ACCT 101: Welcome and intro to FA

Session 1

Dr. Richard M. Crowley

rcrowley@smu.edu.sg

http://rmc.link/

About Me

Teaching

- At SMU since 2016

- What I teach:

- ACCT 101, Financial Accounting

- ACCT 420, Forecasting and Forensic Analytics

- ACCT 703, Analytical Methods in Accounting (Theory)

- IDIS 700, Machine Learning for Social Science

- Before SMU: Taught at the University of Illinois Urbana-Champaign while completing my PhD

![]()

Research

- Accounting disclosure: What companies say, and why it matters

- Focus on social media and regulatory filings (e.g., annual reports)

- Approach this using AI/ML techniques

- Methodology for Natural Language Processing in social science

Research highlights

- The most effective published method for financial misreporting detection (uses text of annual reports).

- Multiple projects on Twitter showcasing:

- How companies are more likely to disclose both good and bad information than what is normal or expected

- That CSR disclosure on Twitter is not credible

- That executives’ disclosures are as important on Twitter as their firms’ disclosures

- Newer work on

- COVID-19 reactions worldwide

- Sentiment and understandability of accounting and finance text

- Misinformation laws (e.g., POFMA)

The above all use some sort of machine learning or text analytics approach.

About this course

What will this course cover?

- Basic elements of FA

- FA statements

- Income & Balances

- Cash flows

- Financial accounting rules

- Complex transactions

- Financial statement analysis

Teaching philosphy

- Accounting is best learned in a seminar style

- Less lecture, more thinking

- Working with others greatly extends learning

- If you are ahead:

- The best sign that you’ve mastered a topic is if you can explain it to others

- If you are lost:

- Gives you a chance to get help and catch up

- If you are ahead:

Grading

- Standard SMU grading policy

- Participation @ 10%

- Homework @ 10% (equally weighted)

- 2 quizzes @ 7.5% each

- Group project @ 15%

- Final exam @ 50%

Participation

- Come to class

- If you have a conflict, email me

- Excused classes do not impact your particpation grade

- Excused quizzes add to the final’s weighting

- If you have a conflict, email me

- Ask questions to extend or clarify

- Answer questions and explain answers

- Give it your best shot!

- Help those in your group to understand concepts

- Present your work to the class

Actively learn & learn from others

Outside of class

Homeworks

- Only 10% because they are for learning

- Submit on eLearn

- Reinforce lesson

- Apply to the real world

- Useful after graduation

- Answers are expected to be your own work

- No sharing answers

- Automatically checked by eLearn

Practices

- For you to practice material

- Not required, no direct impact on grades

- Can do in study groups, individually, etc.

- All practices are on eLearn

- Automatically graded for quick feedback

- These questions are easier than exam questions

Quizzes

- Why?

- Reinforce what you have learned

- Early progress indicator

- What to expect?

- 1 hour each

- Context based

- Long format

- Extracting information from a situation

- Problem solving

Group project

- What to expect

- 1 case per group covering a recent or ongoing accounting issue

- Groups of 4-5, fairly assigned

- Why?

- Brings course material to a real context

- Helps develop soft skills

- Learn about many real world situations

Final exam

- Why?

- Ex post indicator of attainment

- How?

- 3 hours

- Long format (like quizzes)

- Potentially some MCQ

- Same exam across all sections

Expectations

In class:

- Participate

- Ask questions

- Clarify

- Add to the discussion

- Answer questions

- Work with classmates

- Ask questions

Out of class

- Check eLearn for course announcements

- Read in advance of class

- This will help a lot

- Do homeworks on your own

- Submit on eLearn

- Do practices on your own or in groups

- Office hours and TA hours are there to help!

- Short questions can be emailed instead

Textbook

Spiceland, Thomas and Herrmann

Financial Accounting, 5th edition, McGraw Hill.

A decent textbook, but consider my slides to be more reliable.

For this semester: You can alternatively use the 5th edition – I will release practice problem information for both editions

Tech use

- Laptops and other tech are OK!

