Learning objectives

- Theory:

- Develop a logical approach to problem solving with data

- Statistics

- Causation

- Hypothesis testing

- Develop a logical approach to problem solving with data

- Application:

- Predicting revenue for real estate firms

- Methodology:

- Univariate stats

- Linear regression

- Visualization

R Markdown: A quick guide

- Headers and subheaders start with

#and##, respectively - Code blocks starts with

```{r}and end with```- By default, all code and figures will show up in the document

- Inline code goes in a block starting with

`rand ending with` - Italic font can be used by putting

*or_around text - Bold font can be used by putting

**around text- E.g.:

**bold text**becomes bold text

- E.g.:

- To render the document, click

- Math can be placed between

$to use LaTeX notation- E.g.

$\frac{revt}{at}$becomes \(\frac{revt}{at}\)

- E.g.

- Full equations (on their own line) can be placed between

$$ - A block quote is prefixed with

> - For a complete guide, see R Studio’s R Markdown::Cheat Sheet

Example

Let’s predict UOL’s revenue for 2016

- Compustat has data for them since 1989

- Complete since 1994

- Missing CapEx before that

- Complete since 1994

## revt at

## Min. : 94.78 Min. : 1218

## 1st Qu.: 193.41 1st Qu.: 3044

## Median : 427.44 Median : 3478

## Mean : 666.38 Mean : 5534

## 3rd Qu.:1058.61 3rd Qu.: 7939

## Max. :2103.15 Max. :19623Why is it called Ordinary Least Squares?

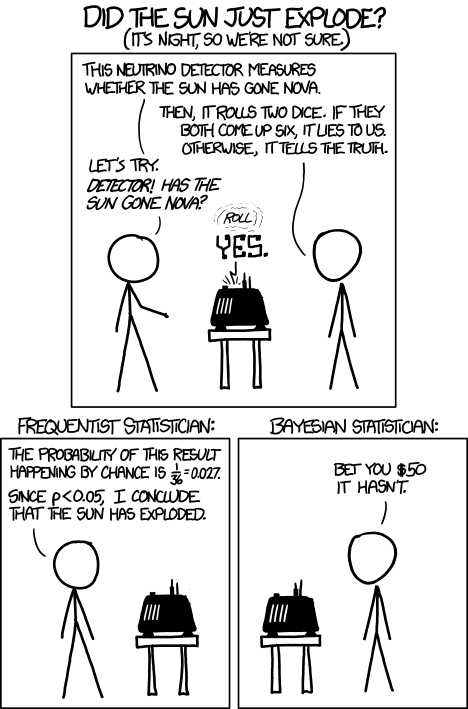

Frequentist vs Bayesian methods

This is why we use more than 1 data point

Mental model of OLS: 1 input

