Main question

Can we use bankruptcy models to predict supplier bankruptcies?

But first:

Does the Altman Z-score [still] pick up bankruptcy?

df %>%

filter(!is.na(Z),

!is.na(bankrupt)) %>%

group_by(bankrupt) %>%

mutate(mean_Z=mean(Z,na.rm=T)) %>%

slice(1) %>%

ungroup() %>%

select(bankrupt, mean_Z) %>%

html_df()| bankrupt | mean_Z |

|---|---|

| 0 | 3.939223 |

| 1 | 0.927843 |

df %>%

filter(!is.na(Z),

!is.na(bankrupt),

year >= 2000) %>%

group_by(bankrupt) %>%

mutate(mean_Z=mean(Z,na.rm=T)) %>%

slice(1) %>%

ungroup() %>%

select(bankrupt, mean_Z) %>%

html_df()| bankrupt | mean_Z |

|---|---|

| 0 | 3.822281 |

| 1 | 1.417683 |

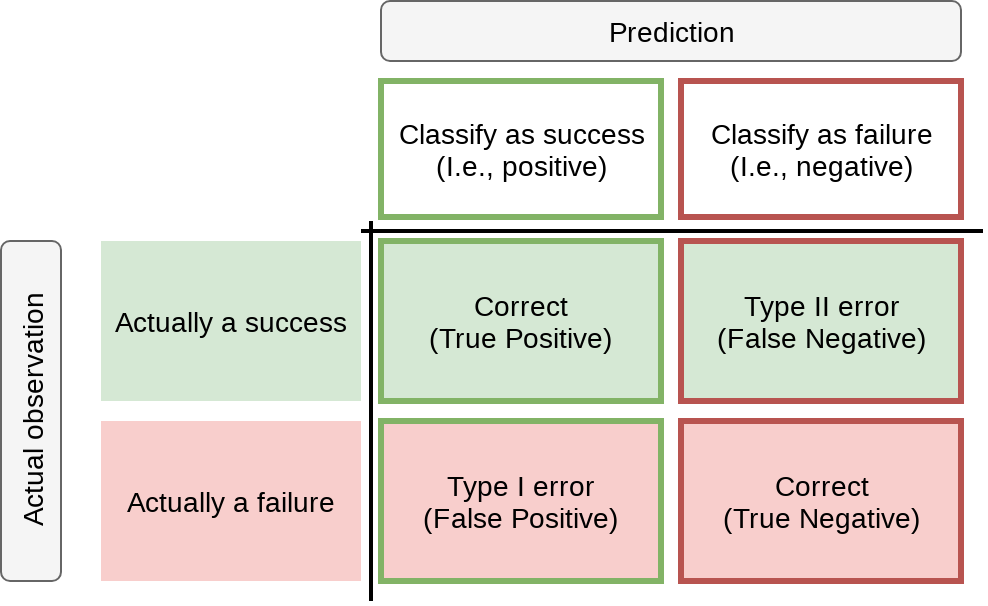

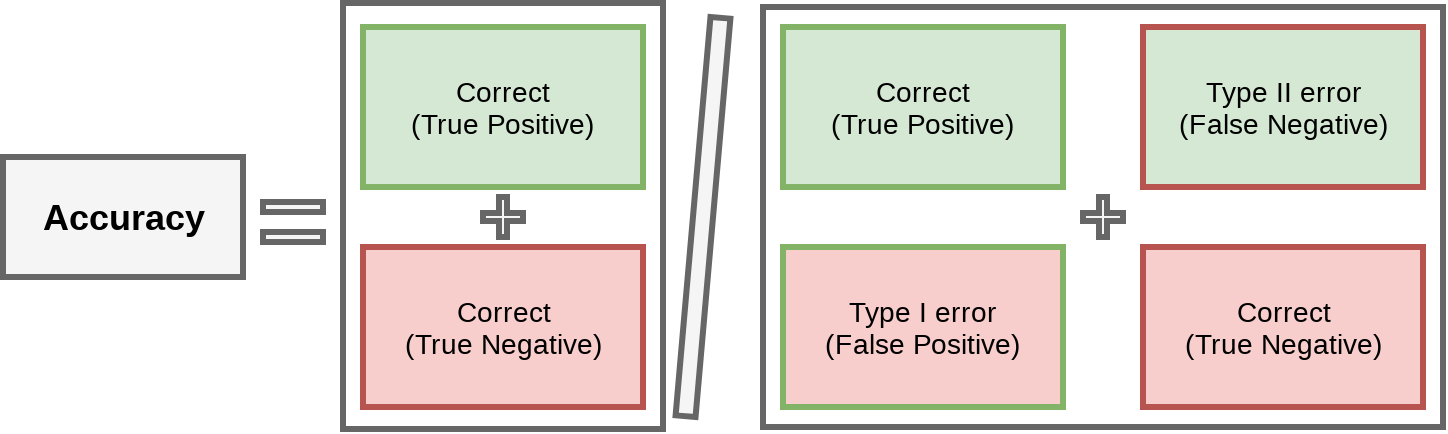

This type of chart (filled in) is called a Confusion matrix

We say that the company will go bankrupt, but they don’t

We say that the company will not go bankrupt, yet they do

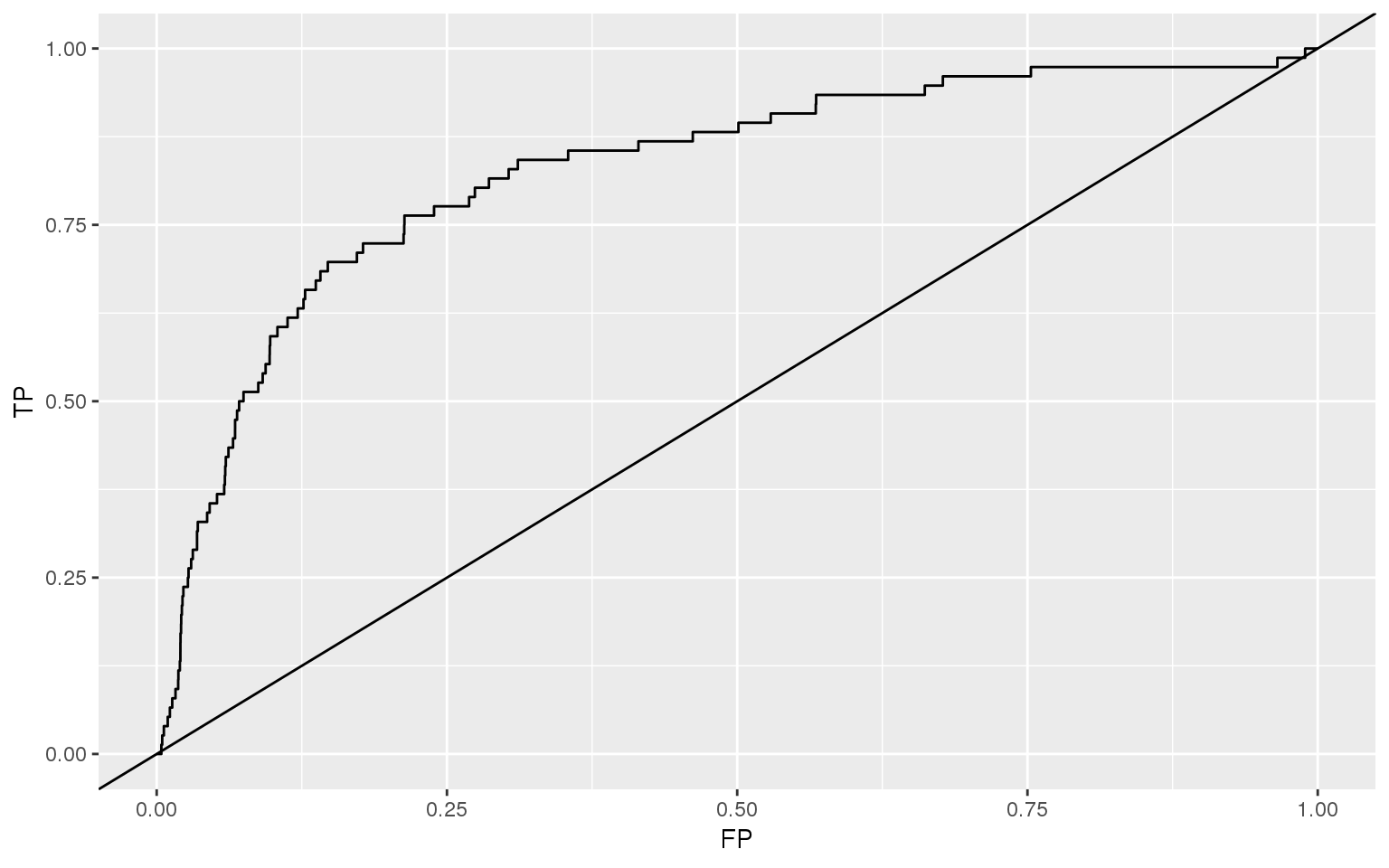

df_ROC_Z <- data.frame(

FP=c(ROCperf_Z@x.values[[1]]),

TP=c(ROCperf_Z@y.values[[1]]))

ggplot(data=df_ROC_Z,

aes(x=FP, y=TP)) + geom_line() +

geom_abline(slope=1)