- Use them for learning, not messaging

- Examples of good tech use:

- Taking notes

- Viewing slides

- Working out problems

- Group work

- Avoid:

- Watching livestreams of pandas or Overwatch

- Messaging your friends on Telegram

- Working on homework for the class in a few hours

Office hours

- TA Office hours:

- Amanda: By appointment on Telegram (see syllabus for contact info)

- Megan: By appointment on Telegram (see syllabus for contact info)

- Prof office hours:

- Bookable at rmc.link/101OH

- Short questions can be messaged to TAs or emailed to me

- I try to respond within 24 hours

\(\quad\)Office hours begin the week of Session 2

Any office hours with me should be booked using the link above.

COVID policies

Official SMU Policy

- If you are in mandated self isolation, do that

- No live streams / Zoom classes

Relaxed policy for this course:

- If you are symptomatic but not positive, you can be excused from class

- If you have completed a 7 day isolation but still feel unwell, you can be excused from class

- Live streams available for those with excused absences (see details on eLearn)

To be excused for a COVID-related absence, fill out this form: https://forms.gle/gPpDZt6cp37sY6iD8

- All requests are automatically approved (unless you hear back from me by email)

Live streams

- Due to room limitations (no camera equipment), the live stream will not capture all of the class

- All of my audio should be captured though

- Your classmates questions probably won’t be captured

- The whiteboard will probably be hard to see

- A recording may or may not be released

Livestream attendance is not required and does not count towards participation

About this course: Online classes / EPTL addendum (if needed)

General Zoom etiquette

- Keep your mic muted when you are not speaking

- 20+ mics all on at once creates a lot of background noise

- You are welcome to leave your video on – seeing your reactions helps me to gauge your learning of the course content

- If you are uncomfortable doing so, please have a profile photo of yourself

- To do this, click yourself in the participants window, click “more” or “…” and then “Edit Profile Picture”

- If you are uncomfortable doing so, please have a profile photo of yourself

- Feel free to use Zoom’s built in functionality for backgrounds

- Just be mindful that this is considered a professional environment and that online class sessions are recorded

Online sessions will be recorded to provide flexibility for anyone missing class to still see the material. It also allows you to easily review the class material.

Asking questions

- If you have a question, use the Raise Hand function

- Where to find it:

- Desktop: Click Reactions and then Raise hand

- Mobile: Under More in the toolbar

- When called on:

- Unmute yourself.

- Turn on your video if you are comfortable with it

- Ask your question.

- You are always welcome to ask follow up questions or clarifications in succession

- After your question is answered, mute your mic.

- Where to find it:

Group work on Zoom

- I will make use of the Breakout room functionality on a weekly basis

- Your group can use the “Share screen function” to emulate crowding around one laptop

- If your group is stuck or needs clarification, you can use the Ask for help function to get my attention

- I will drop by each group from time to time to check in and see how you are doing with the problem

- I may also ask your group to present something to the class after a breakout session is finished.

Groups will be randomized each class session to encourage you to meet each other. Once group project groups are set, breakout sessions will be with your group project group.

Lastly…

- I don’t expect everything to run 100% smoothly on either side, and there will be more leniency than a normal class session to account for this

- If you miss a Zoom session, please let me know the reason in advance, and then work through the recording on your own

- I always provide a survey at the end of each class session that allows you to anonymously voice anything you liked or didn’t like about a session. Do use this channel if you encounter any difficulties. Common agreed-upon problems will be addressed within 1-2 class sessions.

- The survey link is on eLearn (under the session’s folder) and will be on the last slide I present each week.

About you

About you

- Results are anonymous

Introduction to accounting

Learning objectives

- Develop a base understanding of accounting institutions

- Understand the building blocks of the accounting system

- Apply the “accounting equation”

What is accounting?

The language of business

- Measure business activities

- Ex.: Sales, wages, inventory changes, …

- Process reports into data

- For managers, investors, etc.

- Communicate results to financial statement (F/S) users

- Ex.: Statements, disclosures, press releases, …

Types of accounting

- Financial

- Provides information to external users.

- Needs to be decision relevant

- Audit fits in here

- Managerial

- Provides information to internal users

- Used for budgeting, forecasting, strategy

- Tax

- Technically a subset of financial accounting

- Used for determining tax liability

Financial accounting

How companies communicate information publicly

Audit

Looking for a needle – it may or may not be there

Managerial accounting

How companies generate and communicate information internally

Tax accounting

Pay money to save even more money

Why should we care?

“Small-business owners tend to hate accounting because it’s boring. […] The mistake they make is not thinking about how they can use certain numbers as tools to better manage where their business is headed tomorrow.”