Simple OLS measures a simple linear relationship between an input and an output

- E.g.: Our first regression this week: Revenue on assets

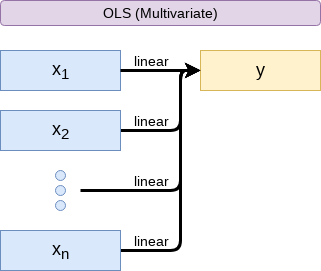

Mental model of OLS: Multiple inputs

OLS measures simple linear relationships between a set of inputs and one output

- E.g.: This is what we did when scaling up earlier this session

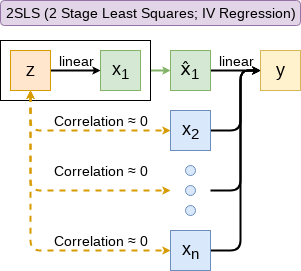

Other linear models: IV Regression (2SLS)

IV/2SLS models linear relationships where the effect of some \(x_i\) on \(y\) may be confounded by outside factors.

- E.g.: Modeling the effect of management pay duration (like bond duration) on firms’ choice to issue earnings forecasts

- Instrument with CEO tenure (Cheng, Cho, and Kim 2015)

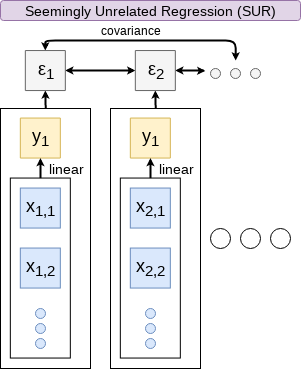

Other linear models: SUR

SUR models systems with related error terms

- E.g.: Modeling both revenue and earnings simultaneously

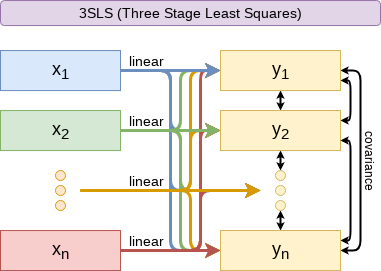

Other linear models: 3SLS

3SLS models systems of equations with related outputs

- E.g.: Modeling stock return, volatility, and volume simultaneously

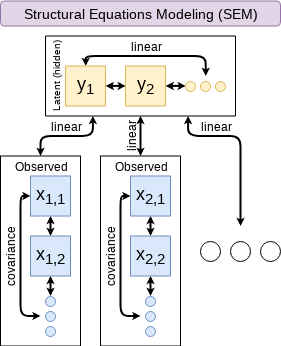

Other linear models: SEM

SEM can model abstract and multi-level relationships

- E.g.: Showing that organizational commitment leads to higher job satisfaction, not the other way around (Poznanski and Bline 1999)

Modeling choices: Variable selection

- The options:

- Use your own knowledge to select variables

- Use a selection model to automate it

Own knowledge

- Build a model based on your knowledge of the problem and situation