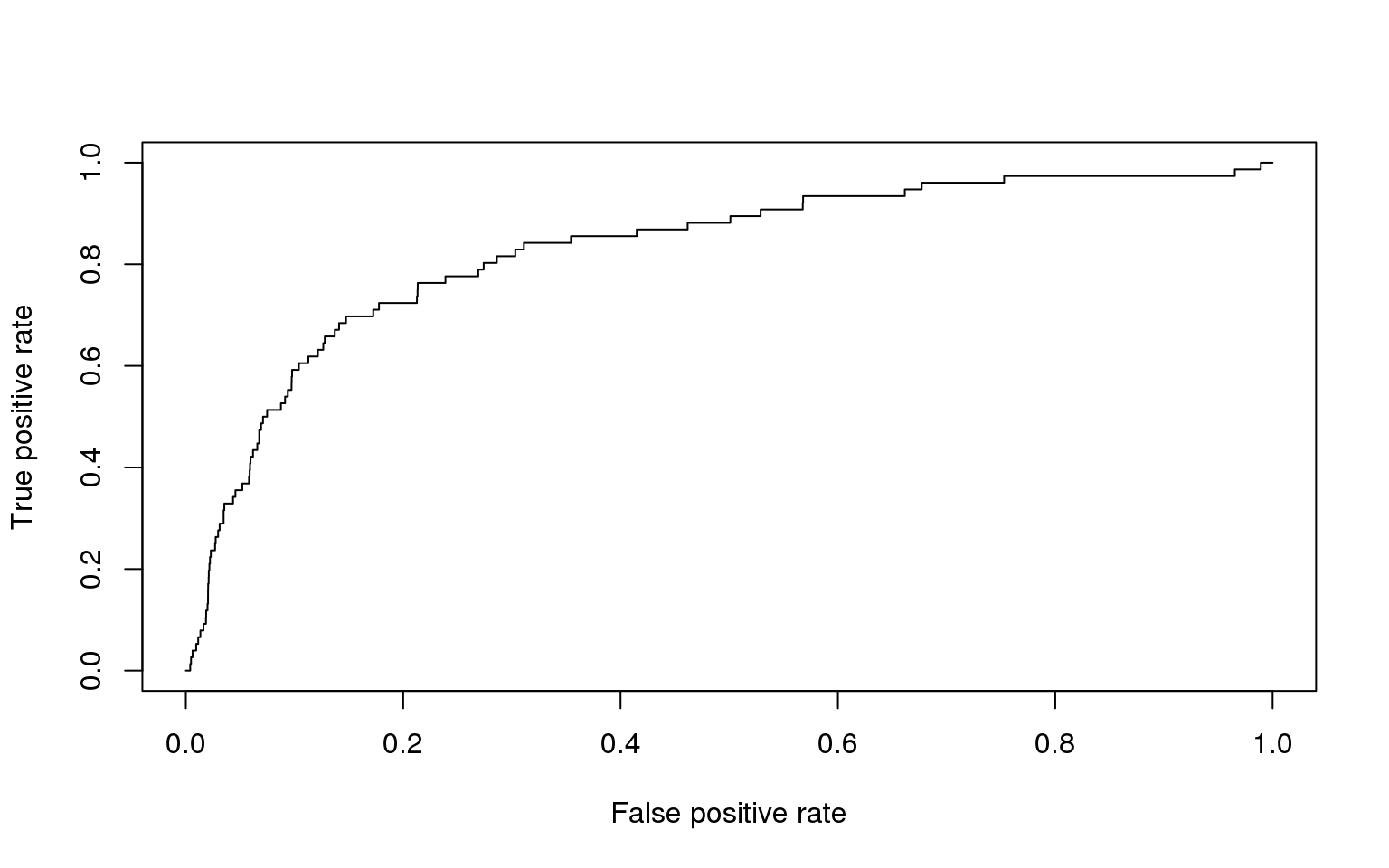

plot(ROCperf_Z)