Forms of business

- Sole proprietorship

- 1 owner, usually small service firms

- Not a legal entity

- Owner receives all profit and loss

- Partnership

- Multiple owners, at least one is a General Partner while others are Limited Partners

- Not a legal entity

- Owners receive all profit and loss

Forms of business

- Corporation

- Has a board of directors, CEO, CFO, COO, etc.

- One or more stock classes

- From Initial Public Offering (IPO) or Secondary/Seasoned Equity Offering (SEO)

- IPO: When a company first offers stock to investors

- From Initial Public Offering (IPO) or Secondary/Seasoned Equity Offering (SEO)

- Separate legal entity under corporate law

- Profit/loss goes to the company

Forms of business

Summary:

| Characteristic | Proprietorship | Partnership | Corporation |

|---|---|---|---|

| Owner(s) | One owner (proprietor) | >1 owner, at least 1 general partner (GP), may have limited partners (LPs) | Shareholders, usually many, but could be as low as 1 |

| Liability for debt | Proprietor is personally liable | GPs are personally liable, LPs are not liable | Shareholders are not personally liable |

| Tax status | Income tax passed through to owner | Income tax passed through to partners | Own legal entity, corporation taxed directly |

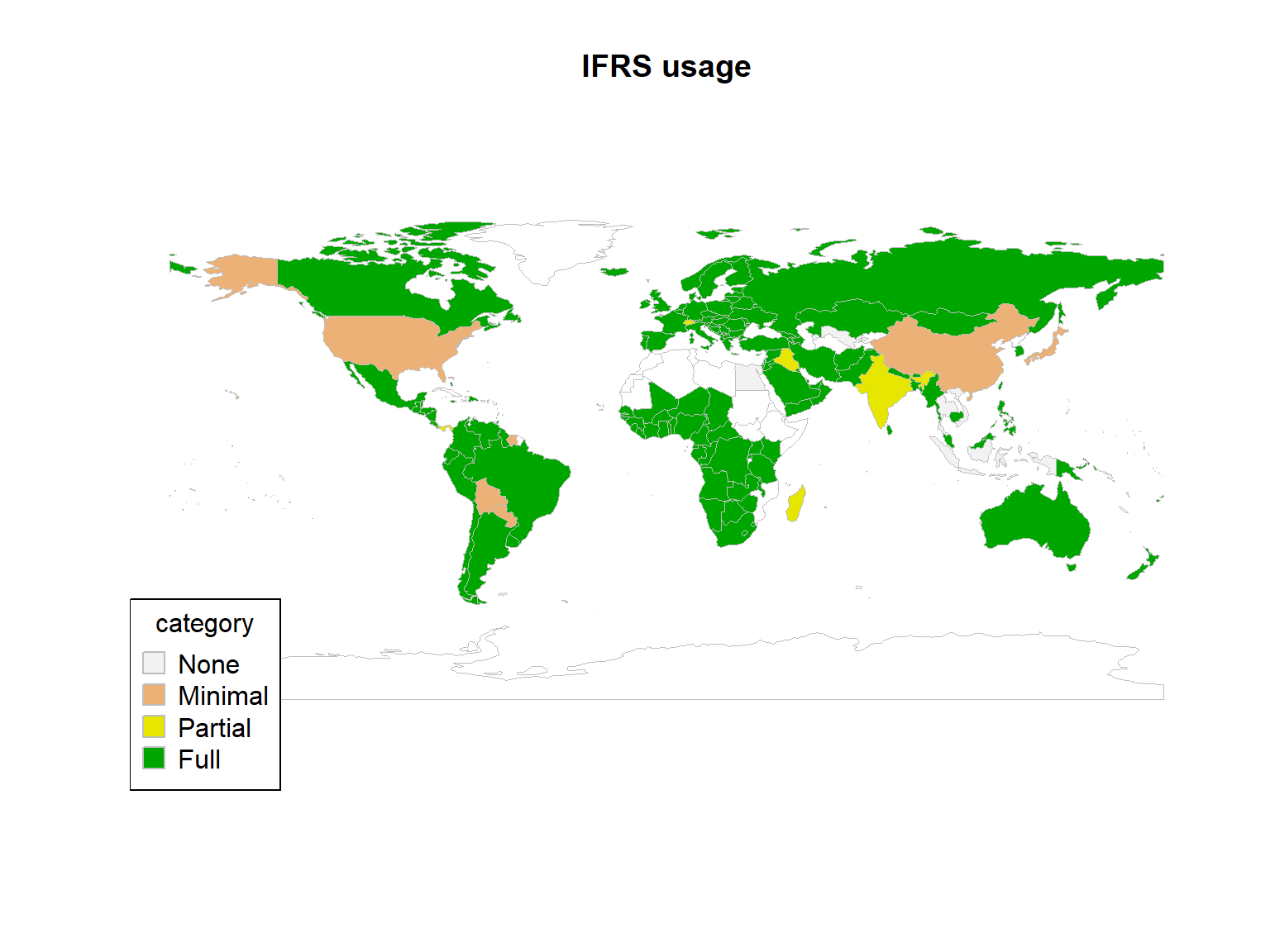

International Financial Reporting Standards

IFRS (our accounting rules)

- IASB created IFRS in 2001

- An attempt to standardize accounting rules across countries

- Over 100 countries and 49,890 companies use IFRS

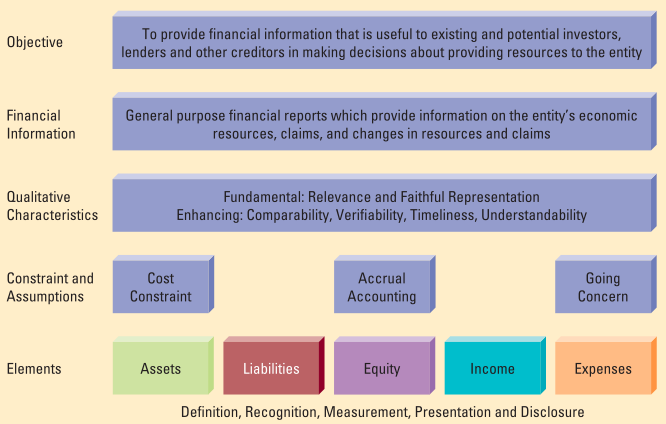

IFRS conceptual framework

IFRS conceptual framework

- Prescribes nature, function, and boundary of an accounting system

- Purpose: To provide financial information that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity

The conceptual framework lays a foundation for resolving big issues

Financial Information

- Focused on general purpose financial statements prepared at least annually

- Usually quarterly

- Semiannually in the UK

- Economic resources: what you own

- Inventory, buildings, patents, etc.

- Claims: claims on the company’s assets

- Claims by lenders and creditors (debt)

- Claims by owners (shareholders)

Relevance

- Fundamental characteristic

- Is the information material?

- Material: Important enough to warrant sharing

- Would not disclosing (or incorrectly disclosing) affect users’ decisions?

The information is useful

Faithful representation

- Fundamental characteristic

- Complete: Includes all necessary information to understand economic phenomenon

- Neutral: No bias

- Free from error: no errors or omissions

Information is complete, neutral and free from error

Comparability

- Enhancing characterisic

- Information by the firm can be compared across years

- Not across firms

- If you change the way something is calculated, show the new and the old way

Compare over time for the same firm

Verifiability

- Enhancing characterisic

- All accounting figures can be verified from a paper trail

- Receipts

- Records of counts

- Calculations

Verifiability: Paper trail

Timeliness

- Enhancing characterisic

- Takes time to prepare and verify information

- More timely is a tradeoff with other characteristics

Is the information useful when released?

Understandability

- Enhancing characteristic

- Regardless of how useful the content is, it isn’t useful unless users can understand it

- Baseline is a reasonably educated user

- You after you finish this class

Can a reasonably educated user use it?

