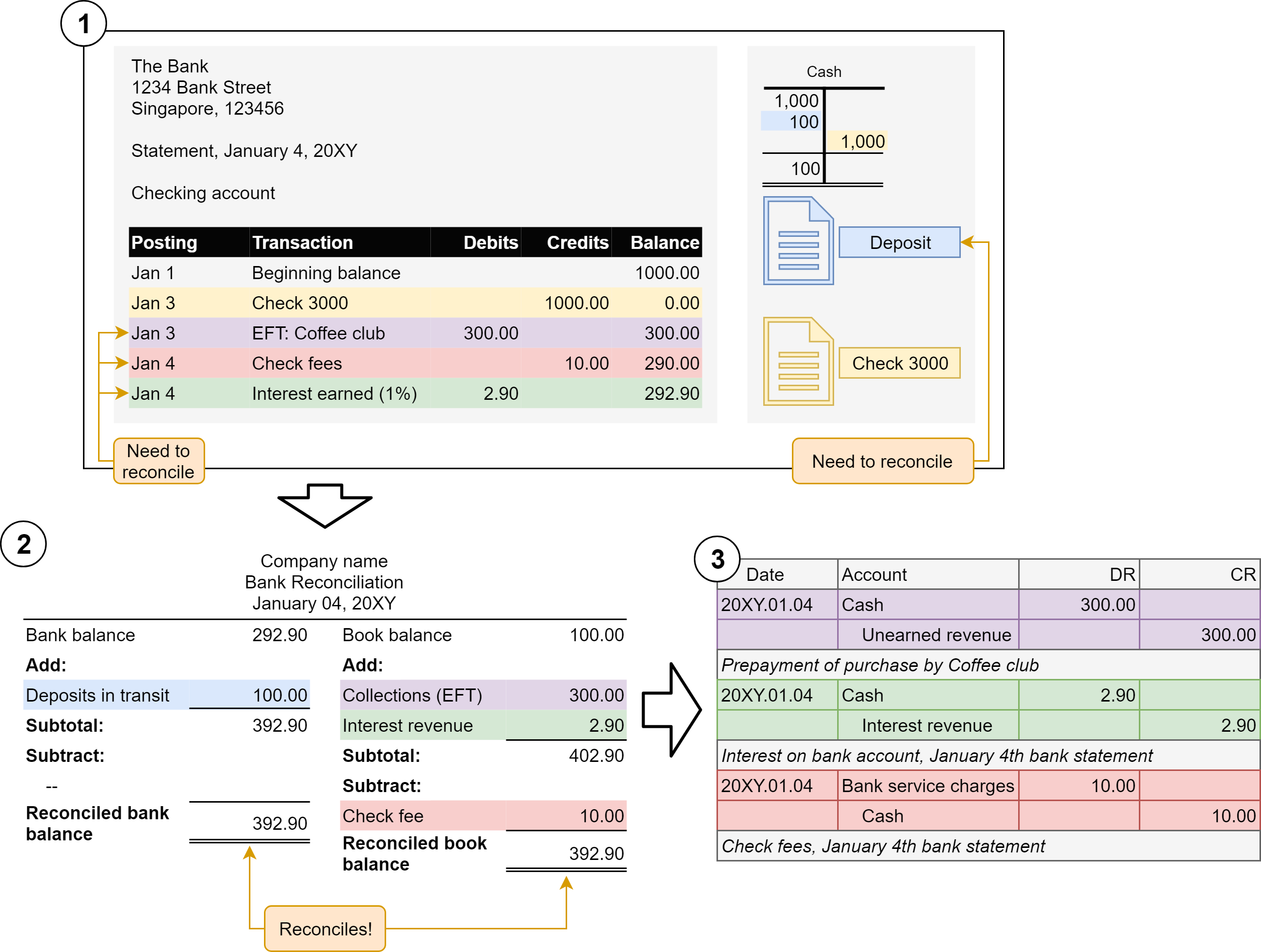

Reconciliation example

Why have uncollectible accounts?