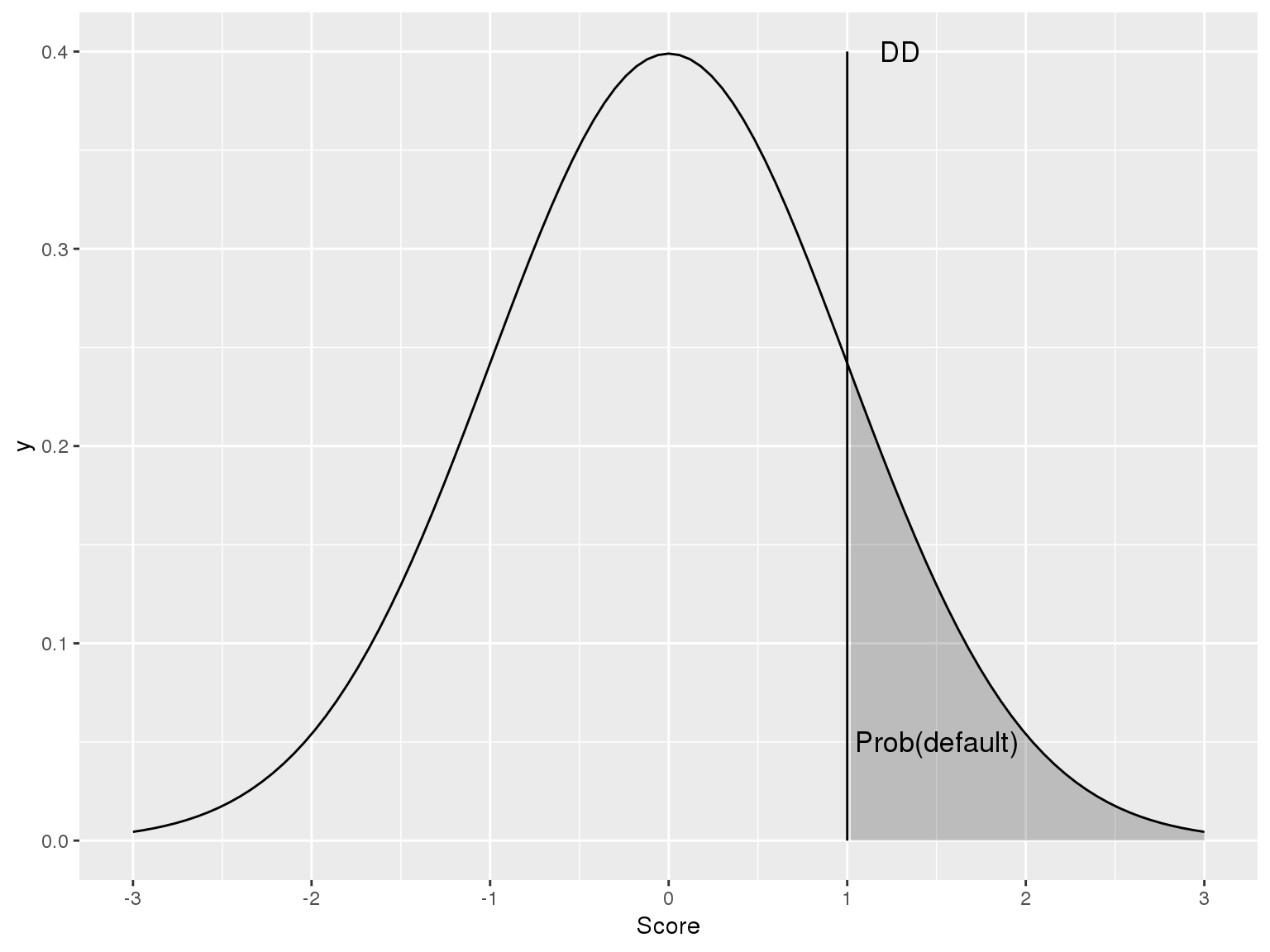

DD = \frac{\log(V_A / D) + (r-\frac{1}{2}\sigma_A^2)(T-t)}{\sigma_A \sqrt(T-t)}

df %>%

filter(!is.na(DD),

!is.na(bankrupt)) %>%

group_by(bankrupt) %>%

mutate(mean_DD=mean(DD, na.rm=T),

prob_default =

pnorm(-1 * mean_DD)) %>%

slice(1) %>%

ungroup() %>%

select(bankrupt, mean_DD,

prob_default) %>%

html_df()| bankrupt | mean_DD | prob_default |