Accrual accounting

- Assumption

- The basis for our accounting system and many others

- Alternative is cash basis

- Record when cash changes hands

- This will be the focus next week

Record when something happens, not when cash changes hands

Going concern

- Assumption

- Entity will last long enough to use all assets and pay all liabilities

Assume the company isn’t collapsing

Cost constraint

Costs

- Companies paying money to employees and auditors

- Theoretical societal loss from leaking of confidential information

Benefits

- Gain from distribution of information

- Leads to more informed investments

- Better contracts

- Better economy

Benefit of accounting to society outweighs its cost

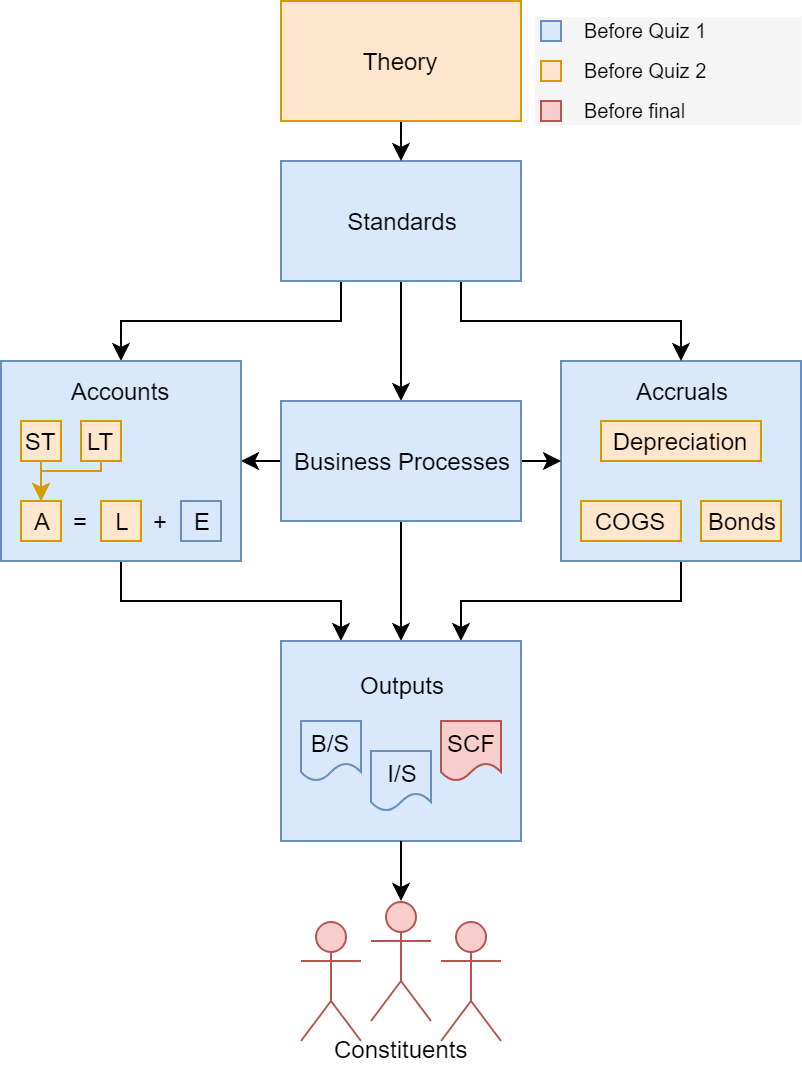

Review

Financial statements

Note

- We’ll cover each of these at length later

- Covered in Session 3:

- Income Statement

- Changes in Equity

- Balance Sheet

- Covered in Sessions 10 and 11:

- Statement of Cash Flows

Income Statement

- Part of the Statement of Comprehensive Income

- We’ll get to this later

- Shows net profit or loss for a period

- Comprised of:

- Revenues and gains

- Expenses and losses

- Comprised of:

Statement of Changes in Equity

- Shows transactions with owners

- Net income flows from the Income Statement to this Statement

- Includes outflows from dividends

Balance Sheet

- More formally known as the Statement of Financial Position

- A snapshot at a point in time of a company’s:

- Assets

- Liabilities

- Equity

Statement of Cash Flows

- Measures cash receipts and payments

- Breaks cash activities into:

- Operating activities

- Investing activities

- Financing activities

Examples

Building blocks of accounting

Building blocks

- Everything is classified as one of:

- Assets

- Liabilities

- [Shareholders’] Equity

These cover all elements of a transaction

Assets

Economic resources controlled by an entity which are expected to produce future economic benefits to the entity.

- Cash, accounts receivable (A/R)

- Inventory, equipment

- Factories, machinery

- Coffee shop:

- Cash

- Inventory (coffee beans, food)

- Fixed assets (building, espresso machine)

Debit = Increase \(\qquad\) Credit = Decrease

Liabilities

Present obligations of the entity which are expected to result in an outflow of economic benefits from the entity.