- This is generally better

- The result should be more interpretable

- For prediction, you should know relationships better than most algorithms

Modeling choices: Automated selection

- Traditional methods include:

- Forward selection: Start with nothing and add variables with the most contribution to Adj \(R^2\) until it stops going up

- Backward selection: Start with all inputs and remove variables with the worst (negative) contribution to Adj \(R^2\) until it stops going up

- Stepwise selection: Like forward selection, but drops non-significant predictors

- Newer methods:

- Lasso and Elastic Net based models

- Optimize with high penalties for complexity (i.e., # of inputs)

- We will discuss these in week 5

- Lasso and Elastic Net based models

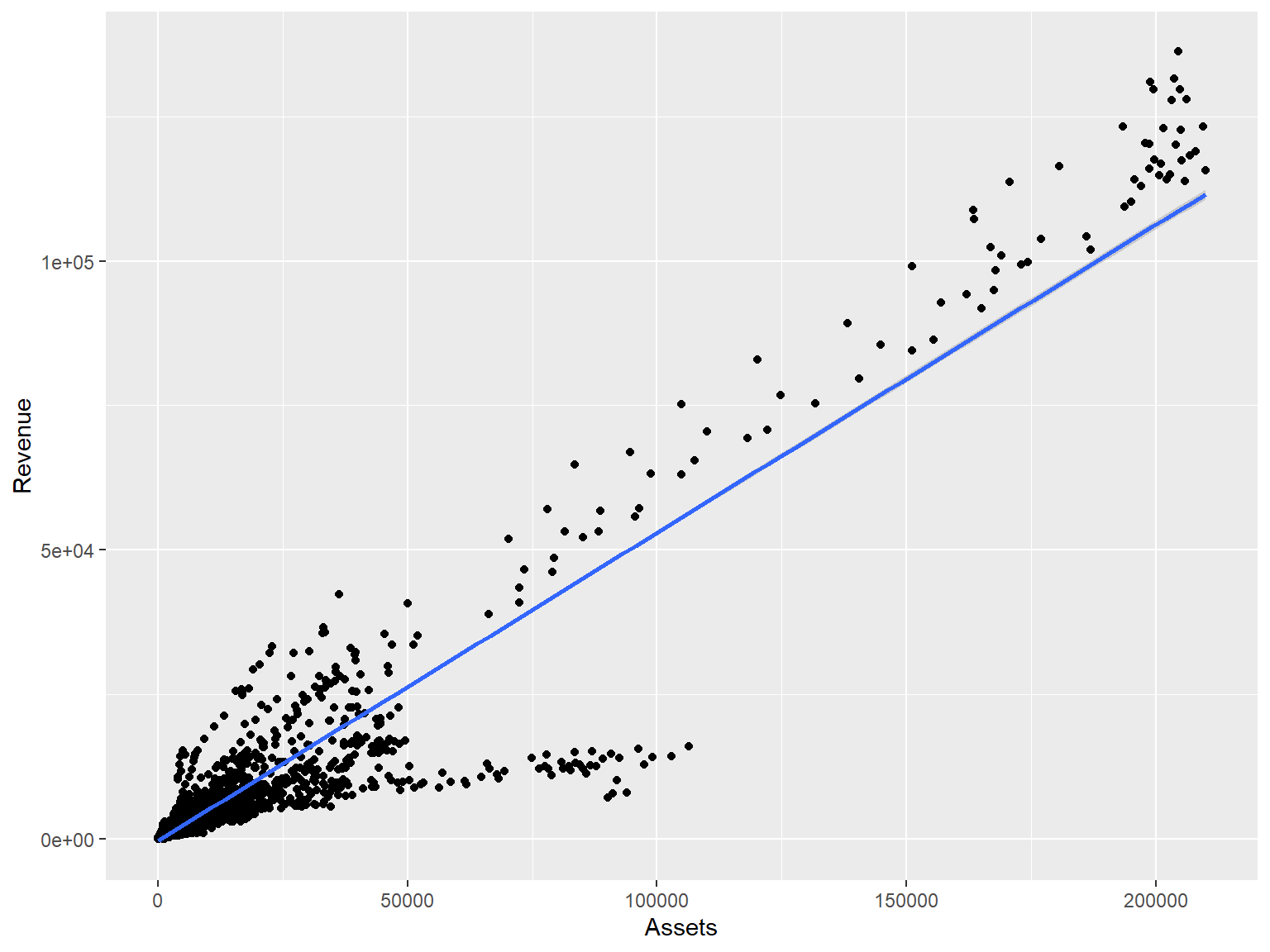

Coefficients

- In OLS: \(\beta_i\)

- A change in \(x_i\) by 1 leads to a change in \(y\) by \(\beta_i\)

- Essentially, the slope between \(x\) and \(y\)

- The blue line in the chart is the regression line for \(\hat{Revenue} = \alpha + \beta_i \hat{Assets}\) for retail firms since 1960

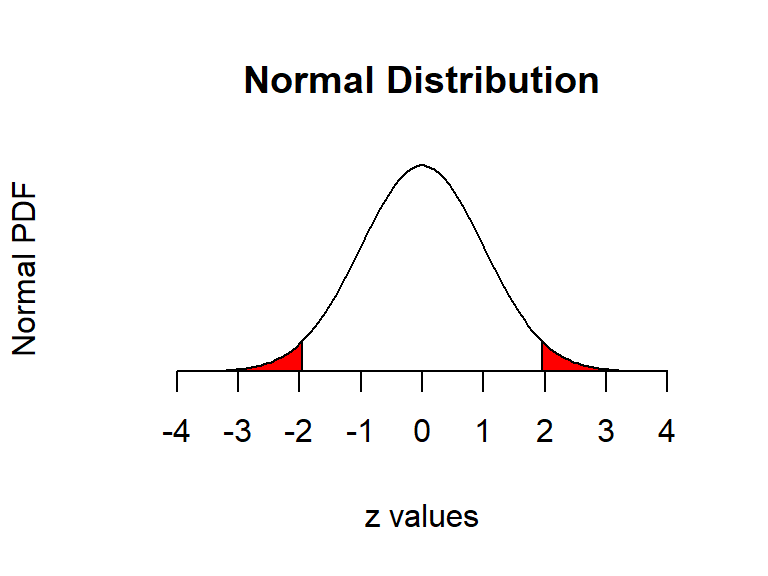

One vs two tailed tests

- Best practice:

- Use a two tailed test

- Second best practice:

- If you use a 1-tailed test, use a p-value cutoff of 0.025 or 0.05

- This is equivalent to the best practice, just roundabout

- If you use a 1-tailed test, use a p-value cutoff of 0.025 or 0.05

- Common but generally inappropriate:

- Use a one tailed test with cutoffs of 0.05 or 0.10 because your hypothesis is directional

What is causality?

\(A \rightarrow B\)