- Case: Hanjin shipping

- Read: rmc.link/101class4

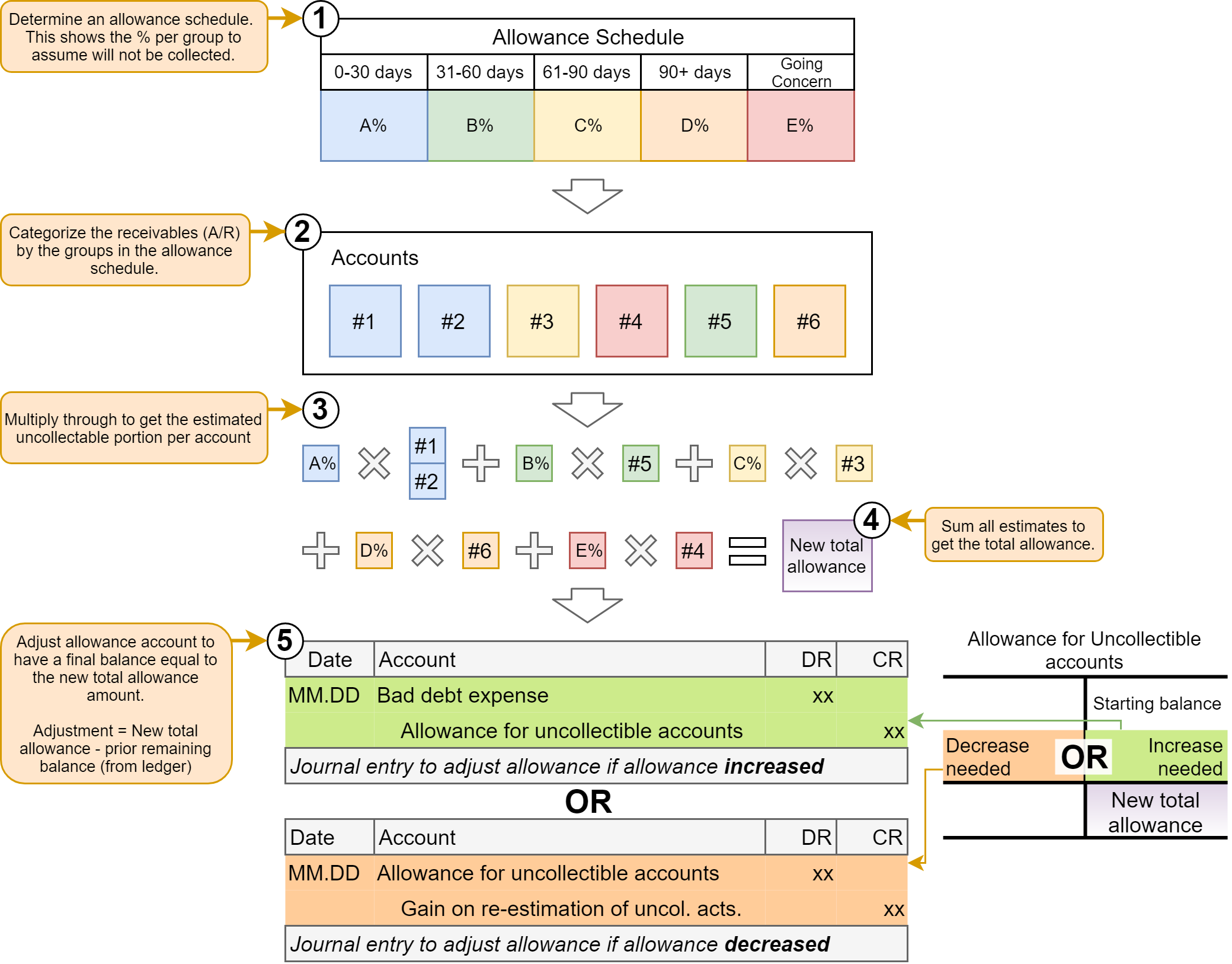

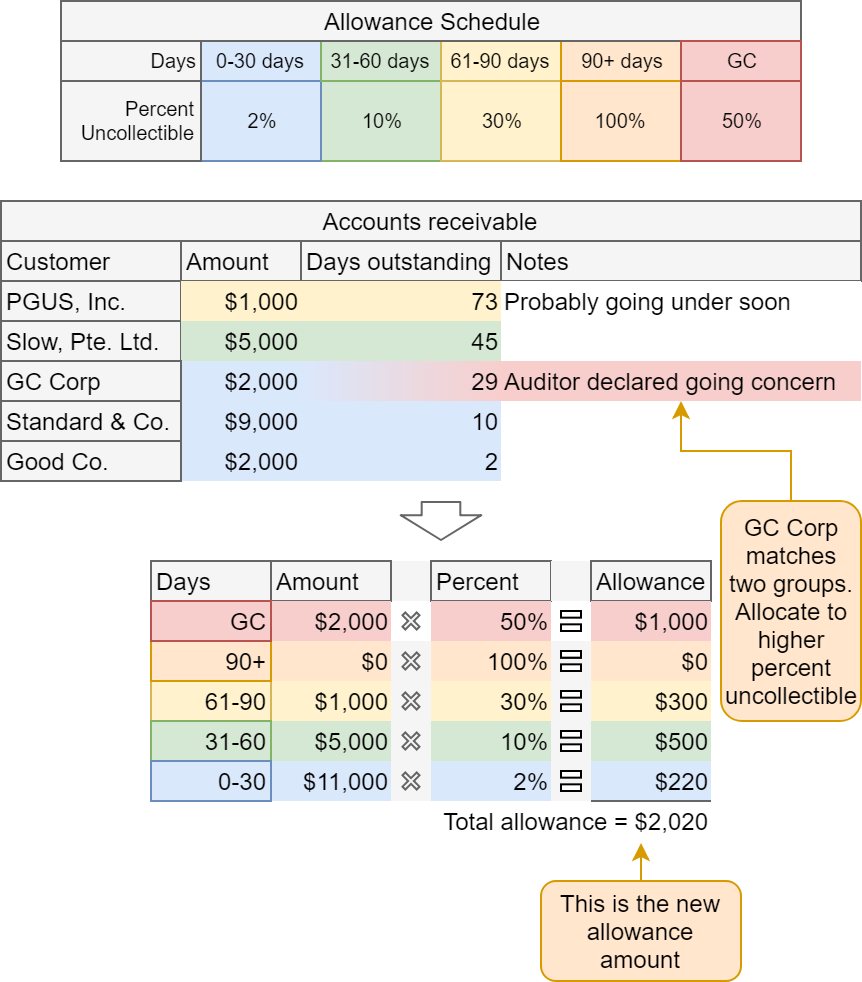

A/R allowance process

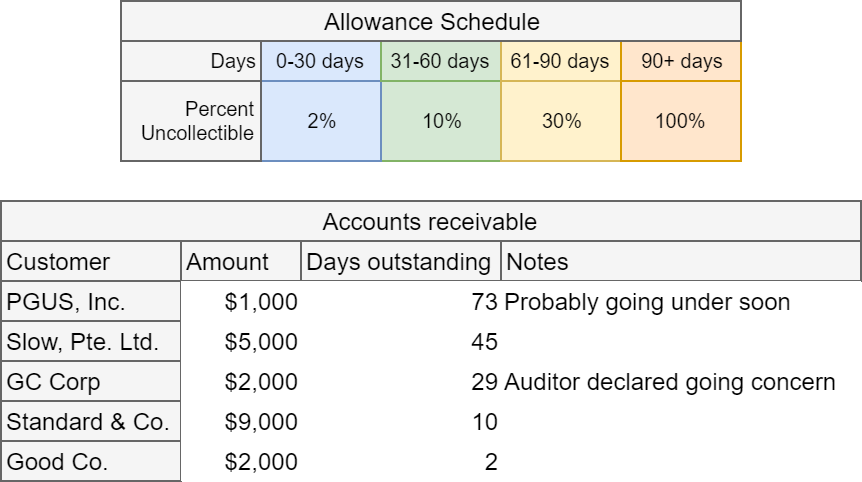