- Accounts payable

- Bills outstanding: Wages payable, utilities payable

- Debt

- Coffee shop:

- Bank loan (maybe used to buy the building)

- Outstanding utility bill

- Bill from coffee supplier

Debit = Decrease \(\qquad\) Credit = Increase

Equity

The residual interest in the entity’s assets after deducting the entity’s liabilities and represents shareholder’s residual claim to the entity’s assets.

- Share capital: Amount paid in by owners

- Retained earnings: net profit not released as dividends

- Revenue: Sales, income

- Expenses: costs of doing business

- Coffee shop:

- The money put in by the founder

- Revenue from selling coffee and expenses from paid wages

Debit = Decrease \(\qquad\) Credit = Increase

In class activity

Instructions:

- Divide up into groups of 4

- Pick any company

- Determine 3 each of:

- Assets

- Liabilities

- Equity

Raise your hand to call me over if you would like something clarified

If you would like to share your work with the class, call me over to let me know (2-3 groups)

Fill out:

- Company:

- Assets:

- Liabilities:

- Shareholders’ Equity:

The accounting equation

Base equation

\[Assets = Liabilites + Equity\]

- Intuition:

- All the assets must be owned by someone

- Liabilities and Equity represent all the claims on assets

- Assets must equal liabilities plus equity

Changing assets

Increase

- Receiving assets

- Creating assets

Decrease

- Selling assets

- Using assets

Changing liabilities

Increase

- Receiving a debt

- Payables: like bills

- Loans

- Recognizing something you owe

Decrease

- Paying off a debt

Changing equity: Income and expenses

Increase

- Income increases equity

- Revenues: Income from ordinary operations

- Gains: Income from other activities

Decrease

- Expenses decrease equity

- Expenses: Expenses from ordinary operations

- Losses: Expenses from other activities

| Effect on equity | Ordinary activity | Not ordinary |

|---|---|---|

| Increase equity | Revenue | Gain |

| Decrease equity | Expense | Loss |

Changing equity: other accounts

Increase

- Share capital

- Money paid in by owners

- For corporation: money paid in at IPO or SEO

- Retained earnings

- Economic contribution of the firm (lifetime)

Decrease

- Dividends

- Paid to shareholders

- Not an expense!

Retained earnings: \(\sum_{\text{all years}}(Revenues - Expenses - Dividends)\)

Expanded equation

\[ \begin{align} Assets &= Liabilities + Equity \\ \\ Equity &= Shares + Retained~Earnings - Dividends \\ &+ Revenues - Expenses \end{align} \]

Tips on the accounting equation

- Raising capital: assets ↑ (cash), equity ↑ (share capital)

- Paying an expense early: assets ↑ (prepaid expense), assets ↓ (cash) [no net effect]

- Paying prerecorded wages: assets ↓ (cash), liability ↓ (salaries payable)

- Revenue: asset ↑ (cash), revenue ↑

- With inventory, add: asset ↓ (inventory), expense ↑ (cost of goods sold)

- Paying debt: assets ↓ (cash), liabilities ↓

- No change in equity unless there’s an interest payment

Group problems

- How would the following transactions affect the expanded accounting equation for a small coffee shop?

- Sell a latte to a customer.

- Pay the utility bill.

- Buy lunch for the supplier’s representative.

- Take a business trip to Guatemala to visit coffee farms. Paid by cash.

- Take a vacation to Guatemala (not for business).

- Bought a new coffee maker on credit.

Try to work these out with your group. If you are stuck/confused, call me over to help.

In class work

Harder group problem

- Pick a company

- Come up with 3 transactions the company might have

- How would each transaction affect the company’s accounting equation, and why?

- Company:

- Transactions:

- A ↑/↓, L ↑/↓, E ↑/↓

- Explanation:

- A ↑/↓, L ↑/↓, E ↑/↓

- Explanation:

- A ↑/↓, L ↑/↓, E ↑/↓

- Explanation:

- A ↑/↓, L ↑/↓, E ↑/↓

- Email me your 3 transactions + explanation by the end of the day

- Include all group members’ names in the email!

End matter

Wrap up

- For next week:

- Recap the reading for this week

- Read the pages for next week

- Bookkeeping (Chapter 2)

- Accrual accounting and adjusting entries (Chapter 3)

- Practice on eLearn

- Automatic feedback provided

- Make sure you have the accounts and accounting equation down!

- You’ll need to know these next week

Packages used for these slides

- kableExtra

- knitr

- plotly

- revealjs

- rworldmap

- tidyverse

- zoo