- Causality is \(A\) causing \(B\)

- This means more than \(A\) and \(B\) are correlated

- I.e., If \(A\) changes, \(B\) changes. But \(B\) changing doesn’t mean \(A\) changed

- Unless \(B\) is 100% driven by \(A\)

- Very difficult to determine, particularly for events that happen [almost] simultaneously

- Examples of correlations that aren’t causation

Time and causality break down

\(A_t \rightarrow B_{t+1}\)? \(\quad\) OR \(\quad\) \(C \rightarrow A_t\) and \(C \rightarrow B_{t+1}\)?

- The above illustrates the Correlated omitted variable problem

- \(A\) doesn’t cause \(B\)… Instead, some other force \(C\) causes both

- The bane of social scientists everywhere

- This is less important for predictive analytics, as we care more about performance, but…

- It can complicate interpreting your results

- Figuring out \(C\) can help improve you model’s predictions

- So find C!

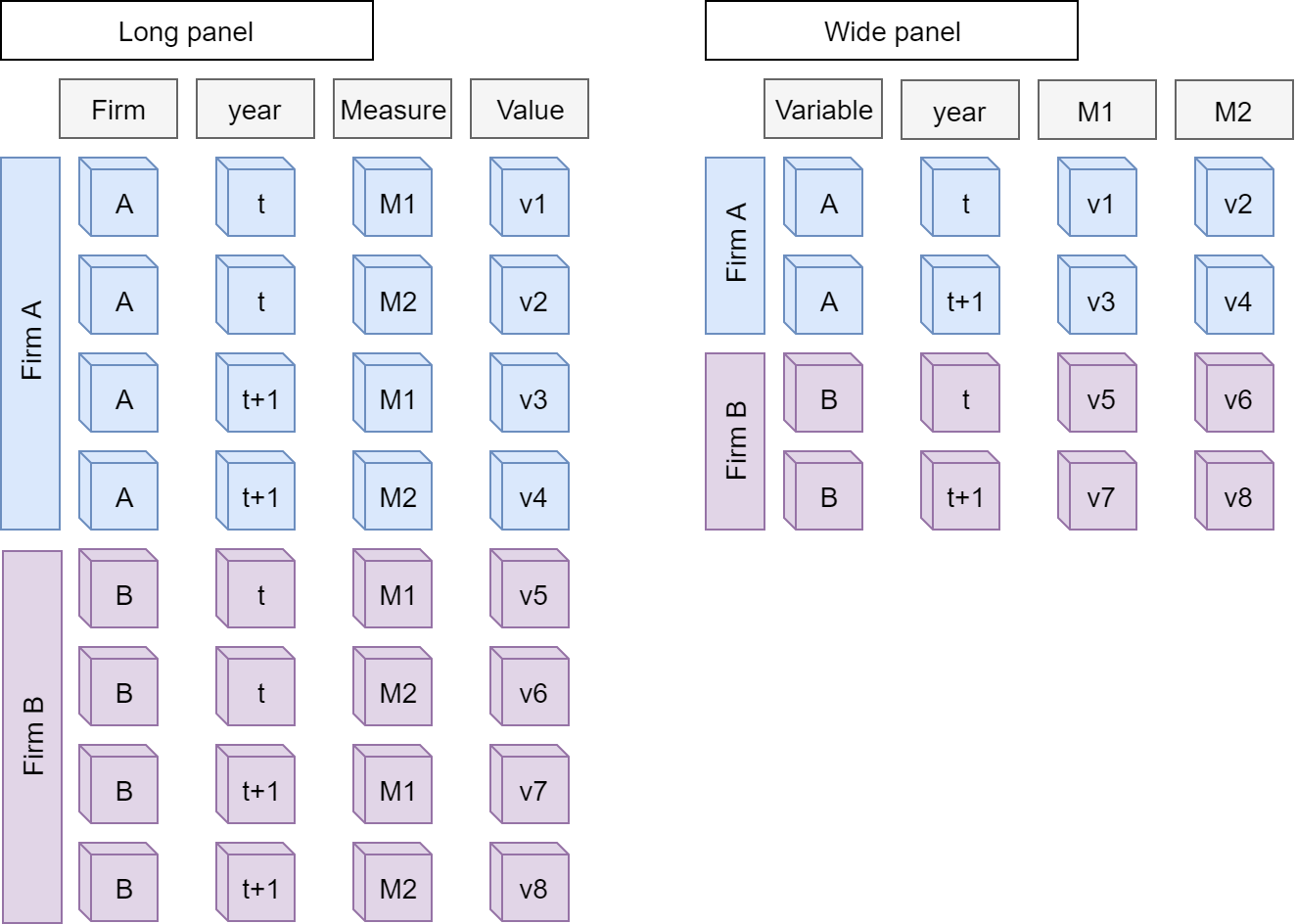

Panel data

Data frames are usually wide panels

All Singapore real estate companies

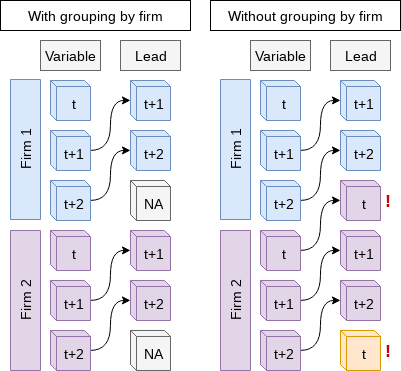

# Note the group_by -- without it, lead() will pull from the subsequent firm!

# ungroup() tells R that we finished grouping

df_clean <- df_clean %>%

group_by(isin) %>%

mutate(revt_lead = lead(revt)) %>%

ungroup()

Why exactly would we use fixed effects?

- Fixed effects are used when the average of \(\hat{y}\) varies by some group in our data

- In our problem, the average revenue of each firm is different

- Fixed effects absorb this difference

- Further reading:

- Introductory Econometrics by Jeffrey M. Wooldridge