|---|---|---|

| 0 | 0.612414 | 0.2701319 |

| 1 | -2.447382 | 0.9928051 |

df %>%

filter(!is.na(DD),

!is.na(bankrupt),

year >= 2000) %>%

group_by(bankrupt) %>%

mutate(mean_DD=mean(DD, na.rm=T),

prob_default =

pnorm(-1 * mean_DD)) %>%

slice(1) %>%

ungroup() %>%

select(bankrupt, mean_DD,

prob_default) %>%

html_df()| bankrupt | mean_DD | prob_default |

|---|---|---|

| 0 | 0.8411654 | 0.2001276 |

| 1 | -4.3076039 | 0.9999917 |

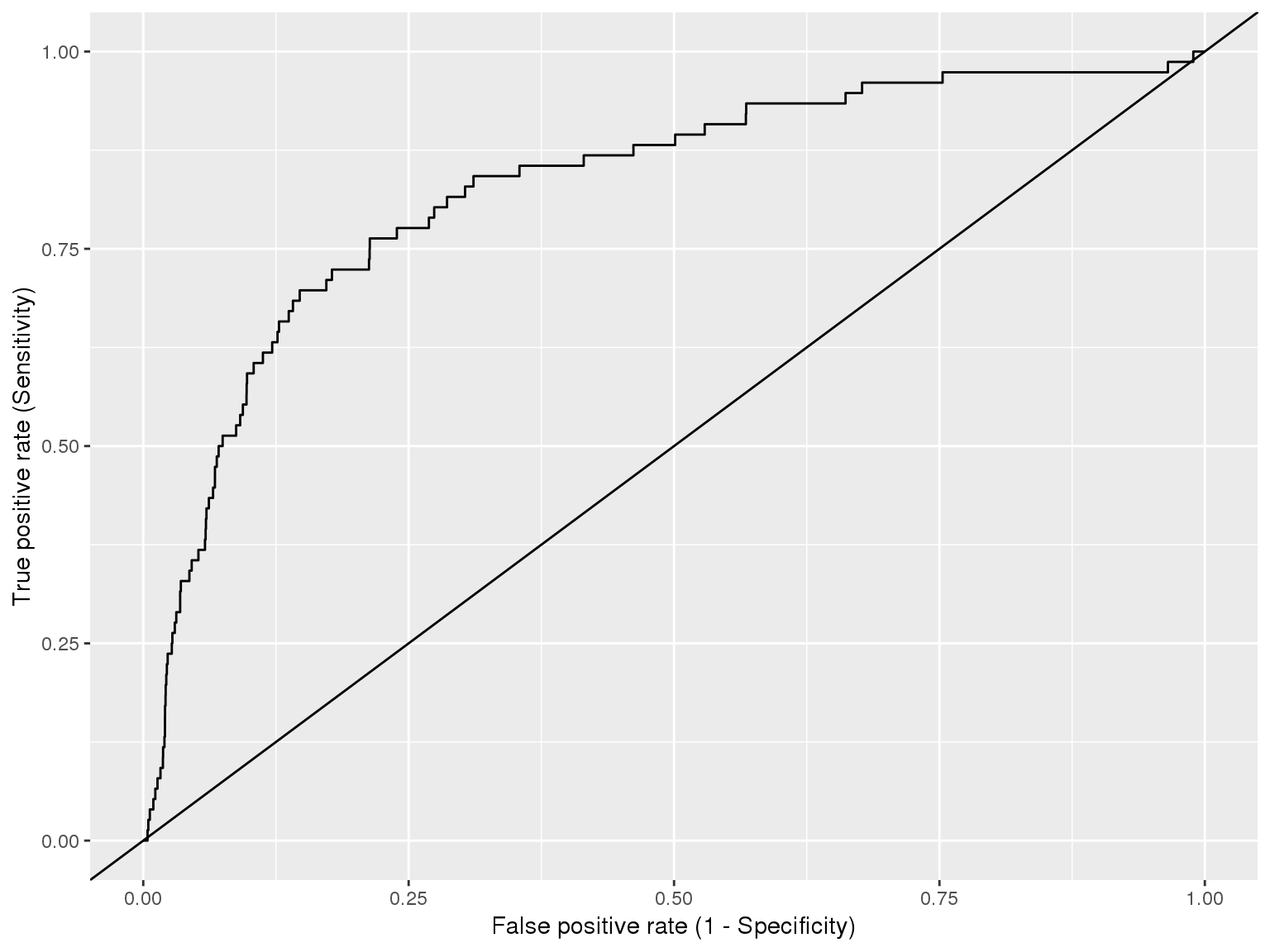

pred_DD <- predict(fit_DD, df, type="response")

ROCpred_DD <- prediction(as.numeric(pred_DD), as.numeric(df$bankrupt))

ROCperf_DD <- performance(ROCpred_DD, 'tpr','fpr')

df_ROC_DD <- data.frame(FalsePositive=c(ROCperf_DD@x.values[[1]]),

TruePositive=c(ROCperf_DD@y.values[[1]]))