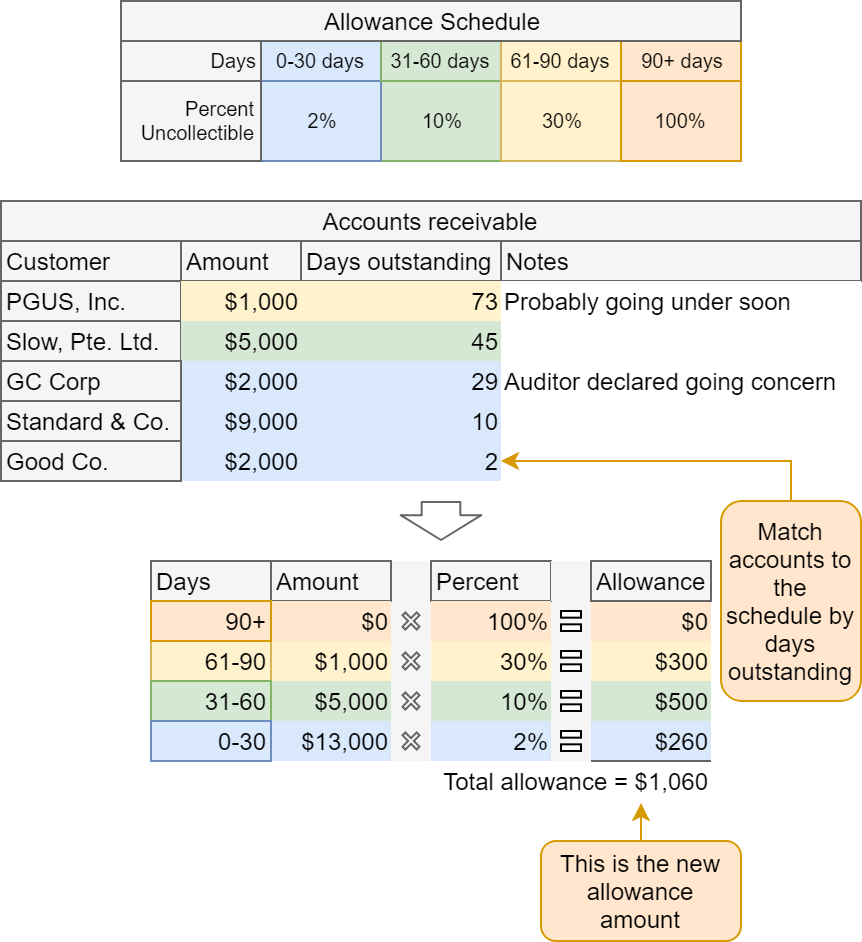

A/R allowances example

- Suppose we have the following allowance schedule and accounts receivables outstanding at year end

- What should our allowance be?

A/R allowances example