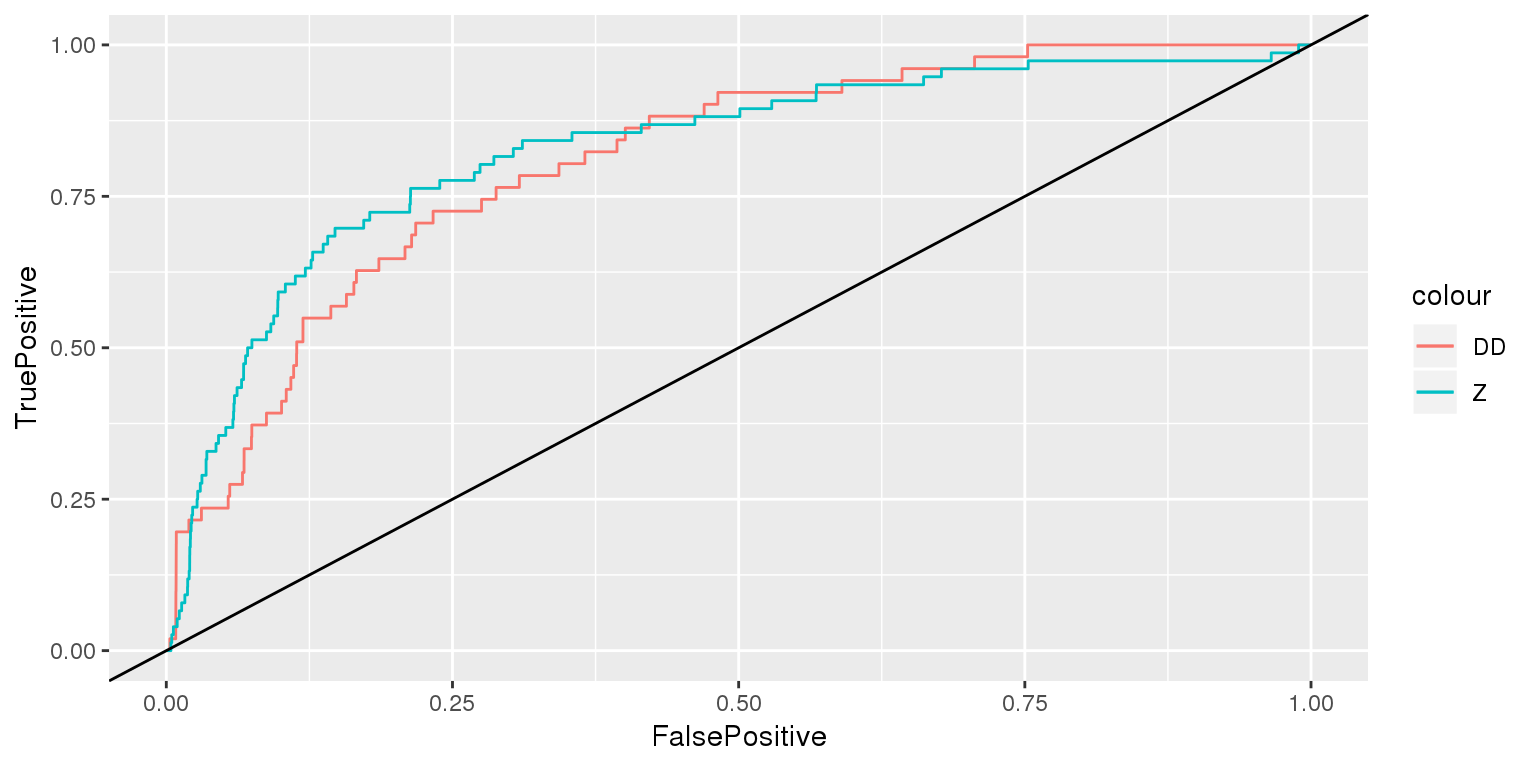

ggplot() +

geom_line(data=df_ROC_DD, aes(x=FalsePositive, y=TruePositive, color="DD")) +

geom_line(data=df_ROC_Z, aes(x=FP, y=TP, color="Z")) +

geom_abline(slope=1)

## Z DD

## 0.6839086 0.6811973

## Z DD

## 0.7270046 0.7183575