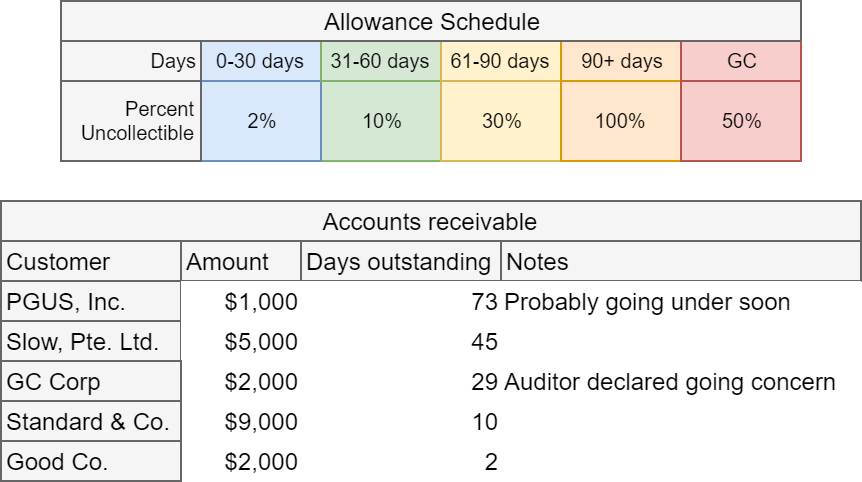

A/R allowances example: Going concern

- What about GC Corp?

- The auditor issued a going concern opinion

- High chance of bankruptcy

- Let’s update the allowance schedule for that:

A/R allowances example: Going concern

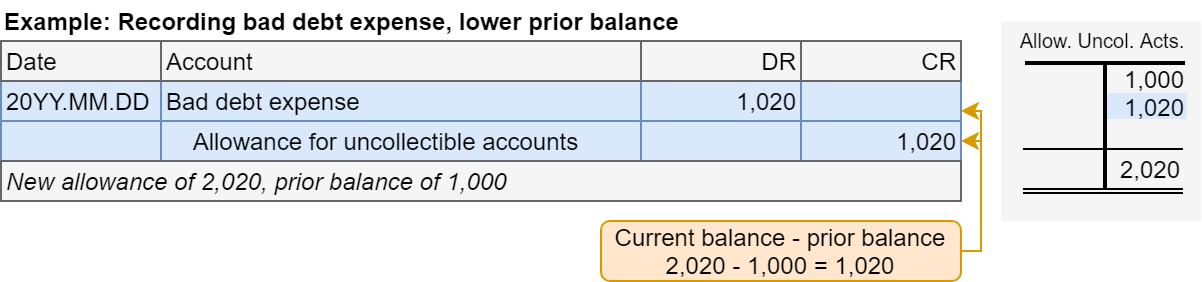

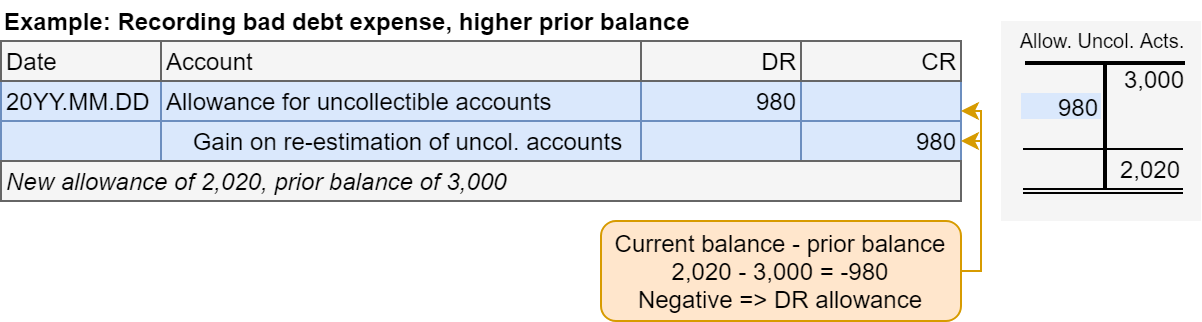

A/R allowances example: Journal entries

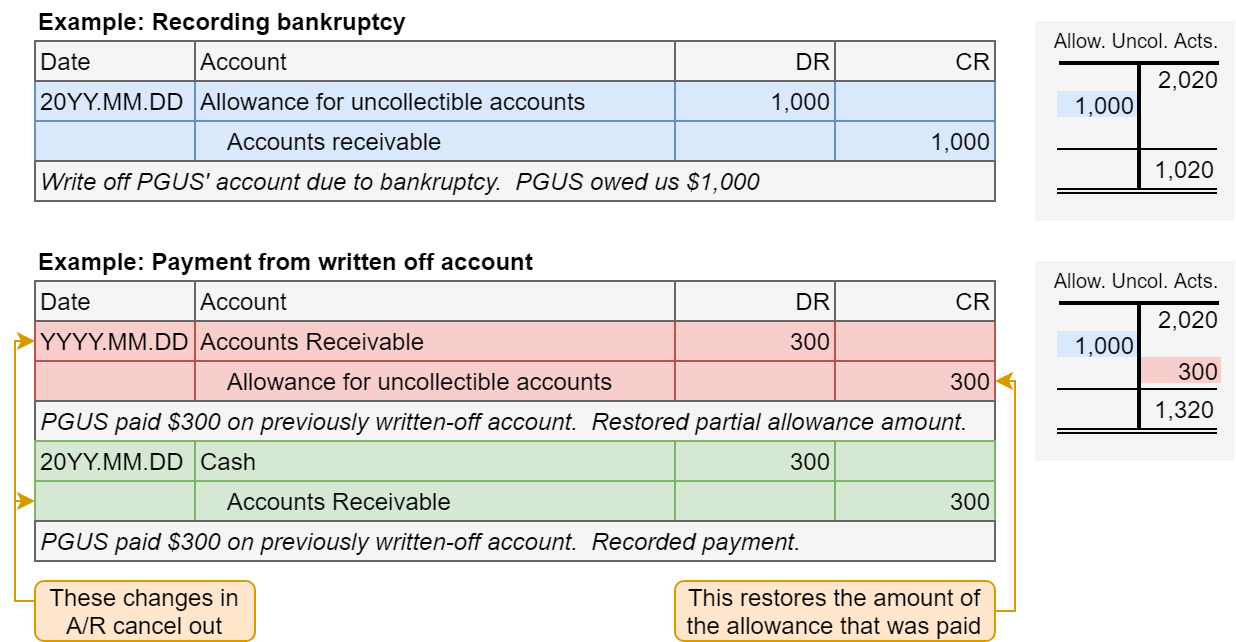

A/R allowances example: Bankruptcy

- Bankruptcy follows the direct write-off method

- We record it when it happens

- Use up some of the allowance (DR), decrease our A/R (CR)

- If the firm recovers, we reverse this transaction

- Example: PGUS goes bankrupt. During bankruptcy they pay us $300, and we expect no further payments from them.